Introduction

UGI Corporation (NYSE:UGI) is a leading American company operating in several segments throughout the United States and Europe. The company distributes, stores, and transports energy products and services through its business territories. UGI’s main operations are in four business segments: AmeriGas Propane, UGI International, Midstream & Marketing, and Utilities. In my previous article, I investigated the company’s operations in each segment, and based on their several investments and initiatives in several agreements, I concluded that I saw improvement in their future operations. However, in this article, I have investigated UGI’s capital structures as well as its leverage and liquidity conditions, and as a result believe it should make leverage and liquidity improvements as their first priority to prevent future risks.

UGI business outlook

The natural gas business of UGI, which contains its utilities business and midstream assets, produces more than 60% of the company’s earnings. It is worth noting that in the utilities segment, UGI is the second-largest regulated gas utility in Pennsylvania and the largest gas utility in West Virginia. Moreover, approximately 84% of UGI’s midstream income is fee-based through minimum volume commitments and take-it-or-pay-it agreements. Furthermore, AmeriGas Propane distributes propane to residential and commercial customers.

It is worth mentioning that UGI has engaged Goldman Sachs & Co. LLC, and J.P. Morgan Securities, LLC, as the advisors because the company is willing to evaluate some potential alternatives associated with its LPG business. The goal of this process is to reduce UGI’s earnings volatility and improve the strength of the balance sheet by optimizing the company’s cost structures. As there has been no result of this review yet and the explanations about it are vague, I assume we need to wait and see, albeit the company generated an attractive dividend growth of 7.2%, which was higher than their long-term target of 4%.

Recently, the company observed lower retail volume and higher operating and administrative expenses due to the heat wave in the West of the U.S. in the first half of 2023, which caused lower AmeriGas Propane sales and margins. As a result, the Pennsylvania utility implemented a weather normalization rider and higher base rates to improve revenues. Overall, the company expects volume growth at AmeriGas in the future. Also, the management plans to focus on cost structure in the current quarter to make the company more stable against weather impacts and volume pressure.

UGI financial outlook

By the end of 3Q 2023:

- AmeriGas experienced flat EPS records in comparison with the same time last year. Thanks to higher margins that could partially offset increased operating and administrative expenses. Also, LPG volumes were down 6% due to continued lower fuel demand, customer attrition, and continued structure of conservation.

- Notwithstanding higher LPG margins, lower non-core energy marketing earnings caused a $0.01 decline in the EPS of UGI International. However, their LPG volumes were up 2%.

- Midstream in marketing’s EPS was down $0.01.

- Higher operating and administrative expenses caused the EPS of the utility segment to become lower than the prior year.

Regarding the management’s future growth expectations, we should notice that they recorded a pre-tax non-cash goodwill impairment charge of circa $660 related to AmeriGas. Goodwill impairment happened because the fair value of AmeriGas has become less than its carrying amount. As a result, the management anticipates future cash flows and overall financial performance of AmeriGas are likely to be lower than their previous expectations. The main reason behind this is related to higher discount rates, as discount rates are the crucial element in calculating the present value of future cash flows. The current interest rate environment boosts the cost of capital, hence making the fund of future cash flows more expensive. Consequently, the future cash flows of AmeriGas are worth less in today’s terms, and we should expect a further fall in the fair value of this segment.

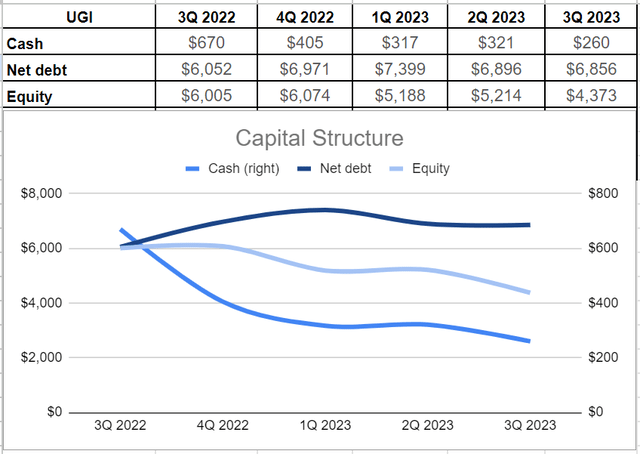

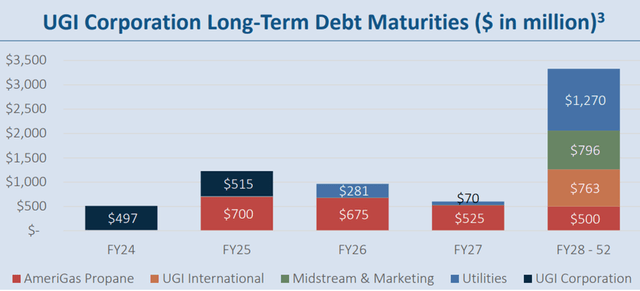

As Figure 1 illustrates, UGI holds more than $6.8 billion of net debt, and it is worth mentioning that several of its debts are due by the end of 2026 (see Figure 2). According to their equity level, which declined by 16% to $4.3 billion versus $5.2 billion at the end of the second quarter, it seems that the credit facility is the main source of liquidity for the company, more than 83% of their liquidity has been related to credit facilities by the end of the recent quarter.

