There is no situation like the open road, and seeing things completely afresh. ― James Salter.

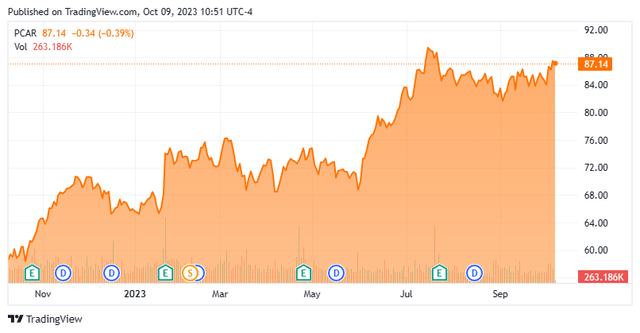

Today, we put Paccar Inc (NASDAQ:PCAR) in the spotlight for the first time. This stock has moved up by over 50% over the past year and still seems cheap on a P/E basis. However, the company’s business can be cyclical, which could make it vulnerable if the country slips into recession in 2024. In addition, the shares have seen some heavy insider selling of late. Still upside ahead, or is it time to take some profits? An analysis follows below.

Seeking Alpha

Company Overview:

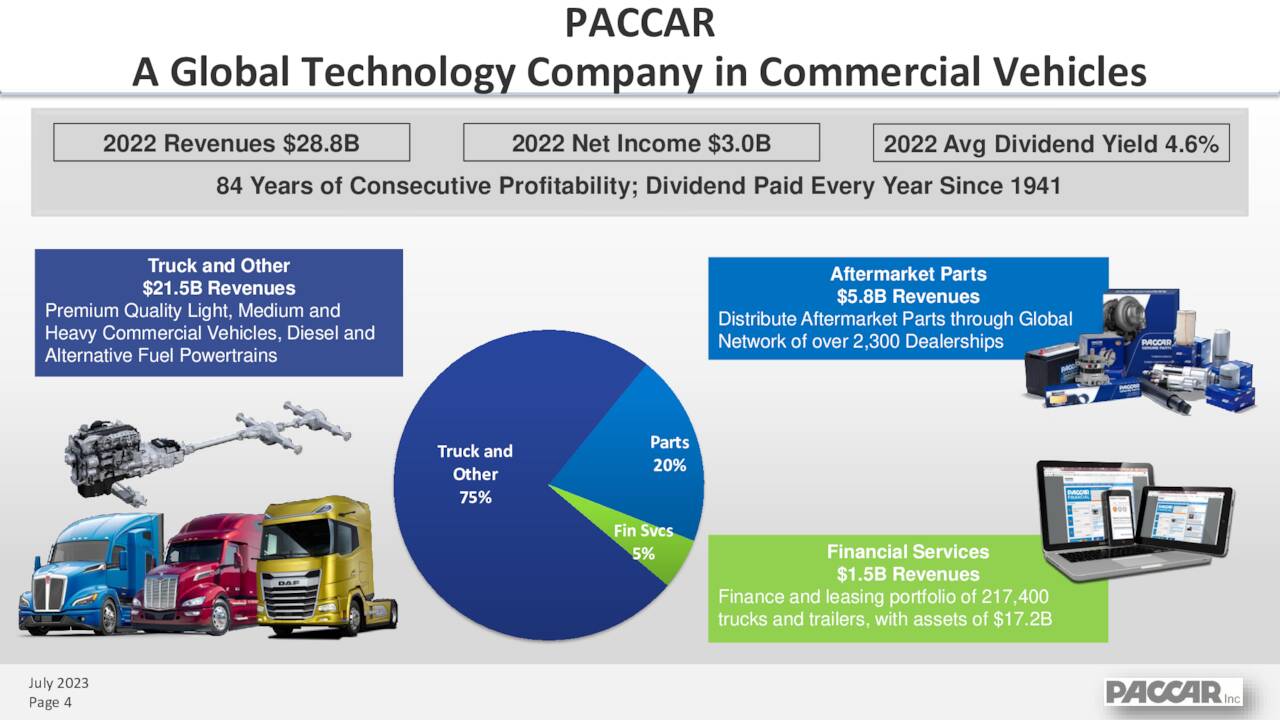

Paccar, Inc. is headquartered just outside of Seattle in Bellevue, WA. Paccar designs, manufactures, and distributes light, medium, and heavy-duty commercial trucks both here in the United States and globally. The company builds these products as well as provides parts and financing. Truck sales do account for approximately three quarters of the company’s overall sales and sell under well-known names like Peterbilt and Kenworth. The stock currently sells around $87.00 a share and sports an approximate market capitalization of just north of $45 billion.

