Investment Thesis

As investors, we look for stocks that trade below their true value. Viasat (NASDAQ:VSAT) is one such stock that caught our eye. The stock, which is now trading at around $20, has lost half of its value since its Viasat-3 satellite incident last July. The stock’s valuation ratios seem very appealing at these levels, so we decided to do a thorough analysis of Viasat’s business and financials to see if there any value traps.

What we have found is that Viasat has a strong growth potential due to its superior satellite technology, diversified revenue streams, strategic partnerships, and cost-saving initiatives. However, Viasat also faces some challenges such as intense competition, high debt management and costly satellite failures. Viasat has the technology and strategy to deal with these challenges and therefore we are optimistic about the company’s positive outlook and its goal to grow and generate positive cash flow by 2025.

We rate Viasat as a Buy with a price target of $30.

Company Overview

Viasat is a satellite broadband and secure networking solutions provider that operates across the globe through three segments: Satellite Services, Commercial Networks, and Government Systems. The company completed its acquisition of Inmarsat during its Q4 2023 quarter, becoming one of the largest satellite operators in the world.

However, Viasat faced some serious setbacks in its satellite operations few months ago. Company’s newest satellite, Viasat-3 F1, faced an antenna issue and became malfunctional while it was ascending to its orbit. The stock price plummeted 30% after the incident since there was speculation that the satellite would be a total loss.

The importance of Viasat-3 F1 satellite is that it is part of the new Viasat-3 network, which is vital for Viasat’s future growth plans. The Viasat-3 network was designed to add more capacity to Viasat’s current fleet, which was struggling with bandwidth limitations especially in the Americas.

Viasat has recently announced that the satellite payload is functional, but it expects the constellation to handle “less than 10 percent” of its planned throughput. Despite this, Viasat is not planning to replace the satellite, saying that it can adapt the system to mitigate the lost capacity.

Market Opportunity

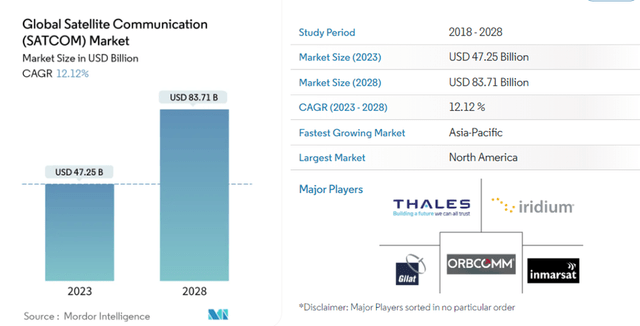

Satellite communication is a booming market that is expected to more than double in size from USD 47.25 billion in 2023 to USD 83.71 billion by 2028, growing at an impressive CAGR of 12.12%.

Global Satellite Communication Market (Mordor Intelligence)

One of the major drivers of this market is the increasing adoption of IoT and autonomous systems in the industrial sectors. According to Ericsson, the number of massive IoT connections will reach close to 200 million by the end of 2027, and 40% of cellular IoT connections will be broadband IoT, mostly using 4G. Moreover, the number of short-range and wide-area IoT devices will reach 22.4 billion and 5.2 billion respectively by the end of 2027. These trends show that the market for satellite communication is growing rapidly, as there is increasing demand for connectivity and data transmission from the expanding number of IoT and autonomous devices.

Business Strategy – Positioned for Growth and Positive Free Cash Flow

We are very optimistic about Viasat’s long-term growth potential in the Satellite Communications market for several reasons.

First of all, Viasat has a very unique and comprehensive portfolio: it has 19 satellites in different frequency bands (Ka-, L- and S-) that can offer high-speed and reliable services for various markets, such as maritime, aviation, government and consumer. We see that Viasat doesn’t want to compete with Starlink for residential broadband customers in the LEO space, but rather wants to focus on becoming a global mobile service provider that caters to government and enterprise customers with unique offers.

Viasat is also deploying its next-generation network, called Viasat-3, which is an impressive project that will offer near global coverage to its customers around the world, especially in underserved and unserved areas. Although Viasat-3 F1 will only be able to provide 10% of its capacity due to its deployment failure, mitigation will be provided by the other 2 satellites that company plans to launch in 2024 and 2025. In our opinion, Viasat-3 will further enhance Viasat’s competitive advantage and become a key growth lever for the company.