UGI Corporation has offered a long history of dividend payments, with 36 years of dividend growth in a row, thanks to its constant earnings growth. The company’s current dividend yield of 6.7% is appealing. However, in the current high-interest rate environment, high debt levels will cause more interest expenses for the company. For example, their interest expenses grew by 17% in the third quarter of 2023 compared with the same time in the prior year. Moreover, UGI’s earnings will likely grow more slowly as their forward EPS growth is expected to decline, with a payout ratio of around 50%, which is likely to lead to less growth in dividend payments. Therefore, their current dividend levels do not seem as safe going forward. It is worth mentioning that the management’s priority is to strengthen the balance sheet. They refinanced the 2024 bonds at AmeriGas and thus reduced circa $200 million of debt at AmeriGas.

Figure 1 – UGI’s capital structure (in millions)

Author

Figure 2 –

UGI Presentation

UGI financial performance

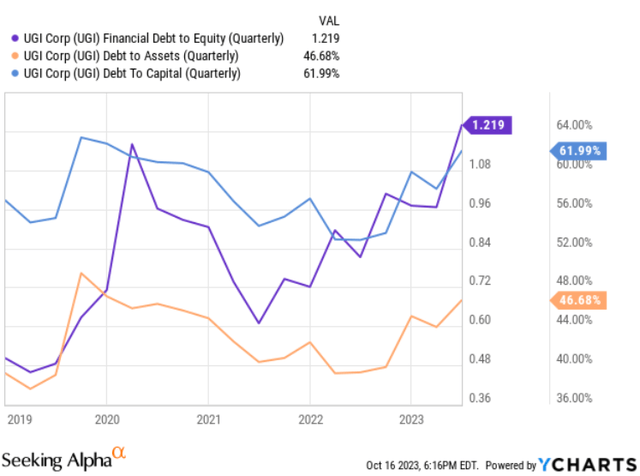

Propane is a super volatile business because it is affected by warmer weather, which lowers demand volumes and the supply and demand of both natural gas and crude oil. Analyzing UGI’s leverage condition indicates that the company should improve its leverage condition in my opinion. In minutiae, after the downturn of 2020, when the leverage ratios sat at high levels, the company could improve its condition gradually. However, challenges like the Russia and Ukraine war, warmer-than-expected winter, energy conservation efforts in Europe, higher inflation rates, and the current interest rates environment caused the company’s leverage ratios to almost hit their 2020 peaks. UGI’s debt-to-capital ratio is circa 62%, which shows that 62% of the company’s capital is funded by debt. Moreover, its debt-to-asset ratio has surged considerably since last year, reaching over 46%. Ultimately, UGI’s debt-to-equity ratio is 1.2x, which indicates for every $1 of equity or ownership, the company has $1.2 debt. This ratio is higher than approximately 1.1x in 2020 (see Figure 3).

Figure 3 – UGI’s leverage condition

YCharts

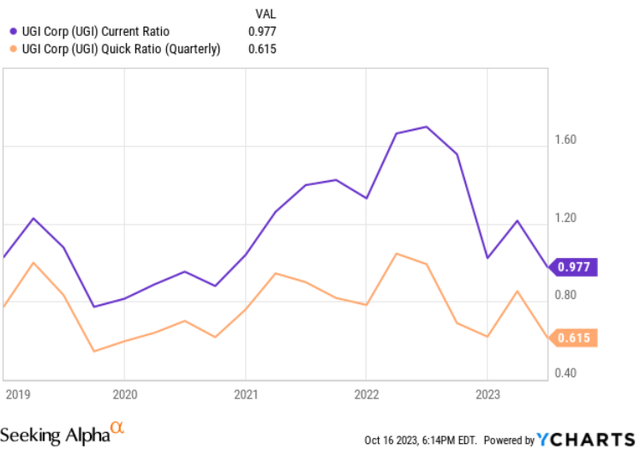

Furthermore, the company’s liquidity ratios are almost as low as the downturn of 2020. As it is demonstrated in Figure 4, UGI’s current ratio plunged to 0.97x, which is far lower than its level of approximately 1.7x in mid-2022. Moreover, the company’s quick ratio sat at 0.6x, which is far lower than the same time in the prior year and almost the same as 2020.

Figure 4 – UGI’s liquidity condition

YCharts

As a result, the company’s current liquidity condition has become their first priority as the management stated:

“We’re really focused on improving the balance sheet and making sure that we have the appropriate liquidity when we are going to be looking and looking at potential M&A. So, M&A is always a part of our strategy, we’re always looking at opportunities that come through, but at this present time we are very focused on improving balance sheet.”

Final notes

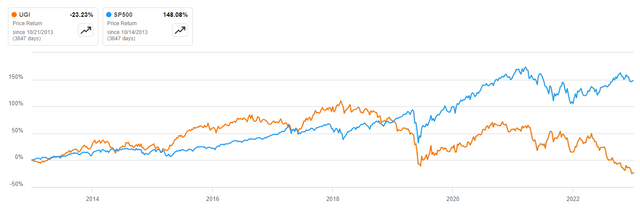

When all was said and done, although UGI has offered an attractive dividend payment historically, the company’s current financial position shows that there might be alternative profitable investment decisions for both income and growth investors. The management has introduced a strategic review of its business. They decided to evaluate some potential alternatives associated with their LPG business. The goal of this process is to reduce UGI’s earnings volatility and improve the strength of the balance sheet by optimizing the company’s cost structures. However, the results of this strategy are not clear yet. Moreover, the company’s leverage and liquidity conditions require serious improvements as they almost reached the same conditions of the downturn of 2020. Finally, comparing UGI’s return with the S&P 500 during the last ten years shows that the company had outperformed the S&P 500 before the pandemic, while after the pandemic, its price return has become far lower than the S&P 500 (see Figure 5).

Figure 5 – UGI’s price return vs. S&P 500

Seeking Alpha

As a result, I downgraded my previous rating to a hold for UGI stock.

Thank you for your time, and as always, I welcome your opinions.

Read the full article here