Investment Thesis

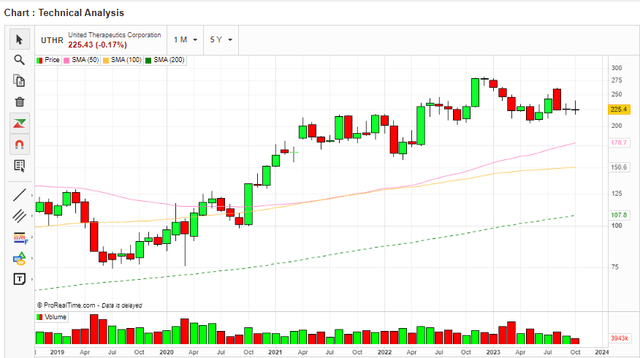

United Therapeutics Corporation (NASDAQ:UTHR) has been in a long-term uptrend since 2019, making higher highs and higher lows. The stock broke out of a consolidation pattern and reached a new all-time high of $283.09, its current 52-week high. This indicates that the bulls are in control, and there is strong demand for the stock. From a technical analysis point of view, the company appears to be on a solid upward trajectory with no signs of a reversal.

I am bullish on this stock from a technical and fundamental standpoint. The company’s solid financial performance, which includes attractive profitability and growth metrics, backs up my bullish stance. Furthermore, the company’s competitive advantage in its niche market, which stems from its diverse array of approved products, will, in my opinion, acts as a significant growth lever. Another factor worth noting that I believe will be a significant long-term growth driver is the projected market growth, which speaks well for the company’s top and bottom lines. The biotechnology market is projected to grow at a CAGR of 12.8% between 2023 and 2030, which, in my opinion, is solid growth and bodes well for UTHR, given its competitive advantage in the industry. Given this background, I am upbeat about UTHR and recommend it to investors.

Fundamental Analysis: Solid And Reassuring

To cover UTHR fundamental analysis, I will focus on several aspects. To begin with, is its competitive advantage. The company has a strong competitive advantage in its niche markets, as it has a diversified portfolio of approved products, such as Remodulin, Tyvaso, Orenitram, Unituxin, and Adcirca. I believe its products serves as a major competitive advantage because it allows the company to address the unmet medical needs of patients with rare diseases, such as pulmonary arterial hypertension, neuroblastoma, and organ transplantation.

Further, the company’s products consist of prostacyclin analogs, a phosphodiesterase type 5 inhibitor, and a monoclonal antibody, which have different mechanisms of action and delivery methods, offering convenience, variety, and quality to patients and physicians. Furthermore, its products are protected by patents and enjoy regulatory exclusivity, which reduces the threat of generic competition. To explain how unique the company’s products are, I will focus on a few examples given below;

- Orenitram: This is an oral formulation of treprostinil that can be taken with or without food. Orenitram is the first and only oral prostacyclin analog approved for PAH treatment.

- Unituxin: It is a monoclonal antibody that binds to a specific protein on the surface of neuroblastoma cells and triggers an immune response to destroy them. Unituxin is the first FDA-approved immunotherapy for high-risk neuroblastoma, a rare and aggressive form of childhood cancer.

In my opinion, this diverse and unique product portfolio serves as a major competitive advantage and is the driving factor behind the company’s solid financial performance in terms of revenues and profits. I believe with such a strategy, the company will maintain its strong financial position in the long run, as well as increase customer retention and satisfaction. Additionally, I believe the company is in a prime position to exploit the growing market with its diverse and unique products, painting a very bright outlook for the company.

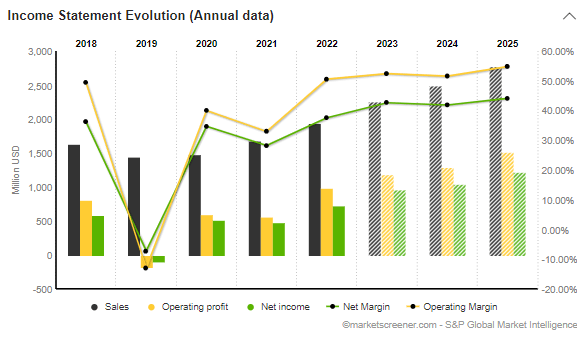

Another aspect of the company’s fundamental analysis is its consistent growth in revenue and profitability over the past years, which has been driven by increased demand for its products and the growth of its market share and customer base. The company reported a revenue growth of 27.76% year-over-year to $596.5 million and an earnings growth of 51.4 year-over-year to $5.24 per share for the second quarter of 2023. It also beat the analysts’ consensus estimate of $4.78 per share by a margin of $0.46. Revenue beat estimates by a margin of $72.33 million. In my view, this sums up a strong financial performance over the years, as shown below.