Viasat-3 Constellation (Viasat)

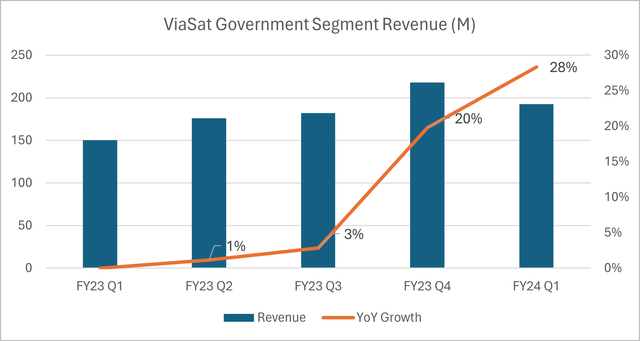

Viasat’s diversified business strategy is another key lever we think. The company has diversified and resilient revenue streams across its three segments: government systems, commercial networks, and satellite services. The government systems segment provides secure communications and networking solutions to the U.S. and allied governments. This segment was the fastest growing segment in Q1 FY2024 with 28% YoY comparable revenue growth and shows an accelerated revenue trend, as illustrated below. We believe this segment will lead the business growth and profitability of Viasat in the next several years.

Viasat Government Segment Revenue (Author)

The commercial networks segment develops and produces satellite and wireless network infrastructure and ground equipment. This segment’s plan is to grow in the global mobile services market and focus especially on enterprises, airlines solutions, maritime, connected cars, trains and other value added services.

We also appreciate Viasat’s partnerships and acquisitions strategy that enhance its capabilities, reach and scale. A prime example is the $7.3 billion deal to acquire Inmarsat, which combines two leading satellite operators with different orbits and frequencies. This will allow Viasat to offer a multi-layered network with better scale and coverage. And we believe this will also create various synergies for the company.

Viasat Inmarsat Acquisition (Viasat)

The company also has a balanced mix of recurring and non-recurring revenues, which helps it mitigate the impact of market fluctuations and uncertainties. Overall, we think that the company’s business is strategically positioned to leverage its core competencies in the growing satellite communications market. If the strategy is executed successfully, we expect Viasat to achieve its ambition of positive free cash flow by 2025.

Revenue Growth – High Single Digits Expected

Viasat reported revenue of $780 million for the first quarter of fiscal year 2024 (36% increase YoY). This number includes Inmarsat’s one-month revenue contribution of approximately $134 million. The combined revenue estimate, including the pre-acquisition period, would have been about $1 billion, an increase of about 11% YoY. This means both companies achieved double-digit revenue growth YoY which we see as a very positive sign.

Looking in the segment performances, the revenue growth was driven by strong demand for Government Systems and Satellite services segments.

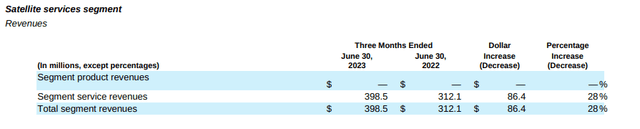

However the growth in the Satellites Services (see below) came from Inmarsat acquisition ($86M contribution)

Satellite Services Segment (Viasat 10-Q)

If we exclude Inmarsat, the Satellite Services revenue would have been flat. Although IFC (In-Flight Connectivity) business is growing, the US fixed broadband is showing weakness and Viasat is allocating greater portion of the available bandwidth to the growing IFC business as per their 10-Q report.

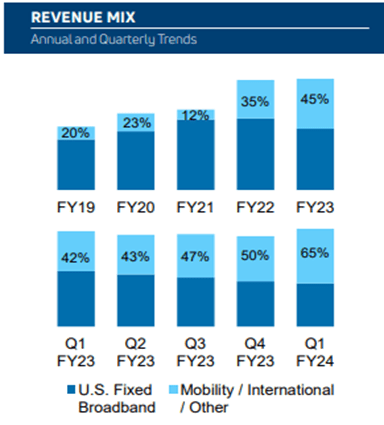

Satellite Services Segment Revenue Mix (ViaSat Q1 FY24 Shareholder Letter)

As we mentioned earlier, Viasat’s strategy is to target the global mobile services market instead of the fixed broadband market. This is reflected in the segment revenue mix as well. US fixed broadband revenue is dropping every quarter and global mobility now accounts for 45% of the Satellite Services Segment. We anticipate that this segment will keep growing as the mobile services market expands rapidly.

