Vista Energy, S.A.B. de C.V. (NYSE:VIST) is an independent oil & gas producer with its “Vaca Muerta” asset in Argentina recognized as the largest shale oil and gas basin under development outside North America. The company also has a working interest in a smaller Mexican concession.

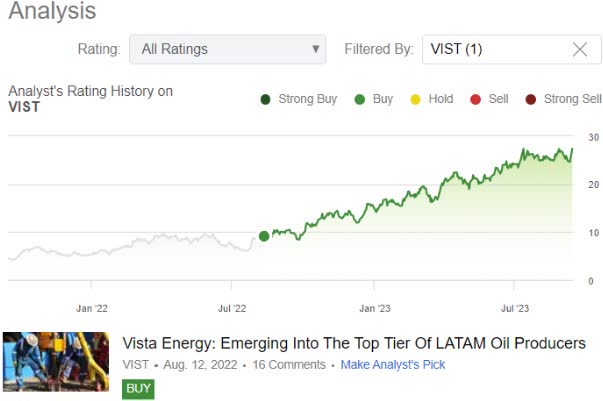

The company has attracted attention since its 2019 IPO with a combination of strong production growth, positive free cash flow, and overall solid fundamentals. Indeed, shares have been a big winner this year, climbing nearly 75% year to date amid a string of impressive results.

We last covered VIST back in 2022, pointing out how the company was emerging as a “top-tier LATAM oil name” while trading at a deep discount relative to peers. Fast-forward and our update today highlights how the share rally may have already incorporated many of those positives.

In our view, VIST is no longer materially undervalued, with valuation now turning as a headwind against further upside in the near term. Even considering the renewed momentum in oil prices more recently, we expect higher volatility from VIST going forward.

source: company IR

VIST Financials Recap

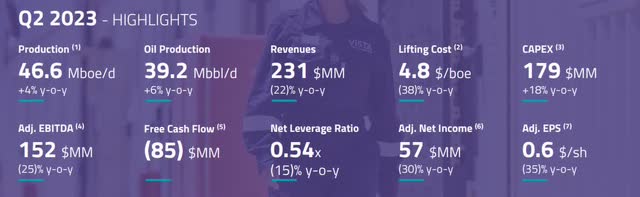

Vista last reported its Q2 results back in July. The headline figures included a 4% increase in total production between a higher oil output balancing a decline on the natural gas side. Considering the lower market pricing environment compared to the period in 2022, revenue of $231 million was down by -22% year-over-year, also resulting in a -25% lower adjusted EBITDA at $152 million. Adjusted EPS of $0.60, compared to $0.93 in Q2 2022.

source: company IR

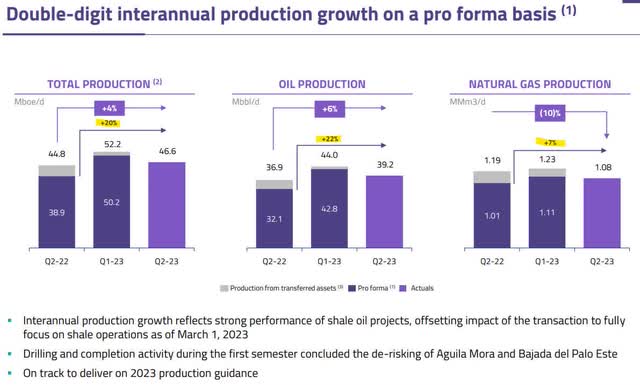

That being said, there were some important operational chances this year adding to some variability in the performance. Since the end of Q1, the strategy has been to shift the company’s production focus completely to shale assets. This included transferring some assets where Vista now only maintains a minority interest.

By this measure, the pro forma production results considering the core operation on a comparable basis paint a more favorable picture. Here, total production climbed by 20% y/y with oil production reaching 39.2 thousand barrels per day, up 22% y/y while pro forma natural gas production is 7% higher. The pure play on the shale profile has led to an improvement in the overall lifting cost, down -38% y/y.

source: company IR

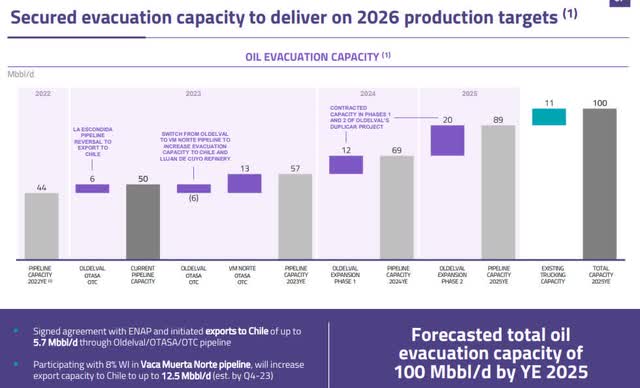

Key developments this quarter include the start of exporting oil to Chile through the “OTASA-OTC pipeline”. Management explains that the increased evacuation capacity is an important step to ultimately reach 2026 production targets.

There is also progress in its “Bajada del Palo Este” and “Aguila Mora” pilot projects. Successful testing has added up to 50 ready-to-drill wells for a total inventory of 1,150.

