Performance Review

| NAVincrease, net |

CumIncept |

Ann Inception |

PF 2019 |

2020 |

2021 |

2022 |

YTD 2023 |

|

WBCP |

73.05% |

14.07% |

17.60% |

19.05% |

37.16% |

(15.38%) |

6.49% |

|

S&P 400 |

35.91% |

8.53% |

5.72% |

13.66% |

24.76% |

(13.06%) |

4.28% |

|

S&P 500 |

54.04% |

12.21% |

9.36% |

18.40% |

28.72% |

(18.10%) |

12.85% |

| The administrator provides performance figures. Prior years are audited. 2023 is unaudited. Performance is net of all realized and accrued fees. |

Portfolio Review

White Brook Capital Partners continues to outperform the S&P Midcap 400 year to date, up 6.49% vs the index’s 4.28% gain but has underperformed the S&P500’s (SP500, SPX) 12.85% gain.

Except for Box, Inc. which released underwhelming results for the quarter, and Green Plains, Inc. (GPRE), which encountered disappointing but temporary setbacks for the quarter, the results for the rest of the portfolio were solid or better, and expected earnings moving forward were either unrevised or revised upwards. The widespread declines resulted from systemic multiple depreciation due to the fear of the impact of recent increases in the 10-year and 30-year treasury yields and a potential recession.

White Brook Capital Partners entered a new position in Knight Swift Transportation Holdings Inc (KNX) and an undisclosed position with a less than 1% allocation at quarter end. It exited its trading position in Unity Holdings (U).

The quarter’s most significant contributors to underperformance were investments in Box, Inc. (BOX) and Builder’s First Source, Inc (BLDR). The most significant positive contributors to performance were Mosaic Inc (MOS) and Afya Ltd (AFYA).

There are currently 11 stocks in the portfolio, including a position initiated in the last week of the quarter that remains undisclosed with a less than 1% allocation as of the end of the quarter.

Market Review

While cash presents an attractive 5% return for risk-averse savers, the recent move in interest rates and the tumult in the bond markets means stable and superior returns in bonds can be had in relatively “safe” yields if investing for the medium term. For long term investors, the prices available in small and midcap stocks are very attractive and are a better option for long term capital.

The magnificent seven, that underpin the S&P 500 performance, META, Google (GOOG, GOOGL) , Apple (AAPL), Amazon (AMZN), Nvidia (NVDA), Tesla (TSLA), and Microsoft (MSFT), now comprise almost 30% of the market capitalization of the S&P500. At least three of the seven stocks have heightened downside risk and suffer from already high penetration, weakening end markets, competitive risk, and lofty valuation. They have been remarkably resilient to increased interest rates and the potential for slowing growth.

Small and midcap stocks, on the other hand, have been systemically penalized by fears of recession and continue to price that eventuality even as significantly better outcomes have become more probable. Today, it’s relatively easy to find attractive investments in this segment.

With supply chain pressures from Covid-19 largely receded, smaller companies are newly competitive against their larger brethren. This year’s increase in interest rates has masked that positive traction, as fears of recession have maintained pressure on small and midcap stocks irrespective of their business’ or capital structure’s actual sensitivity to interest rates or the underlying business’ momentum.

Furthermore, I’m more bullish on the overall economy than most given still strong employment trends and the solid position of the US Consumer. Furthermore, I believe there’s a high likelihood that consumers will shift marginal spending from travel back to goods, a relative boon for the economy. I expect that perhaps during the fourth quarter, but certainly by the first quarter of 2024, many of the remaining built-up inventories will be depleted, and the economy can be closer to run-rate normality by early 2024. This would be a significant positive for the economy and the market.

Opportunities/Inflection Points

White Brook is attracted to businesses currently experiencing a likely nadir because their inflections are usually alternatively underestimated and then overestimated, leading to significant returns for numerate investors. While waiting for those turns can take longer than expected, they are usually worthwhile investments. A few to keep your eyes on include:

Railcars: During the quarter, several of the largest railcar manufacturers’ management spoke at an industry conference. Between those discussions and our follow-up, there were two significant takeaways.

- There is no demand spike this year, and the industry continues to plan for 40,000 railcar deliveries for the next two to three. Those 40,000 cars replace expensive and hard to maintain cars that are both in operation today and that comprise a significant amount of the railcars in storage. This is a good market environment for incumbents. While the industry is hopeful about onshoring and there are whispers of the need for additional cars to move freight to and from new US factories, skepticism developed over the railcar industry’s history pervades the manufacturers, and they plan to deliver from existing capacity if and when that demand materializes.

- Higher interest rates are a boon for railcar lessors. An increase in interest rates of 1% translates to an increase in lease rates of $100 per railcar per month. Given current rates, upon renewal, an increase of $300 per month per car won’t be atypical.

Separately, Greenbrier Companies (GBX), announced a $1.9bn backlog in mid-September that positively surprised the industry. It suggests Greenbrier’s manufacturing is filled through 2025, although it’s unclear whether other manufacturers saw similar demand.

