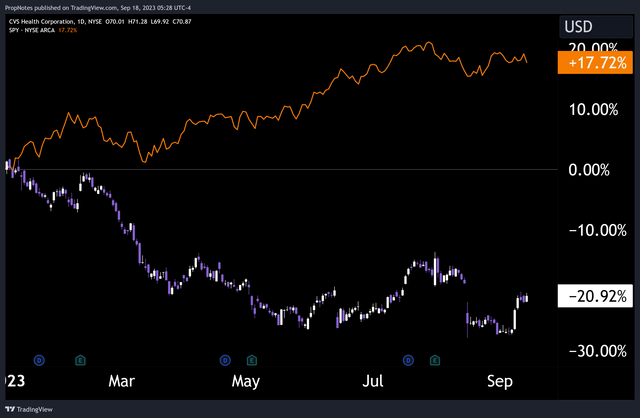

Over the last few months, shares in CVS Health (NYSE:CVS) haven’t been doing so well.

In fact, since the start of 2023, CVS’s stock has plunged more than 20%, even when taking dividends into account. This strongly contrasts with the S&P 500’s return of nearly 18% in that time:

TradingView

Despite this underperformance, we think that CVS deserves a second look.

Today, we’ll outline the top three reasons to take advantage of the recent dip and add this rock-solid company to your portfolio.

Let’s start with reason number 1.

1.) Strong Financial Performance

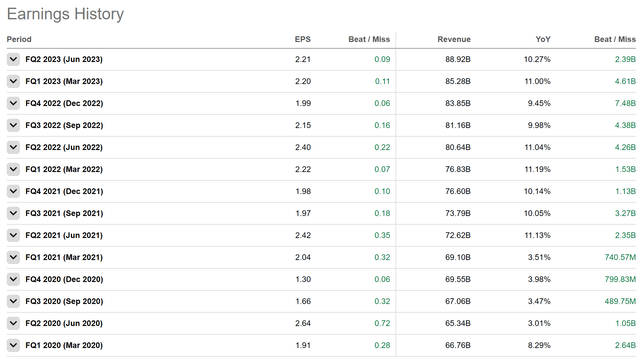

Given the aforementioned dip that CVS shares have undergone in 2023, it would be reasonable to assume that the company has been underperforming financially.

However, that’s not the case. In recent quarters, CVS has beaten both top and bottom-line expectations. Plus, they’ve been doing it for more than 5 years running:

Seeking Alpha

In their most recent quarter, CVS reported revenue of $89 billion, which was a beat of more than $2.3 billion. While small in percentage terms, nominally, the company has continued to grow its massive pie.

This $89 billion figure also represents 10% growth YoY, which shows that even at tremendous scale, CVS is finding ways to increase the scope and size of their business.

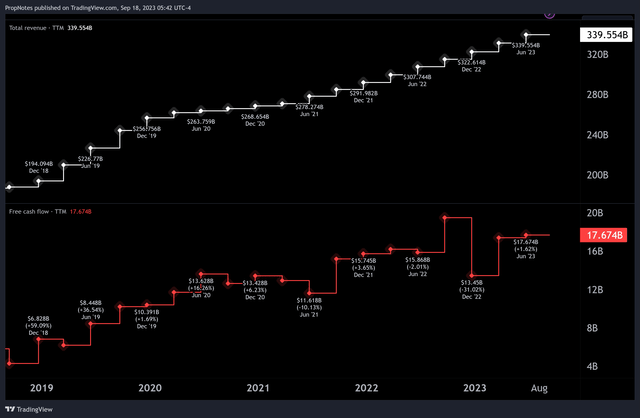

In addition, earnings and free cash flow have continued to grow alongside revenue, which shows that cash conversion is strong, and the company has exceptionally well-run operations:

TradingView

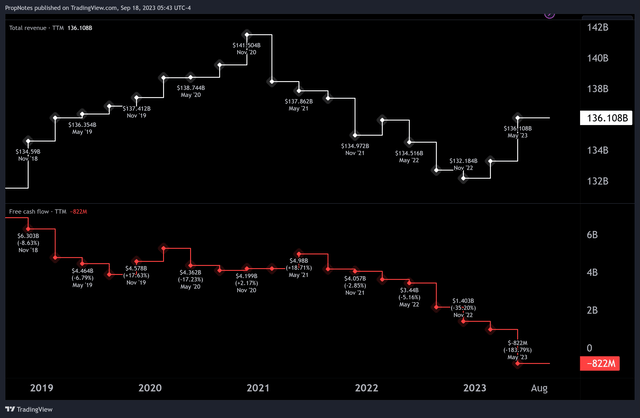

This contrasts with other major players in the space like Walgreens (WBA), which has seen flat revenue and tanking free cash flow:

TradingView

Rite Aid (RAD), another competitor in the pharmacy segment, is reportedly planning to file for bankruptcy.

Clearly, the competitive landscape is rough, which makes CVS’s strong track record stand out even more.

However, the question remains: How can CVS outcompete its competition so effectively?

The answer lies in our second reason.

2.) Massive Scale

A few years ago, CVS was a major pharmacy company, much like WBA or RAD. However, in late 2018, CVS merged with Aetna, a top 5 U.S. health insurance company, which created the first fully integrated healthcare company at scale in the United States.

This allowed CVS to drastically improve their product offering, and offer a better, more fully integrated experience to individuals and employers with healthcare needs.