When we look at the government systems segment (see below), we see strong demand and we believe that this segment will be a key growth driver for Viasat. Viasat says in their quarterly reports that both government and defense related products are in high demand and have healthy backlogs. The revenue trajectory indicates us that this segment can sustain double-digit growth for the next several years.

Government Systems Segment (Viasat 10-Q)

The revenues of the commercial networks segment (see below) rose by $35.8 million (32% YOY) due to the sales of mobile broadband satellite communication systems products, which were driven by higher IFC terminal shipments.

Commercial Networks Segment (Viasat 10-Q)

Viasat expects its revenue to grow at a high single-digit rate for the fiscal years 2024 and 2025. Based on our analysis of the three business segments and their trajectories, we do not see any major obstacle that would prevent Viasat from achieving this growth rate.

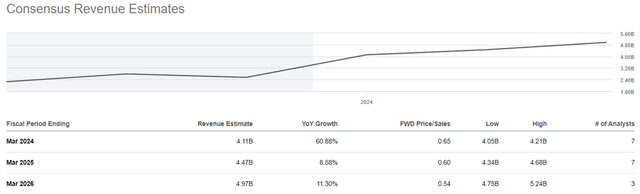

When we look at the consensus revenue estimates (see below) we see that they are aligned with our growth projections as well.

ViaSat Consensus Revenue Estimates (Seeking Alpha)

Synergies Will Lower Expenses and Improve Operating Income

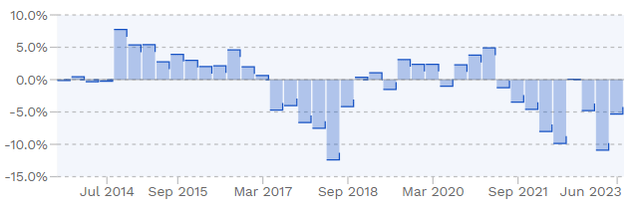

Viasat reduced its operating loss to $41.5 million in the first quarter of FY24, compared to $56.6 million last year. The company’s operating margins have been negative for several quarters, as shown below, due to high operating costs related to the acquisitions, increased R&D and SGA expenses. However, the company expects to improve its operating margins by achieving synergies from the Inmarsat acquisition, which says will lower its operating and capital expenses.

ViaSat Operating Margins (Finbox)

The company recently announced that it will save about $80 million annually in operating costs and about $110 million annually in capital spending by FY25, which is faster than initially expected. This is a positive development and we think that Viasat will find more opportunities to reduce costs and improve operating margins in the future.

Debt Looks Manageable

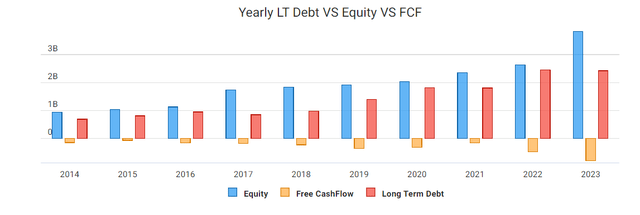

Viasat has a relatively high debt/equity ratio of 1.22, which means it relies more on debt financing than equity financing. However, its liquidity position is strong and has improved significantly in the last quarter.

ViaSat Yearly LT Debt vs Equity vs FCF (Chartmill)

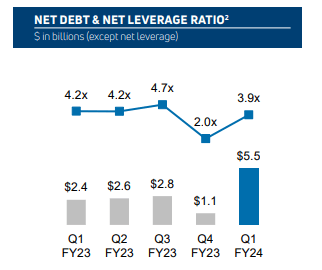

The company closed the sale of its Link-16 Tactical Data Link (‘TDL’) business in Q4 FY2023, which increased its liquidity to $3.5 billion and its current ratio to 2.2 in Q1 FY2024. This shows us that Viasat can easily meet its short-term obligations.

