Research shows that the vast majority of individual investors – and even the majority of active professional money managers – do not even achieve the total returns of the S&P500 let alone “beat the market”. There are, of course, many reasons why this is the case. But the most important thing for the majority of individuals to do is to simply acknowledge that reality and research the subject. I suggest the Bogleheads website as a great starting point. Today, I will explain my strategy to not only attain the returns of the S&P500, but to beat the market. However, in my opinion, the first step to take is to insure that you are at least achieving the average long-term returns of the S&P500.

Investment Strategy

Many years ago, I put all my investments into a spreadsheet and began tracking it on a quarterly basis. After I retired, I started tracking it monthly. Although I thought myself to be an above average investor, I quickly discovered that my long-term average annual returns were actually below those of the S&P500. Again, there were a number or reasons why, but the important point was to acknowledge that fact and to make a course correction. As a result, my strategy was to begin constructing a well-diversified portfolio built for the long-term with the S&P500 as the core foundation of that portfolio. I did so over a period of several years, and have been rewarded with not only a simpler portfolio, but one that has generated better average annual total returns.

One Size Does Not Fit All

Now, before I go any further, and in hopes to minimize the number of comments that will point it out, when it comes to portfolio construction and strategy it is important for investors to understand that one size does not fit all. There are a plethora of factors that should impact any individual investors’ portfolio decision making: age, net-worth, working/retired, goals, risk tolerance, taxes … well, you get the picture. Please keep this in mind when I discuss the sample portfolio structure below.

A Sample Portfolio

I prefer taking a top-down approach when it comes to capital allocation. That is, I look at my total (liquid) net-worth and allocate capital into the various investment categories for which I want exposure. A sample portfolio implementing such a strategy is shown below:

| Investment Category | Allocation |

| S&P500 | 50% |

| Dividend Income | 10% |

| Growth | 10% |

| Sector Specific | 5% |

| Speculative Growth | 3% |

| Precious Metals | 2% |

| “Cash” | 20% |

| 100% |

This sample portfolio has allocated 50% toward the S&P500. In my case, this is accomplished primarily with investments in the Vanguard S&P500 ETF (VOO) and the Fidelity 500 Index Fund (FXAIX). These are long-term holdings in which I never sell but will typically and readily add to during times of big market corrections (as in last year’s bear market).

The dividend income category, for myself, is primarily energy stocks: ConocoPhillips (COP), Phillips66 (PSX), Chevron (CVX), Exxon Mobil (XOM), and Enbridge (ENB). These stocks have delivered excellent dividend growth over the decades that I have owned them. That said, many retired investors have been advised (brainwashed?) into vastly over-emphasizing the dividend income category simply because they are “retired” and despite the fact that many can live just fine on the combination of their pensions, social security, and investments. I discuss this issue in one of my most popular Seeking Alpha articles: Retirees Beware: Dividend Investing Is Overrated. From what I gather from writing articles on Seeking Alpha, and reading thousands of comments, this is probably the #1 reason why retired investors significantly lag the returns that the market is more than willing to give them via the S&P500.

Being an engineer, the growth category of my portfolio is primarily directed at the Technology Sector and is my attempt to outperform the market (i.e. the S&P500). These stocks include the Invesco Nasdaq-100 Trust (QQQ), Amazon (AMZN), Google (GOOG), Broadcom (AVGO), and Jabil (JBL) – most of which have beaten the S&P500 over the time frames in which I have owned them.

I question whether or not the sector specific category is worth the time and effort and if I would simply be better off simply moving the proceeds into the S&P500. Some of these are legacy positions prior to my change in portfolio strategy and include ETFs in the Defense & Aerospace sector (ITA)(XAR), Consumer Staples (XLP), Utilities (XLU), Healthcare (FHLC) and – of course – the Technology Sector: the Fidelity MSCI Information Technology ETF (FTEC), the Van Eck Semiconductor ETF (SMH), and the iShares Expanded Tech/Software ETF (IGV) – among a few others. Other than the technology funds, these funds give me some diversification but have generally lagged in comparison to the S&P500.

The speculative growth category includes higher risk/reward opportunities and typically contains stocks that I watch with an eagle-eye. For instance, one of my speculative investments was in the Grayscale Bitcoin Trust (OTC:GBTC), which I invested in after I noticed that PayPal and Square announced they were supporting the crypto (see: Bitcoin Penetrates Further Into the Mainstream). This turned out to be one of the fastest appreciating investment I have ever made – tripling in a matter of weeks. I eventually sold half to cover my original cost basis, and later sold the other half on the way down. To be fair, I have also had my fair share of failures – most recently in Akoustis (AKTS), a company with great technology but a terrible stock. Regardless, the goal of the speculative growth category is for the successes to far outweigh the failures such that the long-term performance of the category beats the S&P500. More conservative investors may choose to eliminate this category from their portfolios.