August Company Presentation

The company is embracing alt-energy to a large degree throughout the company. During the second quarter, Paccar announced the expansion of a strategic partnership with Toyota to develop and bring to market zero emissions hydrogen fuel cell-powered Peterbilt and Kenworth trucks.

In September, Paccar announced it had joined Cummins Inc. (CMI), Daimler Trucks & Buses US Holding in forming a joint venture to manufacture battery cells for electric commercial vehicles and industrial applications in the U.S. The group plans to build a 21-gigawatt hour factory at a projected cost of $2 billion to $3 billion.

Second Quarter Results:

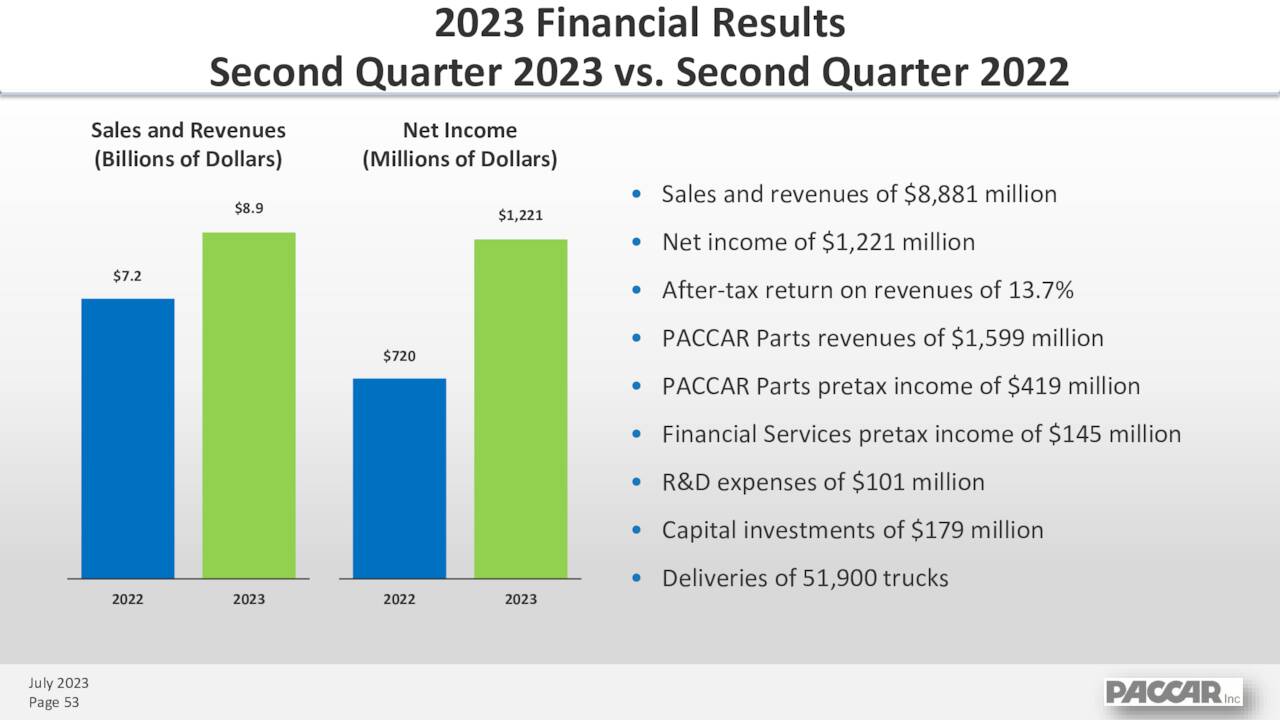

The company posted second quarter numbers on July 25th. Paccar delivered GAAP earnings per share of $2.33, 16 cents a share above estimates. Net income rose 70% from the same period a year ago to $1.22 billion. Revenues grew 24% on a year-over-year basis to $8.88 billion, some $650 million above the consensus.

