By James Knightley

Wealth gains led by stocks and housing

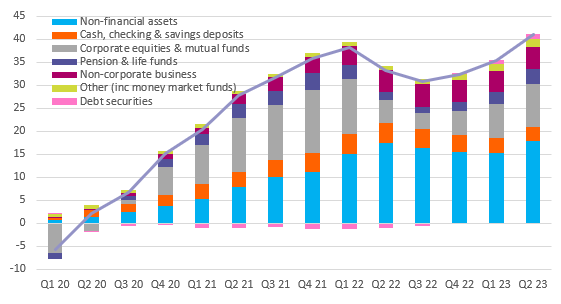

The net wealth held by US households increased by $5.5tn in the second quarter, according to data released by the Federal Reserve. The total value of assets held by the household sector rose to $174.4tn while liabilities rose just $170bn to $20.1tn, leaving net household worth at $154.3tn.

Rising equity market prices were a key factor, with corporate equity and mutual fund holdings rising $2.15tn in the quarter. Meanwhile, a partial recovery in home prices, caused by a dearth of supply of homes for sale offsetting the drop in demand in response to surging mortgage rates, meant non-financial asset holdings increased $2.6tn. The value of debt securities, pension and life funds and non-corporate business all increased as well, with holdings of cash, checking and time savings deposits the only component to post a decline – of $200bn.

This means that the value of financial assets held by the household sector, after initially being dragged down by a sharp drop in equities in the first quarter of 2020, stands $41.1tn above pre-pandemic levels while the amount of liabilities – primarily mortgages but with consumer credit accounting for more than a quarter – is up $3.5tn on fourth quarter 2019 levels.

Cumulative Increase in value of assets held by US households since December 2019 ($tn)

High wealth levels should be a buffer against economic headwinds

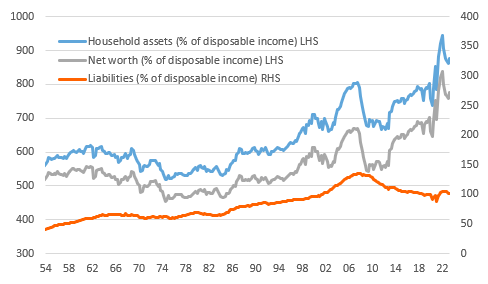

In aggregate, household assets are now equivalent to 876% of annual disposable income, while liabilities are ‘just’ 101% of disposable incomes. While this is down on the peak seen in the first quarter of 2022 and there are questions over wealth concentration, this is a much better position than any previous recessionary environment and means that the consumer sector, on the face of it, should be better able to withstand intensifying economic headwinds and support the narrative that the US economy will experience a soft landing without a painful recession.

Household assets and liabilities as % of disposable income

But stresses are emerging and will intensify

However, because we don’t have the granularity on who holds what, we have to be cautious in interpreting what is happening. There is clearly a strong chance that the bulk of this wealth is held by people who are already wealthy. Lower-income households are less likely to own their own homes, invest in the stock market or have a pension plan.

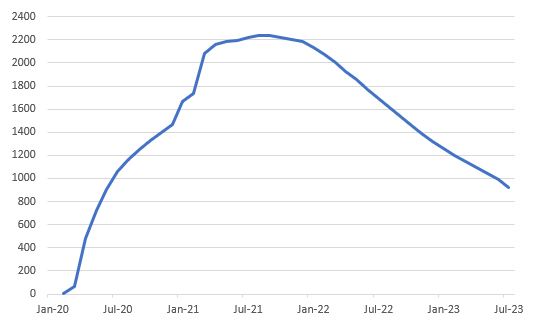

Using the personal income and spending report, we estimate that around $1.3tn of the $2.2tn of pandemic-era accumulated savings (caused by reduced spending and higher incomes via stimulus payments and uprated unemployment benefits) has been exhausted, and at the current run rate, all will be gone before the end of the second quarter of 2024. Note, this week’s Federal Reserve Beige Book warned of similar concerns, with some Fed Districts highlighting “reports suggesting consumers may have exhausted their savings and are relying more on borrowing to support spending”.

Pandemic era excess savings are being run down ($tn)

At the same time, banks are increasingly reluctant to lend to the consumer with the stock of outstanding bank lending flat lining since the banking stresses in March, having increased nearly $1.5tn from late 2021. We suspect that financial stresses have seen middle- and lower-income households accumulate the bulk of the additional consumer debt and have run down a greater proportion of their savings vis-à-vis higher income households, so a financial squeeze for the majority is likely to materialise well before the second quarter of 2024.

Consumer loan delinquencies are already on the rise, particularly for credit card and vehicle loans, with household finances set to become more stressed with the restart of student loan repayments. As a result, we fear that after a strong leisure and tourism-led summer spending splurge, darker skies are likely to emerge as we head towards winter.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Original Post

Read the full article here