Investment Rundown

The share price for Textainer Group Holdings Limited (NYSE:TGH) has been on a roll for the last 12 months as it has risen by nearly 40%. Yet, the company is still trading at what I think is a pretty fair valuation to be buying at. A p/e under 8 and a dividend yield of over 3% I find quite appealing, especially seeing as the earnings multiple is over 50% below the sector. Now, I think there is a good reason for the discount, seeing as the company works with containers which have been under pressure as spending from consumers has taken a turn downwards given the rise in interest rates and the more limited amount of capital available. I think the worst has passed and TGH is now in a good spot to start a position. The market has been bullish for the last 12 months, and I don’t think we have missed the train buying right now.

Company Segments

TGH is engaged in the global intermodal container industry. This multifaceted business is organized into three key divisions, each playing a pivotal role in the company’s operations. TGH specializes in the ownership of intermodal containers, which encompass a wide range of containers, including general-purpose, specialized dry freight, refrigerated, tank, 45-foot, pallet-wide, and other specialty containers. This extensive container inventory forms the backbone of its business.

Investor Presentation

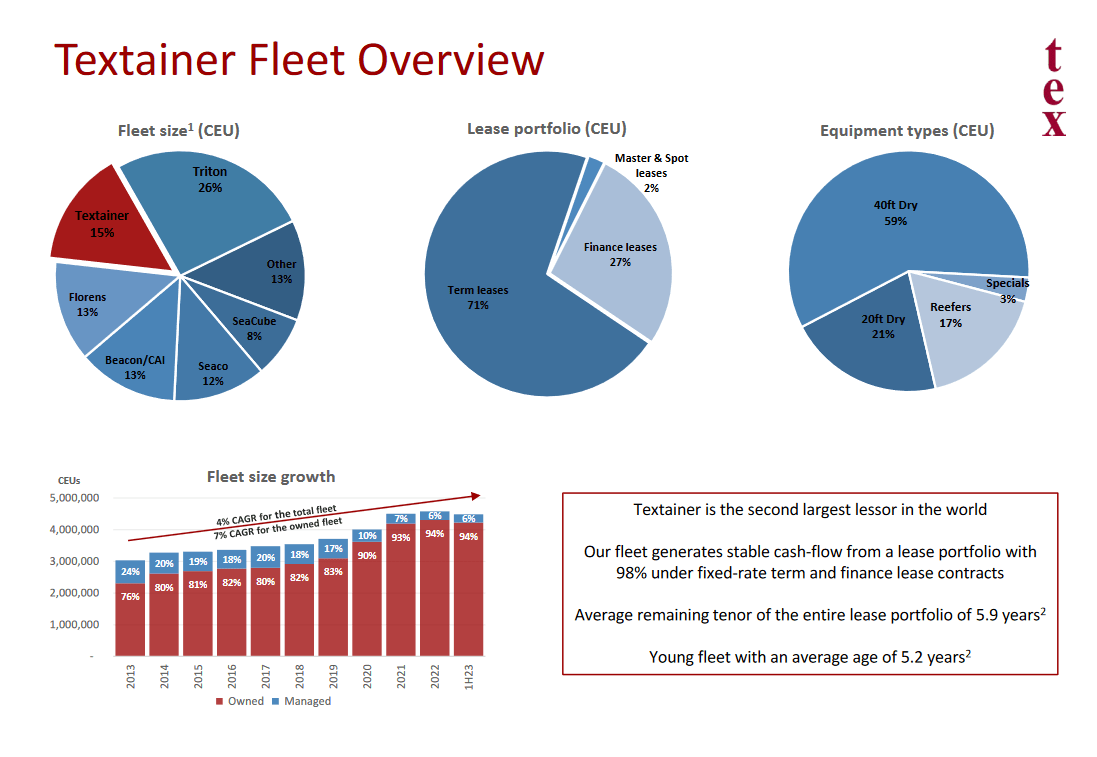

The company manages these containers, providing comprehensive services that include container management, acquisition, and disposal for both affiliated and non-affiliated container investors. TGH is involved in the resale of shipping containers, not only from its fleet but also through the acquisition, leasing, and resale of containers from various sources, including shipping companies and container brokers. With a substantial fleet comprising approximately 2.7 million containers, equivalent to 4.4 million twenty-foot containers, TGH is a major player in the industry. Its diverse customer base includes shipping corporations, freight brokers, and even the United States government. The company has seen shifting demand and the last quarter showed the bottom line take a pretty big leap downwards as interest expenses grew and last year’s quarter had a $16 million higher gain in gain on sales of fleet containers.