The stock positively reacted to the news before negatively reacting to increases in the 10-year treasury, which, ironically, ultimately helps them and their growing leasing operations. WBCP continues to own the stock and believes it is attractively valued.

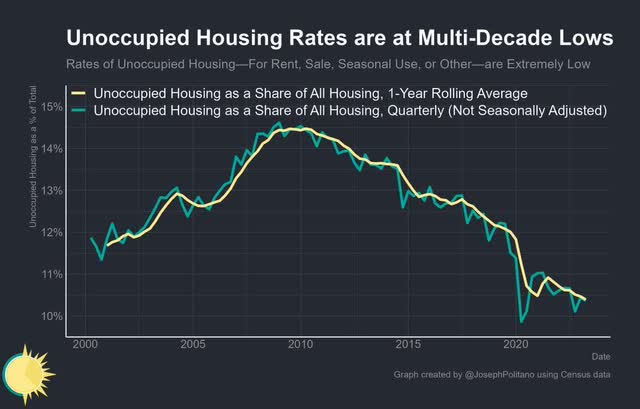

Housing: White Brook continues to invest in Builders FirstSource (BLDR) and believes the stock is materially undervalued. While higher interest rates have substantially slowed the existing housing market, new homes are being built at an above-consensus rate. Fundamentally, the United States continues to be under housed with occupancy of housing at all-time highs, even if particular markets most impacted by the technology sector (SF, Seattle) and a reversal of work from home practices (Miami, Phoenix, exurbs) now see a substantial decline in existing home sale prices.

Tactically, the nation’s largest home builders have adapted to the interest rate environment by adjusting the size of homes built and by subsidizing new customer loans. New housing permits and starts have been far above worst case expectations, and materially better than what would have been expected unless there was a housing shortage, given the current mortgage rate environment. Further supported by solid renovation activity, Builders continues to generate prodigious free cash flow. Over the medium term, the country’s insufficient housing position will have to be rectified, and Builders is well positioned.

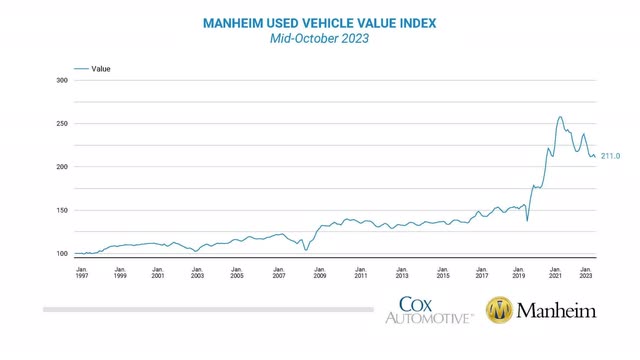

Autos: U.S. new car inventory climbed to the highest level since spring 2021, up 60% from a year ago, and back to “normal” for the industry. New car dealers have less bargaining power than they’ve had since early 2020, which should lead to lower realized new car prices in the short term. Sharply higher interest rates in the first weeks of October only improve the urgency for dealerships to move inventory rather than pay floorplan financing costs, particularly as another model year begins to make it to dealerships and used cars get another year older.

Consumers, also impacted by higher rates, make much lower prices more likely than they have been since the beginning of Covid. I expect the used car market to mirror the new, with total transactions likely to bump around the same level as they have for the past two years and to accelerate sharply as prices find a new, lower level.

Additionally, there are trends where WBCP doesn’t have a position but continues to monitor their progress.

- Office occupancy has hit its nadir as work from home practices continue to be curbed and new businesses are headquartered in offices. At the same time, debt markets are generally unsupportive of additional building investment.

- Shipping prices are at multiyear lows.

- Technology layoffs have peaked.

- Advertising growth is likely to reaccelerate as US GDP continues to grow. With solid employment, a continuing return to work, and a tough environment for marginal capital expenditures, companies are optimizing the efficiency of their current assets by seeking additional demand. Additionally, 2024 is an election year in multiple Western countries.

- The price of oil is likely to be relatively stable with the price at approximately $90.

- The cost of Nvidia’s artificial intelligence state of the art processors has likely hit their high.

As always, feel free to reach out to discuss this or any of your investments at White Brook Capital. I thank you for your support and will strive to continue to earn your trust.

Sincerely,

Basil F. Alsikafi, Portfolio Manager, White Brook Capital, LLC

|

All investments involve risk, including loss of principal. This document provides information not intended to meet objectives or suitability requirements of any specific individual. This information is provided for educational or discussion purposes only and should not be considered investment advice or a solicitation to buy or sell securities. The information contained herein has been drawn from sources which we believe to be reliable; however, its accuracy or completeness is not guaranteed. This report is not to be construed as an offer, solicitation or recommendation to buy or sell any of the securities herein named. We may or may not continue to hold any of the securities mentioned. White Brook Capital LLC and/or their respective officers, directors, partners or employees may from time to time acquire, hold or sell securities named in this report. It should not be assumed that any of the securities transactions or holdings discussed were or will prove to be profitable, or that the investment decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein |

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here