Market Screener

Another aspect is the company’s solid balance sheet. UTHR has a market cap of $10 billion and a total debt of $800m. With a debt-to-equity ratio of 14.78%, the company has very low leverage, which is very reassuring because it translates to a very low debt risk. Further, the company has a solid liquidity position with a cash balance of $2.68 billion, which covers its total debt 3.35x. It also has a current ratio 8.68x. Looking at this liquidity position, the company’s solvency is guaranteed, which is very encouraging. Further, this balance sheet gives the company a lot of financial flexibility, which it can exploit to leverage on emerging opportunities.

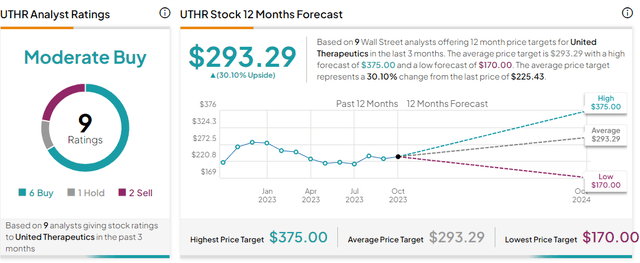

Lastly, the company has a low short interest of 2.23% of its shares sold short, indicating that investors are not betting against the stock. Based on this information, I think that UTHR is a good value stock to buy now in 2023, as it has strong fundamentals. To back this claim is a moderate buy consensus rating from 9 Wall Street analysts, with an average price target of $293.29, representing a 30.1% upside from its current price of $225.43. The highest price target is $375.00, and the lowest is $170.00.

Tipranks

This bullish projection is consistent with my upbeat viewpoint and a price target of $267.77, as described in the technical analysis section. My price target translates to an 18.78% upside potential.

Market Potential: A Major Long-term Growth Catalyst

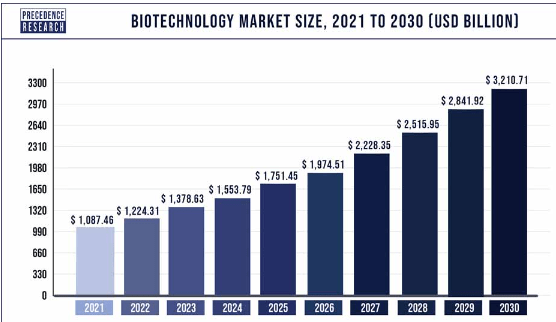

UTHR operates in the biotechnology industry, which is expected to grow rapidly, creating a significant growth opportunity for the company. The global biotechnology market was valued at $1,224.31 billion in 2022 and is anticipated to be worth roughly $3,210.71 billion by 2030, with a 12.8% CAGR from 2023 to 2030.

Precedence Research

Given this strong projected market growth, I believe that UTHR is better positioned to capitalize on the opportunity, given the company’s solid fundamentals. Specifically, I expect its competitive advantage stemming from a unique and diverse product portfolio to earn the company a significant market share and customer base in this growing industry. Further, its innovativeness, as illustrated by its unique products, some of which are the first and only products registered to address specific conditions, will help the company develop new products that can address dynamic customer needs. Above all, its robust balance sheet, in my opinion, provides the company with substantial financial flexibility, which it can leverage to invest in the expanding industry. In a nutshell, I have a bright outlook for UTHR in light of the projected market growth and expect it to maintain and even improve its top and bottom line in the long run.

Technical Analysis

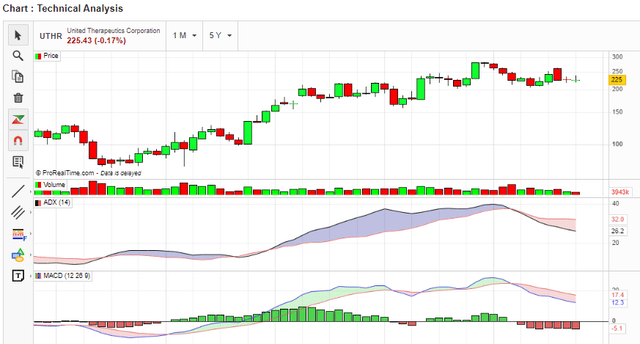

In this section, I will discuss UTHR’s technical analysis using several indicators. First, consider the UTHR price trend. Since 2019, the stock has been in a long-term uptrend, with higher highs and higher lows. The stock broke out of a consolidation pattern and hit a new high of $283.09. This suggests that the bulls are in command and that the stock is in high demand.

