Introduction

Strong gross inflows have been what characterized the last quarter for the company as the AUM also rose to $161 billion in total. This puts Victory Capital Holdings Inc (NASDAQ:VCTR) to be one of the larger asset managers in the country and right now a very appealing investment opportunity. Despite being in the financial sector, the company was able to withstand a lot of the volatility that was felt earlier this year as two of the larger regional banks went under and caused a ripple effect.

The resilience of VCTR was seen and I think that the discount based on earnings of nearly 20% right now is making it a solid buying opportunity. Besides this, the company also has a very good dividend yield that I think will be able to be built upon further as VCTR continues to grow the AUM steadily. Furthermore, VCTR continues to buy back shares at a fast rate, and last quarter was a record for the business. In conclusion, I am rating VCTR a buy right now.

Company Structure

VCTR is as we know a part of the asset management and custody banks industry where it has been growing at a very decent rate the last few years and also quarters. VCTR functions as a prominent asset management company with a reach spanning the United States and international markets. The company’s operational landscape encompasses a variety of services, including investment advisory, fund administration, fund compliance, fund transfer agency functions, comprehensive fund distribution, and a range of other specialized management services.

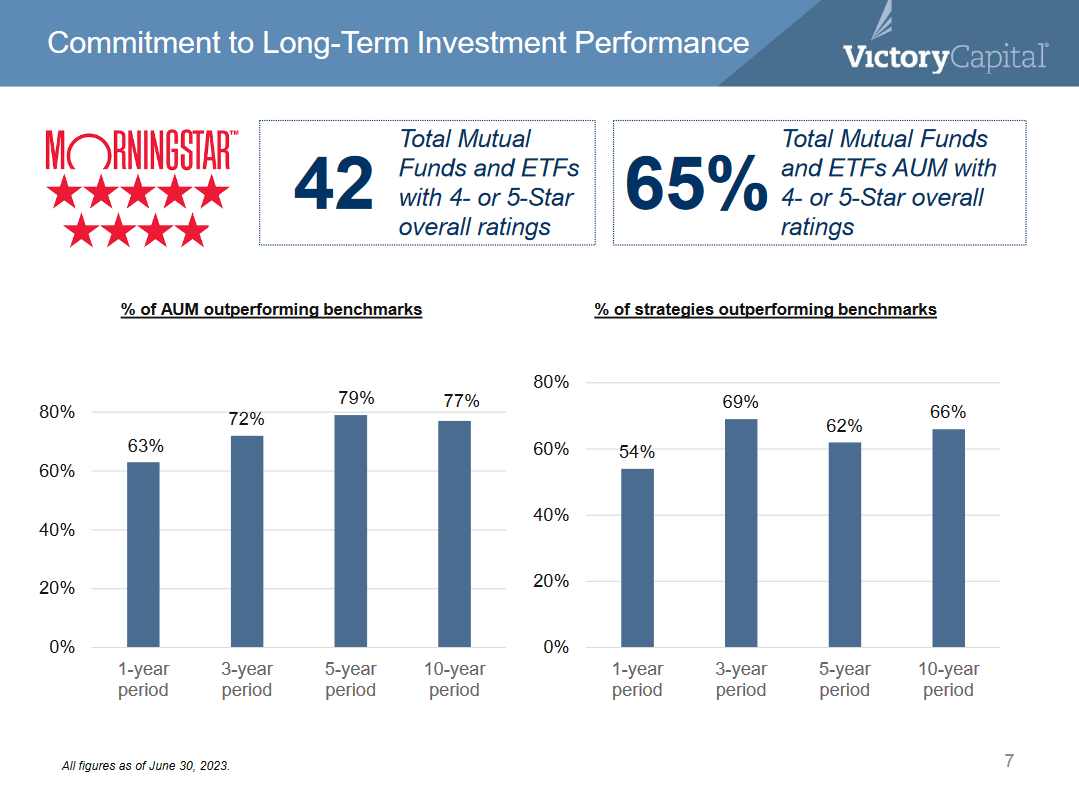

Long-Term View (Investor Presentation)

Relying heavily on growing the AUM to drive further growth, I think VCTR has so far done a very good job as they have been outperforming benchmarks as displayed in the charts above. This growth has landed the company able to diver further shareholder value as a strong dividend has been established and the momentum of buying back shares seems to accelerate as the valuation of the company is where I would consider it quite heavily discounted.