August Company Presentation

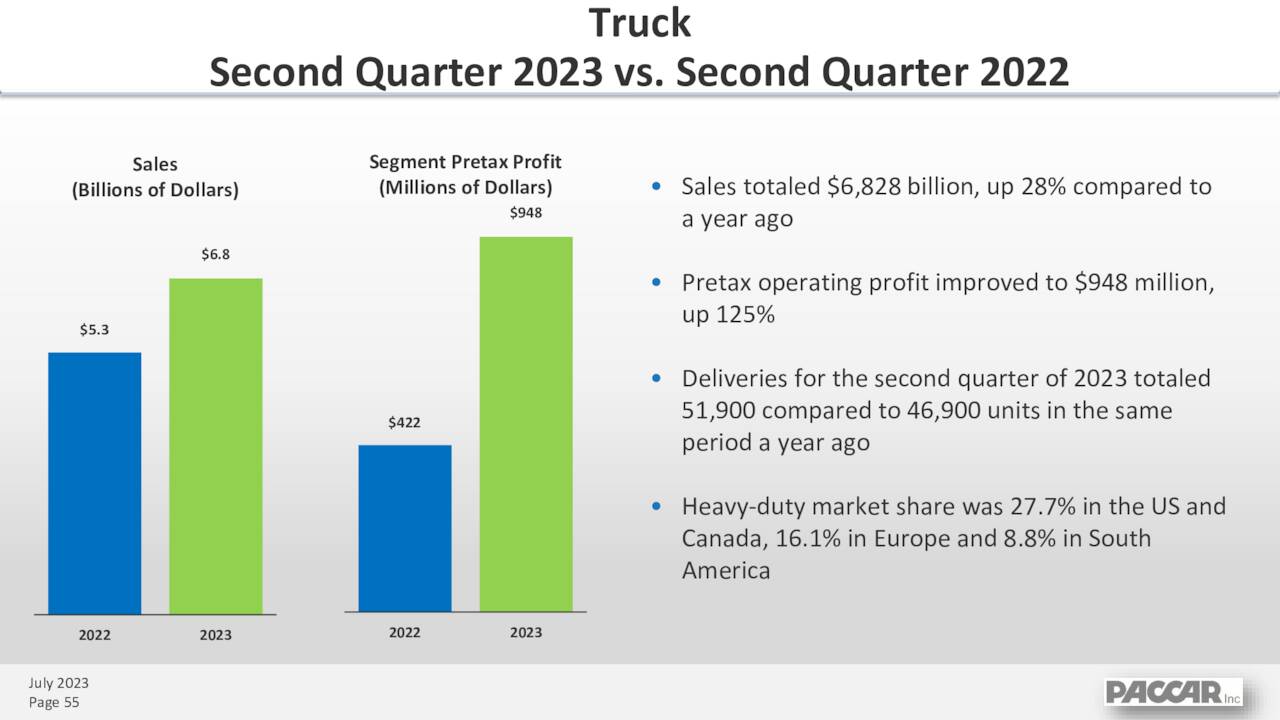

The company delivered nearly 52,000 commercial trucks during the quarter. Management estimated it will deliver 48,000 to 52,000 trucks in the third quarter, a traditionally slow part of the fiscal year. The truck division made $948 million of pre-tax income of $6.8 billion. A significant improvement in the $5.3 billion in sales and $422 million of pre-tax income it made in 2Q2022.