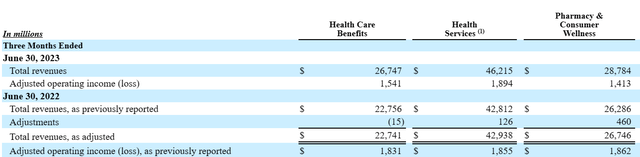

Right now, CVS operates through 3 different revenue-producing segments: Pharmacy Services, Health Services, and Health Care Benefits.

The Pharmacy Services segment includes the company’s retail pharmacies, mail order pharmacy, and specialty pharmacy.

Retail pharmacies are the most visible part of CVS Health, and they dispense prescription drugs and other healthcare products to consumers.

The mail order pharmacy provides prescription drugs to customers through the mail, and the specialty pharmacy dispenses high-cost and complex prescription drugs to patients with chronic or rare conditions.

The Health Services segment is the largest and most profitable segment in the company. Its products include CVS Health’s MinuteClinic walk-in clinics, HealthHUBs, and telehealth services. MinuteClinics offer a variety of basic healthcare services, like immunizations, physical exams, and treatment for minor illnesses.

HealthHUBs are larger clinics that offer a wider range of services, including primary care, dental care, and behavioral health care. Telehealth services allow patients to see a doctor online from the comfort of their own home.

Finally, the Health Care Benefits segment offers health insurance plans to individuals and employers. CVS Health also offers pharmacy benefit management (PBM) services, which help employers manage their prescription drug costs.

These varied segments are important because the scale that CVS has across different dimensions of human health leads to incredible cross selling opportunities:

10-Q

This cross-segment strength also leads to strong diversification of revenue and profit, which is incredibly important in times of economic instability.

Given that our gloomy economic outlook hasn’t changed much from our assessment a few months ago, the ability to weather all economic backdrops is a valuable trait to have for potential portfolio constituents.

But why is now the right time to get involved?

Let’s take a look at reason number 3.

3.) An Attractive Valuation

While CVS has a solid financial track record and an unmatched product offering, why is now the time to get involved?

In short, we think the valuation at the moment represents one of the best deals on the market today, and that combined with the solid 3.4% dividend yield, an entry point around these prices should lead to very strong total return potential over the medium & long term.

Let’s have a look at that valuation.

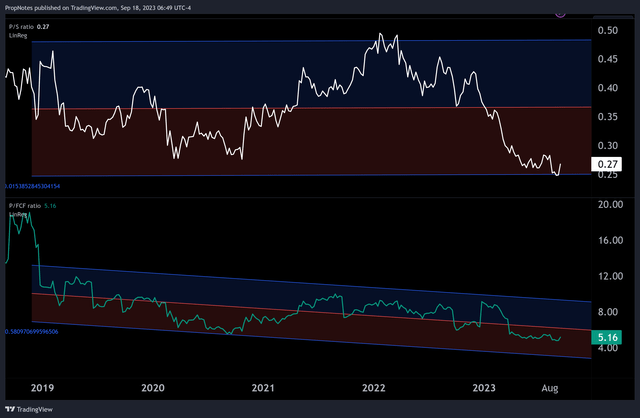

Right now, CVS is trading at only 0.27x sales and 5.16x free cash flow.

Looking historically, a sales multiple at this level represents the best deal that could be had for CVS revenue over the last 5 years, and the same goes for FCF:

TradingView

Not only are these multiples at 5-year lows, but they are also deeply discounted when measured vs. the linear regression & deviation of historical values.

When values get to this point, it can prove to be a very advantageous time to buy.

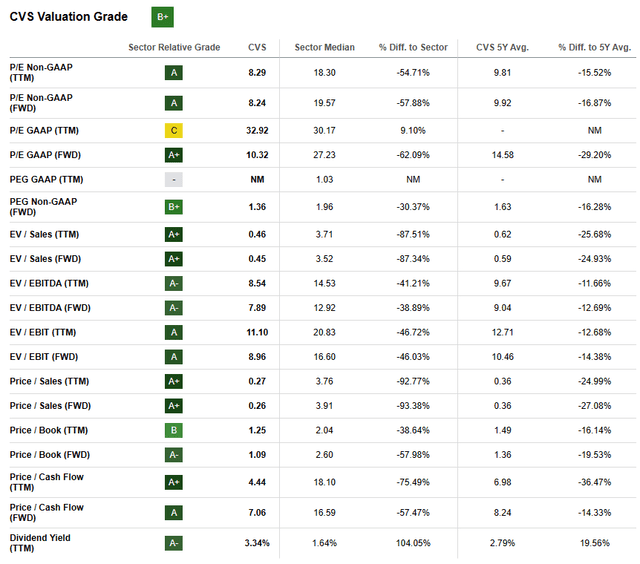

Additionally, Seeking Alpha’s Quant Rating System gives CVS a value score of “B+”, which we broadly agree with.

Seeking Alpha

All in all, CVS appears to be trading at an advantageous valuation as a result of a momentary slowdown in profit growth. That said, we’re not concerned about the company’s business portfolio, and expect that things will continue to normalize following the COVID traffic boom.

Now seems like a good opportunity to get in front of that expectation.

Summary

In conclusion, CVS’s strong financial performance is evident in its revenue, earnings, and free cash flow growth & stability. The company has attained massive scale, which gives it a competitive advantage and allows it to cross-sell its products and services. Finally, CVS’s valuation is quite attractive, with its sales and free cash flow multiples at 5-year lows.

Net net, CVS Health is a rock-solid company, and the recent stock underperformance should serve as a great opportunity to pick up some discounted shares for your portfolio.

Cheers!

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here