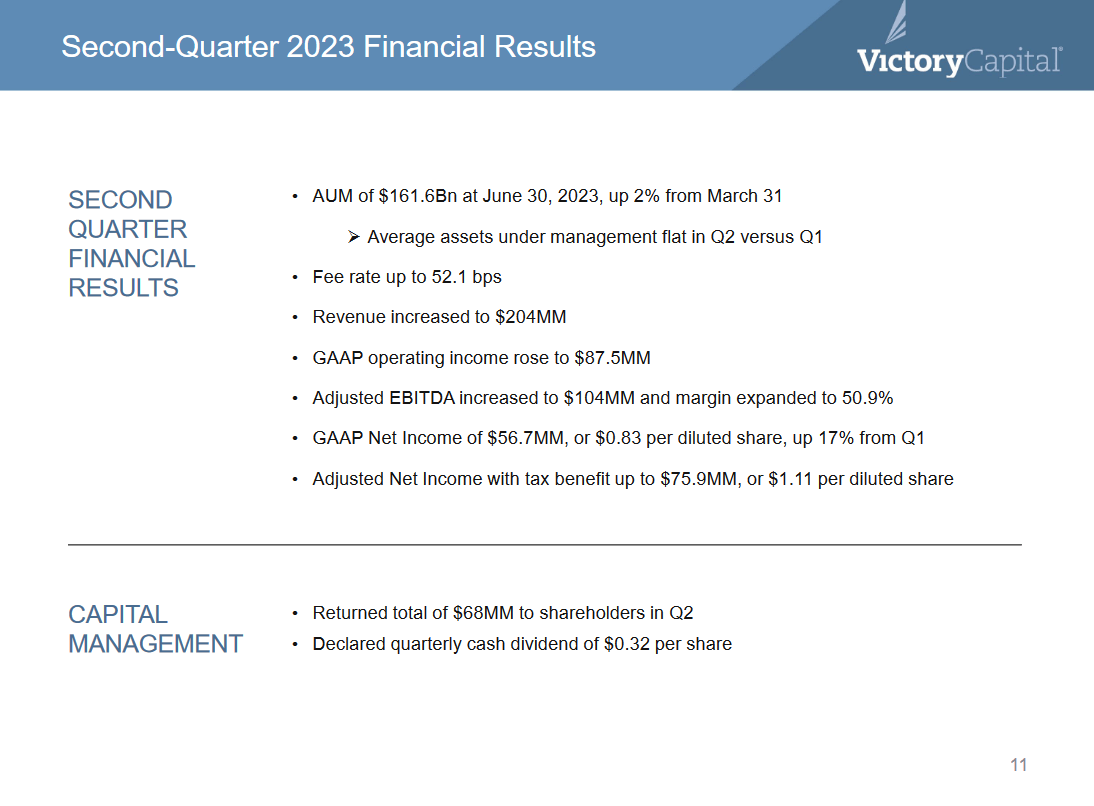

Q2 Results (Investor Presentation)

The last report showcased the strength of the business model and the ability to grow despite there being some significant economic slowdowns taking place and people are becoming more and more worried about where they are spending their money. In times like that though, VCTR has still been able to deliver a strong return for shareholders and deserves a buy rating as a result.

Earnings Transcript

From the last earnings call by the company, the CEO David Brown had some good comments on the recent performance and some valuable insight as well.

-

“Our margins remained exceptional, coming in at 50.9% this quarter, which highlights the differentiated nature of our operating platform and its highly variable expense structure. This is the 12th quarter in a row that we achieved margins above our long-term guidance of 49%. And this is the eighth quarter over that period where our margin surpassed 50%. Our long-term margin guidance remains unchanged at 49%. And keep in mind, this does factor in ongoing strategic investments that will help us grow our business in the future”.

With strong margin retention, I think that VCTR is further solidifying itself as a very good investment opportunity and a way to get exposure to the asset management industry. The differentiated and new platforms the company is investing in seem to be paying off very well and I expect to see this trend continue as VCTR continues to post better gross inflows and AUM growth in coming quarters as interest rates hopefully start to stabilize somewhat.

-

“A number of our products rose into the top quartile according to Morningstar’s trailing three year rankings. These include the Victory Income Investors Tax-Exempt Intermediate Term Bond Fund, Victory RS Global Fund, Victory RS Partners Fund and the Victory RS Investors Fund as well as the Victory Munder MidCap Fund and our emerging markets value momentum ETF. In total, approximately 43% of our mutual funds to ETF AUM is ranked in the top quartile as of June 30th”.

With a rise in popular, I think it will eventually start to become a snowball effect for the company as more eyes land on the company. If VCTR can maintain strong returns on the funds as well I think more inflows will happen and the investment thesis of VCTR being able to grow AUM will only strengthen.

Risk Associated

Looking ahead to the long term, the focal point of attention shifts to the challenges linked to the company’s potential to expand its AUM. The success of this endeavor hinges on the sustainability of enduring market trends favoring asset appreciation. Furthermore, it rests upon the company’s consistent ability to deliver compelling returns that are enticing enough to retain and attract investors in a competitive landscape.

Investments (Investor Presentation)

The company has made its investment strategies quite clear and some of them include ensuring they enter new markets and deliver on gaining market share and new clients and customers at a decent rate. If there prove to be some troubles along this way, then I think that the share price and valuation of the company will contract quite quickly. The data & analytics platform though I think should add some fuel to the growth as the further diversification of services and financial products will only be beneficial in the long term.

Investor Takeaway

VCTR has for a long time been characterized as an investment opportunity that hinges on its ability to grow AUM efficiently and generate a strong return to shareholders. So far I think the results speak for themselves and VCTR has done a very good job. The dividend seems sustainable and once interest rates go down, I don’t think it will harm the earnings of VCTR that much as hopefully more activity and inflows will offset that and ensure they can maintain their history of growing the dividend. I am also seeing VCTR trade at a very decent entry point right now with a 20% discount to the sector based on earnings alone. I would be happy paying an 8 – 9x earnings premium for the company and will therefore be rating it a buy right now.

Read the full article here