Markets They Are In

alphaliner

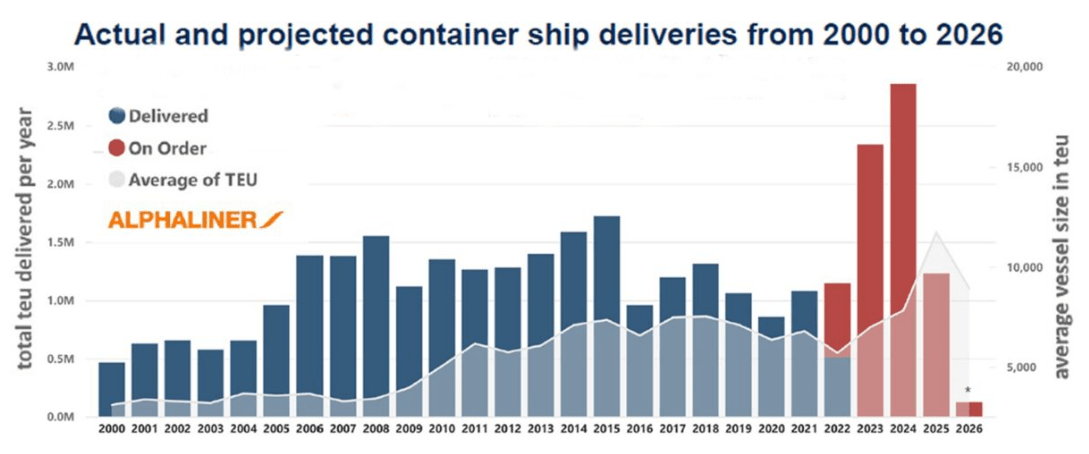

The intermodal logistics sector has experienced its peak shipping season from June through December. Although June might seem like an early start, it marks a crucial period for many shippers striving to expedite the transportation of their goods through West Coast ports before the end of June. Rail transport often plays a pivotal role in the movement of imports arriving at West Coast ports, contributing to the increased activity during this timeframe. This peak season presents a significant opportunity and challenge for the intermodal industry, requiring effective planning and management to meet the heightened demand efficiently.

I think that going into both the third and fourth quarters for the company I think that TGH will post an uptick in their revenues and this could ignite another share price run upwards should they manage to surprise the market and estimates.

