Colgate-Palmolive (NYSE:CL) is one of the world’s largest consumer products companies, founded in 1806. Since then, the company has gradually become a leader in the production of personal care and home care products, and its products are currently sold in almost every corner of our planet.

The Oral Care business is key to Colgate-Palmolive’s financial position, accounting for more than 40% of its total revenue. Its portfolio comprises pharmaceutical products for dentists, various toothpastes, and toothbrushes sold under world-famous brands such as Colgate, Darlie, and elmex.

In addition, the company continues to be a leader in the global beauty and personal care market due to the high demand for its skin health products, shampoos, shower gels, and deodorants. The growth in sales of these products from year to year is ensured by factors such as strong brand recognition and the significant marketing capabilities of Colgate-Palmolive, which help minimize the negative impact caused by the emergence of new players in the sector.

The company also holds a leading position in the global pet food market. Colgate-Palmolive’s products are available in most countries worldwide, and their sales contributed about 21.9% of the company’s total revenue for the second quarter of 2023.

2Q 2023 Earnings Presentation

In recent months, euphoria in financial markets has continued, caused by an increase in interest in technology companies developing and implementing AI-related products and services. However, Colgate-Palmolive is a consumer defensive stock, which we believe should again begin attracting long-term investors’ attention due to its stable cash flow even during periods of geopolitical turmoil and rising inflation.

For sixty years, Colgate-Palmolive has maintained a policy of increasing dividend payments year after year, and, as a result, it is a member of the prestigious S&P 500 Dividend Aristocrats index.

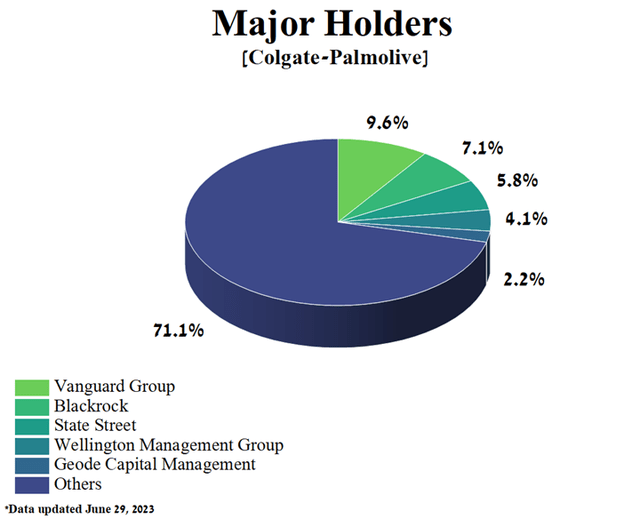

On the other hand, a significant increase in the company’s operating income in recent quarters has contributed to the fact that many well-known Wall Street companies remain among Colgate-Palmolive’s major shareholders. The top five stockholders, including Vanguard Group, State Street, Wellington Management Group, Blackrock, and Geode Capital Management, collectively hold a significant 28.9% stake in the company.

Author’s elaboration, based on Yahoo Finance

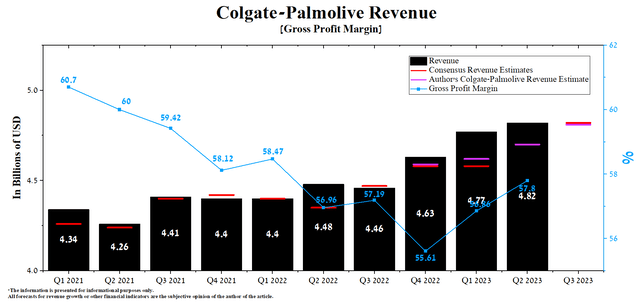

The second quarter of 2023 showed excellent results since not only Colgate-Palmolive’s revenue was able to exceed analysts’ expectations, but on the other hand, its gross margin has been growing in recent quarters despite the persistence of elevated inflation in some countries of the European Union.

On October 27, Colgate-Palmolive will publish its financial report for the third quarter of 2023. According to Seeking Alpha, Colgate-Palmolive’s third-quarter 2023 revenue is expected to be $4.72 billion to $5.01 billion, up 8.1% year-over-year and 2.6% higher than analysts’ expectations for the prior quarter. At the same time, under our model, the company’s total revenue will be within this range, amounting to $4.81 billion. We expect Colgate-Palmolive’s year-over-year revenue growth trend to continue, driven by its share in the global toothpaste market, growth in sales of Pet Nutrition products, and expansion of its personal care portfolio. These factors, in particular, will soften the negative impact of strengthening the US dollar against other currencies.