August Company Presentation

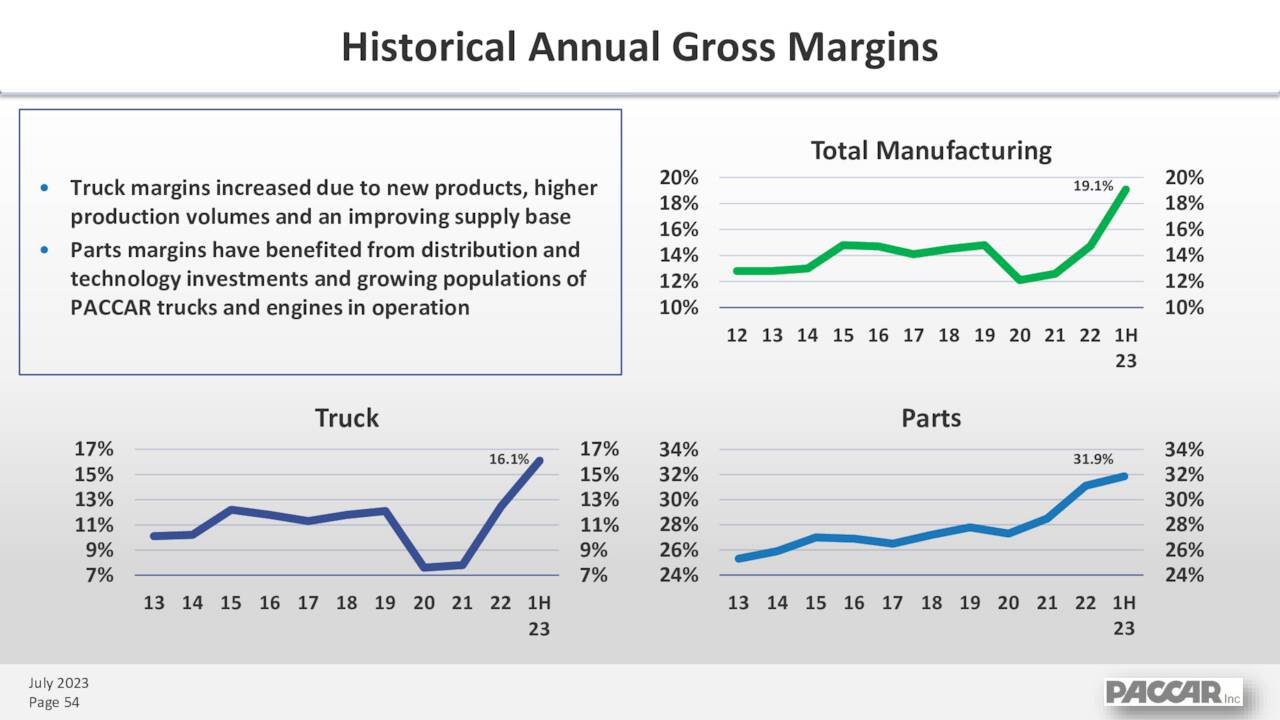

Paccar’s parts division grew pretax income by 19% on a year-over-year basis to $419.3 million on $1.6 billion worth of net sales (an 11% increase over 2Q2022). Parts historically have much higher gross margins than sales of trucks, it should be noted.

August Company Presentation

PACCAR Financial Services produced pretax income of $144.7 million, roughly flat to the same period a year. Revenues did increase to $439.8 million from $372.5 million.

Analyst Commentary & Balance Sheet:

Over the past three months, Raymond James ($105 price target), JPMorgan ($97 price target) and Jefferies ($115 price target) have reissued Buy ratings on the stock. In contrast, a half dozen analyst firms including Goldman Sachs and Credit Suisse have reiterated Hold, Sell, or Neutral ratings on the stock. Price targets proffered range from $78 to $90 a share.

Less than two percent of the outstanding float of these shares is currently held short. Two insiders sold just under $11 million worth of shares in September of this year. Multiple insiders also sold nearly $20 million worth of shares collectively in 2023 to that point as well. There have been no insider purchases in this stock since 2018.