Net Leverage Ratio (ViaSat Q1 FY24 Shareholder Letter)

The company’s capital structure may seem highly leveraged, but we believe that the debt is manageable. The leverage ratio of 3.9 is not too high, considering the sustained EBITDA growth and no near-term debt maturities. We do not have any major concern for Viasat to manage its debt.

Valuation

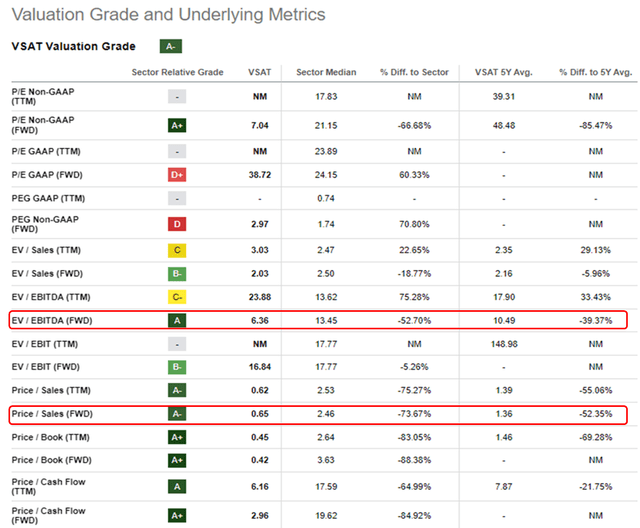

When we look at the multiples we see very attractive valuations for Viasat. Its EV/EBITDA (fwd) and Price/Sales (fwd) ratios are quite below the sector median values indicating significant upside potential.

Viasat Valuation Metrics (Seeking Alpha)

–

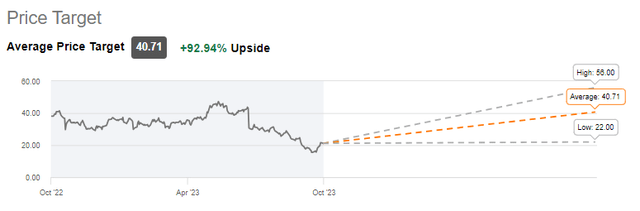

Also we see that Wall Street analysts have an average rating of Buy and a consensus price target of $41 for Viasat. The most recent analyst upgrade was from J.P. Morgan , who upgraded Viasat to Overweight with a price target of $30.

Wall Street Price Target (Seeking Alpha)

We believe that Viasat deserves at least a 10x EV/EBITDA (fwd) multiple, based on the various opportunities and risks that we see in the business. This valuation implies a substantial upside potential for Viasat, with a target price of $30.

Risks

We have identified the following possible business risks for Viasat.

Intense Competition From Other Operators

Viasat faces intense competition from other satellite operators, terrestrial service providers and emerging technologies that offer similar or alternative services to its customers. Viasat’s competitive advantage depends on its ability to differentiate and expand its portfolio with new products. We see this as a medium risk for Viasat and think that Viasat should continuously develop new strategies and technologies to mitigate competition.

Costly Satellite Failures

Viasat’s services depend on the performance and availability of its superior and costly satellites. These assets could be disrupted, failed or degraded, which could affect Viasat’s service quality, customer satisfaction and business results. A similar incident like the recent VS-3 F1 failure would be devastating for Viasat’s business. We think this is a low-to-medium risk as we believe that company has learned from the failures and will implement extra controls and remedies to prevent similar problems.

Possible Financial Distress

Viasat has a lot of debt that requires a lot of positive cash flows to pay off. Viasat’s ability to pay its debt and other obligations depends on its future performance, cash generation and access to capital markets. We think this is a low-to-medium risk as its share price already reflects this and we think that Viasat has the necessary financial discipline in place.

Conclusion

In conclusion, our analysis of Viasat’s investment potential reveals a compelling opportunity despite the challenges it faces. The company’s recent setbacks, notably the Viasat-3 F1 satellite incident, raised concerns, but Viasat’s strategic initiatives and unique market position indicate a positive trajectory. With a robust portfolio, diverse revenue streams, strategic acquisitions like Inmarsat, and the ongoing deployment of Viasat-3, the company is positioned for growth in the expanding satellite communications market.

Considering these factors and the favorable valuation metrics, we rate Viasat as a Buy, with a target price of $30, representing almost 60% upside potential.

Read the full article here