Elevator Pitch

I still rate TPI Composites (NASDAQ:TPIC) stock as a Hold. A Buy rating isn’t warranted, as TPIC will need more time to witness a turnaround of its business operations. A Sell rating isn’t justified, as TPI Composites’ long-term growth outlook is intact.

Patience Is Required For TPI Composites

In my previous May 23, 2023 initiation article for the stock, I mentioned that “it will take some time for TPI Composites to achieve a better set of financial results” and I noted that TPIC is “more of a 2025 story.” My cautious view of TPI Composites is supported by recent developments, management disclosures, and consensus numbers.

Firstly, TPIC’s most recent quarterly financial performance was poor. The company’s latest third quarter top line of $373 million fell short of the Wall Street analysts’ consensus revenue estimate of $384 million by -3%. Normalized net loss for TPI Composites widened from -$0.39 in Q3 2022 to -$1.53 for Q3 2023, which was much worse than the market’s consensus bottom line forecast of -$0.59 per share. In its Q3 2023 results press release, TPIC highlighted that “the wind industry continues to face a challenging near-term macro environment” and this has affected the company’s results for the recent quarter.

Secondly, TPI Composites lowered the company’s full-year fiscal 2023 financial guidance. TPIC reduced its FY 2023 net sales guidance from $1,525-1,575 million previously to $1,500 million now. The company also revised its FY 2023 EBITDA loss margin outlook from -2.5% (mid-point of guidance) to -5%. At its Q3 2023 results briefing, TPIC revealed that its “customers are working through rationalization of their own inventory levels” which translates into “weakened near-term demand.”

Thirdly, the company acknowledged at its most recent third quarter results call that “we do not expect 2024 to be a year of growth” and it expressed its hopes of “an inflection probably in 2025.” TPIC cited factors like the rising rate environment and supply chain issues pushing back the timeline for the turnaround of the wind industry and the company.

Lastly, the current sell-side analysts’ consensus financial projections point to a meaningful improvement in financial performance for TPI Composites that only begins in FY 2025. The market sees TPIC’s revenue growth accelerating from a modest +3.0% in FY 2024 to +16.7% for FY 2025. Also, the company is expected to remain loss-making for FY 2024, before generating positive pre-tax earnings in FY 2025 as per S&P Capital IQ consensus data.

Based on what I have presented above, I continue to take the view that this isn’t the time to award a Buy rating to TPI Composites.

But TPIC Is A Good Long-Term Play Boasting Attractive Valuations

A Sell rating for TPIC will be too harsh, even though I am not ready to rate the stock as a Buy now.

TPI Composites emphasized at the company’s latest third quarter results call that it stays “bullish on the long-term energy transition” and thinks that TPIC will “play a vital role in the pace and ultimate success of the transition.” This really sums up the investment thesis for TPIC pretty well. Having a position in this stock is a way of placing a bet on the energy transition investment theme.

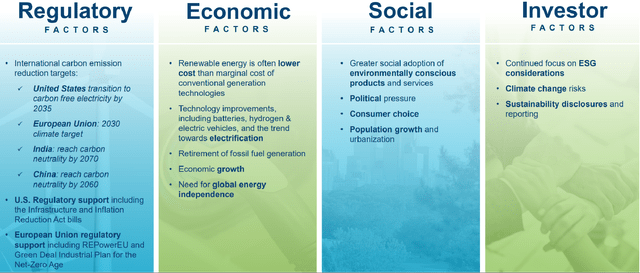

Key Drivers Of The Energy Transition

TPI Composites’ November 2023 Investor Presentation

As indicated in the chart above, there are multiple factors supporting the energy transition trend. TPIC has been a share gainer in the worldwide wind blade market over the past couple of years, which makes it an energy transition play.

In its November 2023 investor presentation slides, TPI Composites cited data from research firm Wood Mackenzie which shows that its “onshore global excl. China” market share in the wind blade industry increased from 15% in 2016 to 29% in 2019, prior to rising further to 33% last year. The proportion of wind blades production being outsourced grew from 50% for 2014 to 68% in 2021 as per Wood Mackenzie data highlighted in TPIC’s investor presentation. In other words, TPI Composites’ market share gains in recent years were supported by a growth in outsourcing.

On the other hand, TPIC’s current valuations and recent stock price performance seemed to have already factored in the unfavorable short-term prospects for the company.

In this year thus far, TPI Composites’ shares dropped by -76.2%, which represents a substantial underperformance as compared to the S&P 500’s +18.7% rise during the same time period. Also, TPIC’s last done share price of $2.33 as of November 21, 2023 implies that the stock is now -84.3% off its 52-week peak of $14.80. The market currently values TPI Composites at reasonably undemanding consensus forward FY 2024 and FY 2025 EV/EBITDA multiples of 3.1 times and 1.1 times (source: S&P Capital IQ), respectively.

Final Thoughts

TPI Composites, Inc. is a leading player in the worldwide wind blades market and it has been gaining share by leveraging on the outsourcing trend. While the stock is a play on the energy transition investment theme, this isn’t the time to be bullish on TPI Composites, Inc. stock in view of a disappointing outlook for the near term.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here