Author Analysis On Trade view

The other indicator is the moving average convergence divergence [MACD]. The MACD of UTHR is currently above the signal line and above zero, which suggests a bullish momentum and a positive trend. Moreover, the MACD is not showing any signs of divergence with the price, which means that the trend is not losing steam. To complement MACD is the trend strength is the average directional index [ADX]. The ADX also has two components: the positive directional indicator (+DI) and the negative directional indicator (-DI), which show the direction of the trend. A buy signal occurs when +DI crosses above -DI, while a sell signal occurs when -DI crosses above +DI. The ADX of UTHR is currently around 32, which indicates a moderately strong uptrend. The +DI is also above the -DI, which confirms the bullish direction.

Author Analysis On Market Screener

Further, the stock is trading above its 50-day, 100-day, and 200-day simple moving averages [SMA], which are rising and act as support levels for the price. This indicates that the stock is in an uptrend and has a positive momentum.

Author Analysis On Market Screener

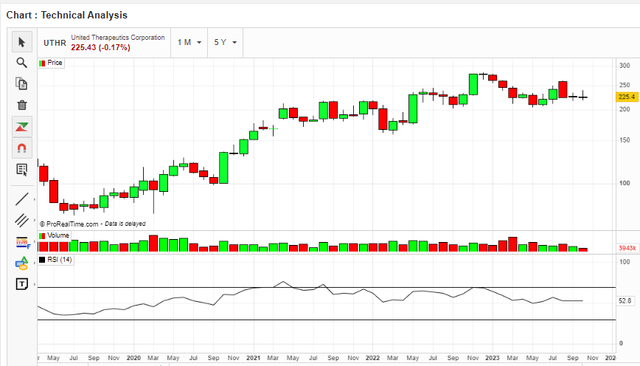

Additionally, the relative strength index [RSI] is above 50(at 52.8) and rising, which indicates that the buyers are in control and the stock has more room to grow. The RSI is not yet in the overbought territory of 70, which means the stock will not likely face a reversal soon.

Author Analysis On Market Screener

Lastly, the stock has broken out of a symmetrical triangle pattern, which is a bullish continuation pattern that suggests a further upward movement of the price. The breakout target is calculated by adding the height of the triangle to the breakout point, which gives a potential price of $267.77.

Author Analysis On Trade View

The potential price is my new target, representing an upside potential of about 18.78%. Given its solid fundamentals and projected market growth, I believe the stock can exploit this potential. Based on these technical analysis tools, UTHR seems to have a strong upside potential in the future. The stock has shown bullish patterns, indicators, and oscillators that indicate a continuation of its uptrend and a possible breakout to new highs. It is for this reason that I recommend the stock to potential investors.

Risks

Although I am bullish on this stock, there are some risks associated with investing in this company. Here are some of the risks. First are the technological and operational risks that could result from launching, operating, and maintaining a complex network of satellites and ground stations. The company is developing organ transplanting technologies that rely on satellite communications to enable remote monitoring and control of bioreactors. Its satellite network is subject to various risks and uncertainties, such as launch failures, malfunctions, interference, cyber-attacks, or natural disasters. The company could also face technical challenges or delays in developing, testing, and deploying its organ manufacturing technologies.

The other risk is competition. The competitive risks could result from the emergence of new or improved products or services from other satellite and terrestrial communications providers. Although the company enjoys a great degree of competitive advantage due to patents and innovation, other companies can develop superior products that can eat UTHR’s market share and customer base.

My Investment Take

Based on this analysis, UTHR is a good value stock backed by solid fundamentals. The company’s strong financial performance and position bodes well for the company’s solvency and ability to finance future developments, especially in light of the strong projected market growth. Guided by the technical analysis, UTHR is a robust upward trajectory, which I expect to be sustained by its solid fundamentals. For this reason, I expect the company to exploit my double-digit projected upside potential. Given this background, I recommend the stock to potential investors seeking a good value opportunity in the biotechnology industry.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Best Value Idea investment competition, which runs through October 25. With cash prizes, this competition — open to all contributors — is one you don’t want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

Read the full article here