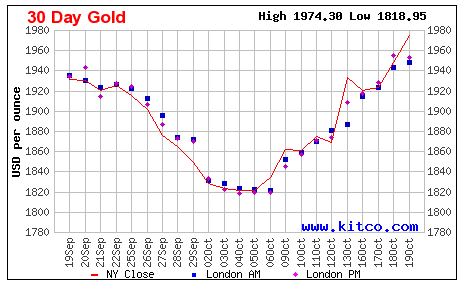

I got into precious metals way back in the George W. Bush administration when I predicted he would get us into a war and spend a lot of money. I bought gold and silver U.S. minted coins. Both have roughly doubled since then, but have probably lagged the returns had I simply bought the S&P500 instead. However, I view gold and silver as insurance policies for black-swan events and geopolitical uncertainty – which is exactly what the world faces today: the 2020 January 6th coup-attempt in the U.S., a republican party that arguably no longer even supports American Democracy and has proven to be incapable of governing the House of Representatives (no Speaker of the House now for 17-days and counting …), Putin’s horrific war-on-Ukraine, the potential for a large-scale in the Middle East, and China’s militaristic aggression on Taiwan. It is no surprise that gold has been rallying over the past couple of weeks:

Kitco

In my opinion, and despite the lack of investor analysis on the subject, the “cash” category – and the management of it – is one of the most important categories within an investor’s portfolio. “Cash”, at least for me, is defined as: checking/savings accounts for day-to-day transactions, money market funds, CDs, and bonds. Each of these can be a source of income, comfort, and long-term gains.

For instance, in the early 2000’s when I was still working, I bought some U.S. I-bonds with excess cash that I was uncomfortable putting into “the market”. As you know, I-bonds have two components: a “fixed” rate and a “variable” rate. The variable rate is based on the rate of U.S. inflation. At the time (pre-shale), I was worried about a potential shortage of oil leading to high inflation. For years these I-bonds were pretty awful investments and I almost sold them. But I am glad I didn’t as over the past couple of years some of them yielded 10-11%. And, as Einstein once said:

Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.

I also maintain a CD ladder and have various money market funds that are currently yielding 5%+. However, in my opinion the most important aspect of the cash category is to enable you to take strategic advantage of market volatility by pouncing on attractive investment opportunities when they arise. Last year, investors were given a bear-market gift with tremendous investment opportunities – but only if you had available cash to put to work.

Take Action (But Not All At Once)

As I mentioned earlier, I track my portfolio spreadsheet on a monthly basis. But that doesn’t mean I take action every month. Now that I have my portfolio structured the way I want it (well-diversified and built for the long-term …), I can go months hardly doing anything at all. And to repeat, it took me years to transition my under-performing portfolio into the portfolio I decided I wanted – and I advise investors not to rush that process. Take your time and move intentionally and wisely.

I say that because research also shows that individual investors (and professional money managers …) are just awful at timing the market. Much of that is because of the influence of incessant investment “noise” by loud-mouthed “experts”. The other reason is because timing the market means you have to be right twice: when to get out, and when to get back in. I have several friends that sold during the 2008/2009 financial crisis and to this day have never gotten back into the market. As a result, they missed the biggest bull-market of their lives.

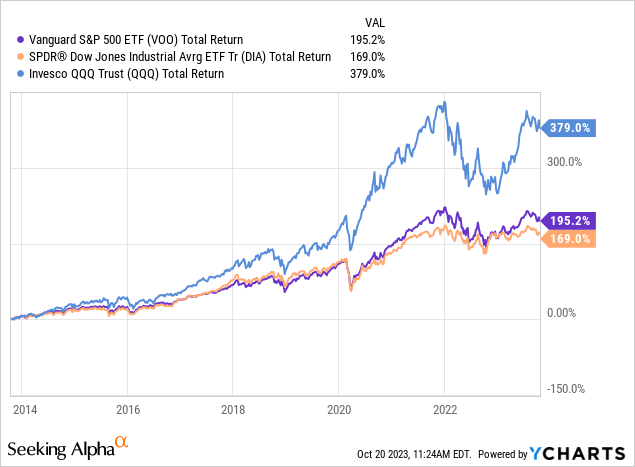

At the end of the day, a picture is worth a thousand words, and the 10-year total returns chart of the major market indexes (as represented by VOO, (DIA), and QQQ) speaks volumes:

Heck, when I first started investing in the market during the early 80’s, the DJIA was around 1,200. At pixel time the DJIA is at 33,266 (+27.7x). The S&P500 was trading around 460. At pixel time the S&P500 is at 4245 (+9.2x). And those returns don’t even include dividends.

Rebalancing

The importance of periodically rebalancing your portfolio cannot be overstated. I recommend reaffirming your allocation percentages and your portfolio at least once a year – I do it at least twice a year and even monthly during times of high volatility. Rebalancing makes sure you stay on your long-term plan and prevents you from become over-loaded into any particular asset class (unless that is what you planned to do, like me with the S&P500).

Summary & Conclusions

As we head toward the end of another eventful and fascinating year of world events and investing, I encourage investors to analyze their portfolios to make sure it matches their goals, objectives, and risk tolerance. I also encourage them to be ready to take advantage of market volatility because, given the world we live in today, you are quite likely to get a great chance to make some wise portfolio moves at valuation levels significantly below those available today. Thanks for reading and I wish you (long-term) success!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here