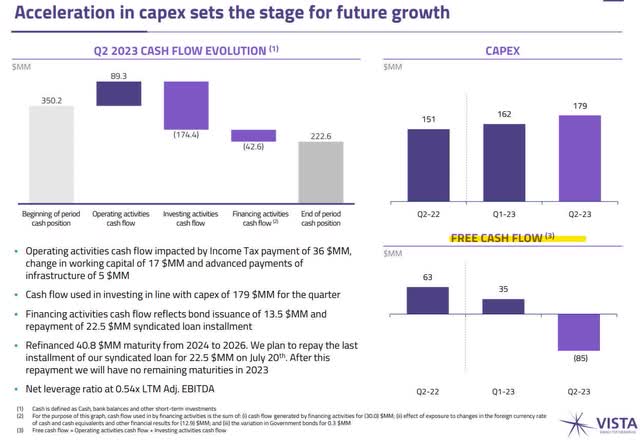

On the balance sheet, Vista ended the quarter with $223 million in cash against $651 million in total debt. Considering an annualized run rate of adjusted EBITDA above $600 million, net debt to EBITDA leverage ratio of 0.5x highlights the solid balance sheet.

What’s Next For Vista Energy?

A strong point for Vista is its Argentina operation and shale profile which offers attractive economics. The lower costs and even depreciated currency in the region are a big reason Vista captures low lifting costs and higher overall margins.

The plan is to continue expanding with a target to reach 100,000 barrels per day in evacuation capacity by year-end 2025. Compared to total production of 39.2 Mbbl/day in Q2, the path is to essentially double output through a broader midstream and export network over the next two years.

source: company IR

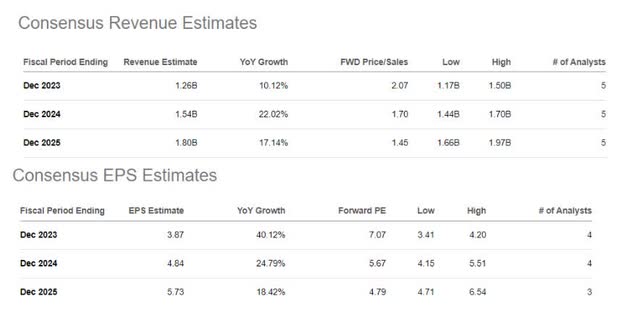

According to consensus, Vista revenues are expected to climb from $1.3 billion this year to $1.8 billion by 2025. From the 2023 EPS forecast of $3.87, the expectation is that there is room for earnings per share to reach $5.73 within the next two years.

Seeking Alpha

Naturally, these estimates are subject to changing market pricing. Oil has rallied from its 2023 lows in recent months, and the potential that there is further upside would translate directly into higher revenues and earnings.

At the same time, the understanding is that the necessary capex will climb from recent levels that naturally pressure free cash flow. While the top-line growth is positive, there is a case to be made that the accelerated spending adds to earnings uncertainties with incremental downside risks. There is also the scenario where energy prices simply lose momentum and reverse lower, which would further pressure the outlook.

source: company IR

Is VIST Undervalued?

While it was possible to find Vista Energy in early 2022 as something of a “hidden gem” or under-the-radar idea, it’s clear now that the secret is out. With shares more than tripling from their 52-week low, there’s an argument to be made that the market has already repriced VIST higher accordingly.

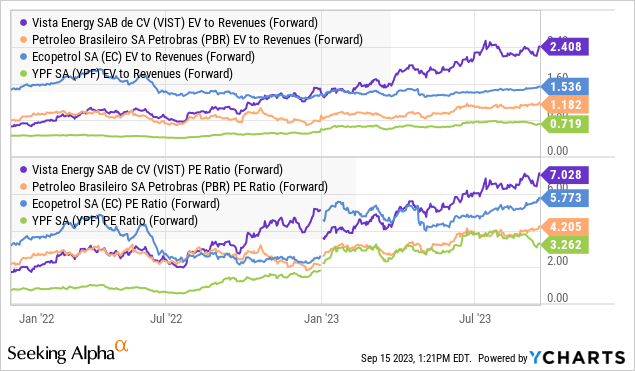

That dynamic can be observed across various valuation metrics. On an EV to revenue basis, VIST went from trading at a discount to names like Ecopetrol SA (EC) and Petrobras SA (PBR) this time last year to a wide premium at 2.4x on a forward basis currently. That’s also reflected in earnings premium, where VIST is trading at a 7x forward P/E multiple, compared to 6x for EC and 4x for PBR.

To be clear, there are some major differences with each of these Latam energy names. EC and PBR are state-owned, which adds a layer of political risk. There is also YPF SA (YPF), Argentina’s national oil company, which has faced deeper financial difficulties in recent years.

Those factors can justify some part of a discount relative to a non-state-owned enterprise like Vista Energy, but there are also advantages to the size and scale of companies like EC and PPR. In this case, those names are much larger and have a broader diversification including downstream activities. VIST stands out from this group as not distributing a regular dividend.

There are many moving parts here, but we don’t see a good reason Vista’s current valuation spread should necessarily widen significantly from here.

VIST Stock Price Forecast

We rate VIST as a hold, balancing our positive view of the company with a sense that valuation and shares have gotten a bit ahead of themselves. The stock was cheap in 2022, but it’s a new ballgame now. We believe there are simply better opportunities in the energy sector among beaten-down names and companies that can better leverage the upside in the price of oil.

From the stock price chart, VIST has been trading in a relatively tight range since the Q2 earnings report. We don’t see a good catalyst for shares to break higher beyond a major move in the price of oil. On the downside, a break below ~$24.00 would signal a more concerning technical sell signal.

Vista Energy has an investor day presentation on September 26, representing an opportunity for management to update on current conditions and the strategic plan ahead of the Q3 earnings report. While we don’t expect a major announcement, any financial targets will be key monitoring points.

source: company IR

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here