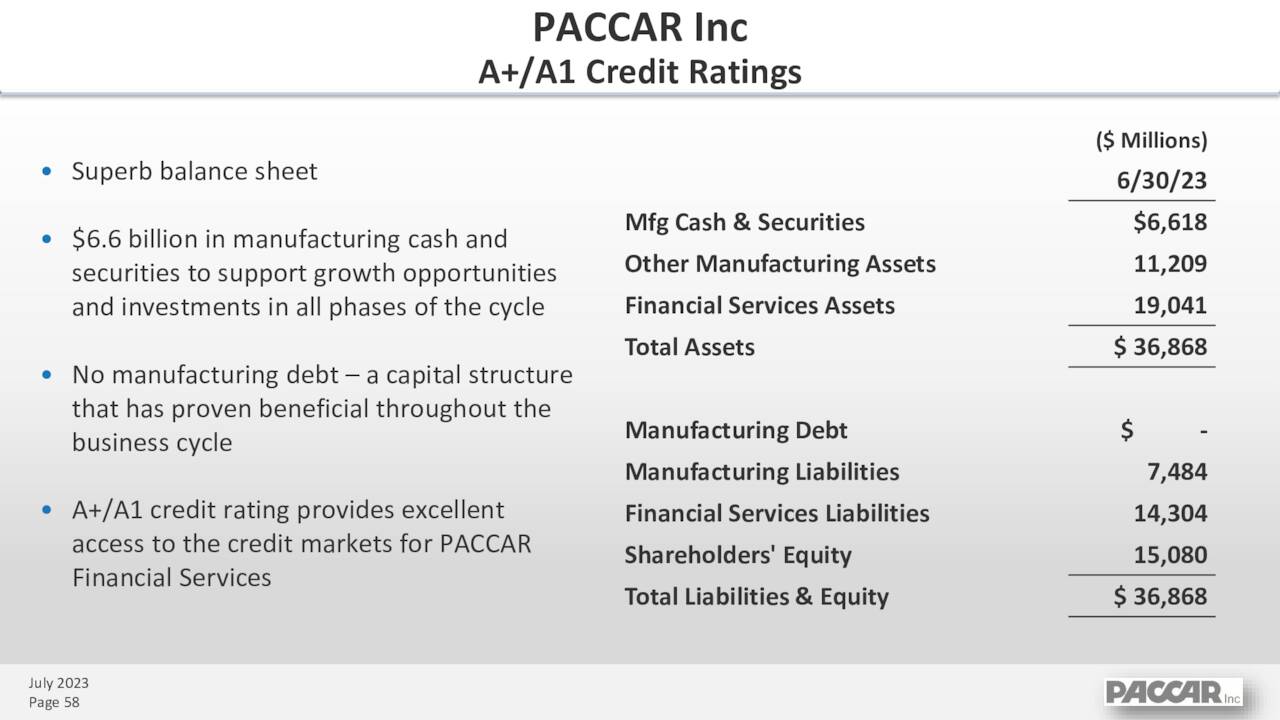

The company ended the second quarter with just over $6.6 billion worth of cash and marketable securities on its balance sheet after delivering an operating cash flow of $975 million in the quarter.

August Company Presentation

Verdict:

Sales came in at $27.3 billion for FY2022, and Paccar booked a profit of $5.75 a share. The analyst firms’ consensus has revenues growing 20% in FY2023 and profits soaring to $8.51 a share. The analyst community projects that earnings will fall to seven bucks a share in FY2024 as revenues fall in the high single digits.

The shares don’t seem expensive compared to the overall market multiple in the high teens. PCAR goes for just over 10 times forward earnings and pays a just over 1.2% dividend yield after boosting its dividend payout by eight percent this July.

However, this has been a historically quite cyclical industry that suffers large decreases in orders for new commercial trucks when the country enters a recession. Demand tends to ease as the movement of goods decreases during economic contractions. The recent large rise in interest rates certainly doesn’t make a commercial truck easier to finance, either.

Given this, I think analyst firms have it right here and PCAR is simply not a Buy at current trading levels. Something also reflected by the significant amount of insider selling in the shares in recent months as well.

There is more credit and satisfaction in being a first-rate truck driver than a tenth-rate executive. ― B. C. Forbes.

Read the full article here