Risks

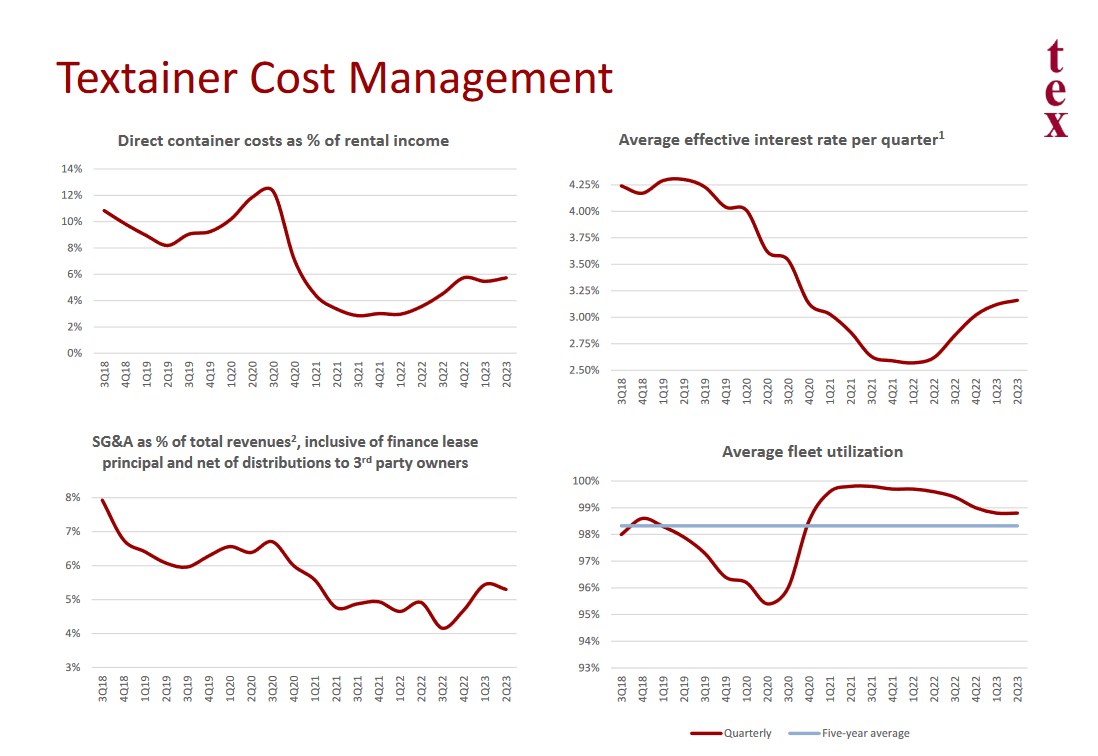

TGH maintains ownership of a substantial fleet of containers, which are primarily deployed through leasing arrangements. While these containers are valuable assets, it’s important to acknowledge that their value can diminish over time due to various factors such as wear and tear, accidents, or becoming outdated in a rapidly evolving industry. The ongoing maintenance and repair costs associated with these containers can also influence the company’s overall profitability. It’s imperative for TGH to effectively manage and address these challenges to ensure the continued success of its container leasing business. In the last quarter, the utilization rate was at 98.8% which is a slight decline from the 99.6% it had a year prior. This seems to indicate a slight decline in demand, but something that should reverse in 2024 and beyond I think. With this lower utilization rate, the depreciation has declined YoY as well for the company. I think a positive trend has been that it has been quite stable for TGH as Q2 FY2023 was $70 million last quarter.

Investor Presentation

TGH conducts its operations on a global scale, generating revenues in various currencies. The inherent exposure to multiple currency markets means that the company is susceptible to fluctuations in exchange rates. These fluctuations can have a significant impact on various aspects of TGH’s financial performance, including revenues and costs, ultimately affecting its overall profitability. Sudden currency devaluations or abrupt shifts in exchange rates can potentially result in financial losses, making it essential for the company to actively manage and mitigate these currency-related risks. It doesn’t seem to have impacted the cash flows that harshly though for the last quarter. Given the stronger dollar though, I would have expected that perhaps TGH could have made use of this to invest and expand their fleet by purchasing from countries with depreciating currencies to the US dollar. I can see the lack of investment in new fleets as something that can spook the market. If TGH doesn’t see it as valuable to expand the fleet it could indicate that market conditions may worsen and lead to lower earnings. For the moment, I don’t think this is an immense risk, seeing as TGH still invested around $32 million in purchases, down from $254 million the year prior.

Valuation

The share price for the company has risen quite quickly over the last few months but I still see them going higher. The valuation is just at an FWD p/e of 7 and with the broader sector trading at a multiple of 17 it leaves a lot of potential still. TGH has been performing quite well over the last few quarters with decent top and bottom-line growth, which should be rewarded with a higher multiple. The market has realized this and is partially the reason for the quick climb in the last 12 months. I see the stock as a solid buy as long as it’s under a p/e of 12 – 13, which leaves a solid margin of safety seeing as TGH is far below that multiple currently.

Final Words

TGH has had a nice run in the last 12 months as the share price is up nearly 40%. I think that given the discount the company is still trading at to the sector, it constitutes a buy. Pair that with a solid dividend yield and we have a pretty solid long-term investment.

p/e (Seeking Alpha)

With an over 50% discount based on earnings to the industrial sector, I think TGH displays a limited amount of downside still. I find a fair value for TGH to be closer to the sector. The last quarter showed some short-term pain but isn’t indicative of the long-term potential of the company. I don’t think we will see a 100% increase in the near term, which is what it would take to move towards a valuation more in line with the sector. Such an increase I think will instead come over the medium term as TGH continues to expand its fleet and deliver a higher net income consistently. Given the upside potential I am concluding that TGH stock constitutes a buy.

Read the full article here