Author’s elaboration, based on Seeking Alpha

We forecast the company’s operating income margin will reach 20.1% by 2023. Moreover, in 2024, this financial metric will rise to 21.1% due to an increase in prices for the company’s goods, a decrease in the cost of raw materials and packaging materials, which are used to produce the company’s products, optimization of labor costs, and a decrease in selling and administrative expenses.

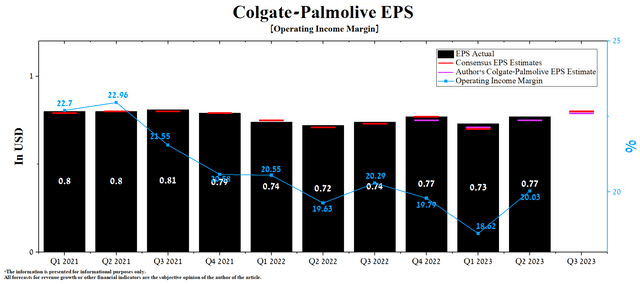

According to Seeking Alpha, Colgate-Palmolive’s Q3 EPS is expected to be $0.78-$0.82, up 6.7% from the Q2 2023 consensus estimate. At the same time, according to our model, Colgate-Palmolive’s EPS will be $0.79, an increase of 6.8% compared to the previous year.

Moreover, the company’s Non-GAAP P/E [TTM] is 22.88x, which is 38.52% higher than the sector average and 8.18% lower than the average over the past five years. On the contrary, Colgate-Palmolive’s Non-GAAP P/E [FWD] is 21.79x, which is one of the factors indicating its slight overvaluation by financial market participants at a time of rising tensions in the Middle East, which increases the likelihood of further disruptions in the global supply chain.

Author’s elaboration, based on Seeking Alpha

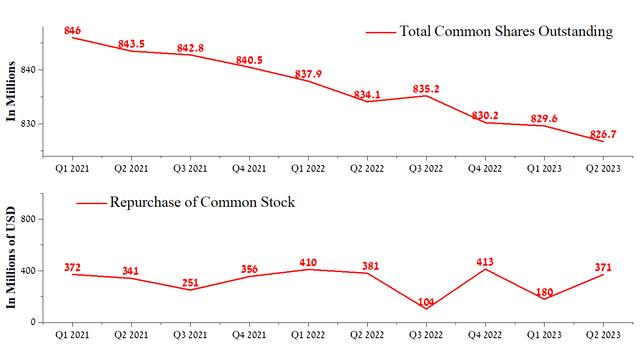

One of the main factors behind Colgate-Palmolive beating consensus EPS in recent quarters is primarily attributed to its share buyback program. Over recent years, the amount of cash flow allocated for this purpose has continued to remain stable, and for the three months of 2023 ended June 30, 2023, the company repurchased approximately $371 million of its shares.

Author’s elaboration, based on Seeking Alpha

At the same time, at the end of the second quarter of 2023, the remaining authorization to buy back Colgate-Palmolive shares amounted to $3.43 billion. According to our assessment, this will partially minimize the impact of short sellers on the company’s share price in the event of a continuation of the upward trend in inflation in the United States and a possible hike in the Fed interest rate at the end of 2023.

YCharts

Conclusion

Colgate-Palmolive is one of the world’s largest consumer products companies, founded in 1806. Since then, the company, whose headquarters is located in New York, has gradually become a leader in the production of personal care and home care products, and its products are currently sold in almost every corner of our planet.

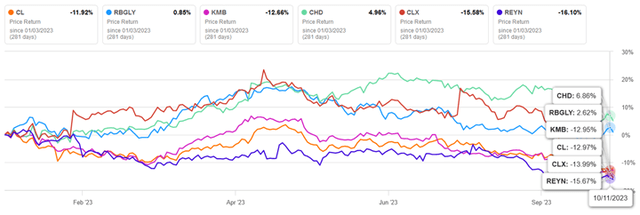

Despite the company’s margin growth, its share price is down more than 12% year-to-date, underperforming main competitors in the consumer staples sector, such as Church & Dwight (CHD) and Reckitt Benckiser Group (OTCPK:RBGLY).

Author’s elaboration, based on Seeking Alpha

On the other hand, the main risks for Colgate-Palmolive’s financial position are increased competition in the global beauty and personal care market, a significant increase in U.S. household debt, and a military conflict in the Middle East, which threatens stability in this region. Moreover, given the technical analysis, we believe that the price level at which the risk/reward profile will be attractive is $67-$68 per share.

We initiate our coverage of Colgate-Palmolive with an “outperform” rating for the next 12 months.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here