Why TECK Should Be On Your Watchlist

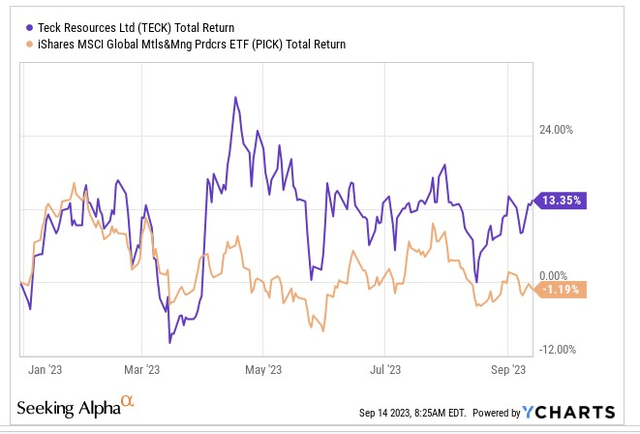

Teck Resources Limited (NYSE:TECK), headquartered in Vancouver, BC, is a global metals and mining player, with particular expertise in the terrains of copper (~20% of group revenue), zinc (~20% of group revenue), and steelmaking coal (~60% of group revenue). Within these portfolios, TECK dabbles in exploration, development, mining, and processing. This year, when global metal and mining stocks have largely not made any headway, TECK has held up reasonably well, delivering double-digit returns.

YCharts

Note that TECK has managed to deliver positive returns this year, despite facing some production challenges, and consequently trimming its FY copper guidance production by -15% at the end of Q2 (now expected to come in at 330k-375k tonnes by the end of this year).

Much of the interest around TECK has been centered around its intention to split its business and create value for shareholders by selling a part or the full portion of its steelmaking coal business (Elk Valley Resources). Elk Valley will no doubt have plenty of suitors as it is a tried and trusted business, with a strong reserve base, and a track record of generating reliable free cash flows, across various commodity cycles. Note that it is also considered to be amongst the world’s top-3 exporters of steelmaking coal and, the situation is even more favorable, as we are now in an era where the alacrity to pursue new projects is certainly on the wane.

While Glencore has been bandied around as the most convenient buyer for the sale of the entire coal business (as it will not require a complicated shareholder vote), it looks like this portfolio could generate more value for buyers from South Asia. For instance, in India, the government there intends to press the pedal and boost the country’s steel production capacity by 86% over the next seven years. That is all very well, but the local metallurgical coal in India is sub-par as it is deficient in vitrinite, and has high ash properties. For entities who are part of the domestic steel cycle in India, it would make greater sense to buy high-quality international coal portfolios such as TECK’s where the vitrinite and ash content is more well-balanced. Regarding this theme, whilst there has not been any official confirmation, India’s biggest steel producer – JSW Steel has now emerged as the favorite to take a stake in Elk Valley, with reports valuing the entire business at $8bn.

If this comes to fruition, then TECK’s prospects will predominantly be driven by conditions in the copper market, where long-term demand conditions are expected to surge on account of the burgeoning electrification wave across the globe. Recent studies have shown that copper demand through 2030, could potentially exceed supply by 5-9m MT.

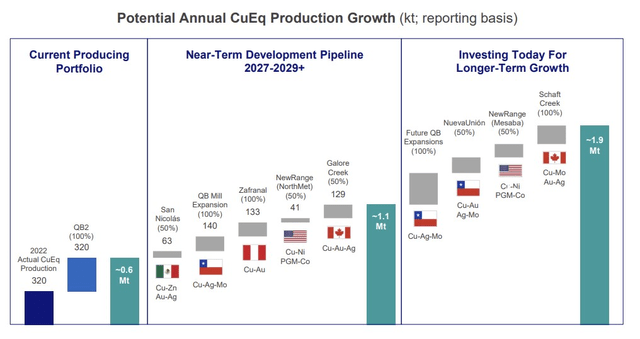

TECK recognizes the opportunity and is putting the building blocks in place to flourish over the next decade. Admittedly, the company’s copper production from its flagship QB2 copper mine in Chile has recently been hampered by certain construction and commissioning roadblocks (Q2 production was down by 10%), but this is an ephemeral development, and by the end of the year, QB2 is still likely to hit full production. QB2 at full tilt would immediately put TECK in the midst of the top 20 producers in the world; it also has a slew of other development projects in established mining territories in North and South America (see image below) which could see it have a production capacity of 1.1MT towards the latter half of this decade.

Q2 Presentation

EBITDA Outlook and Valuation

Whilst one can appreciate the medium to long-term tailwinds that could potentially lift TECK’s status over time, we are not sufficiently convinced that this is the best time to pursue the stock.

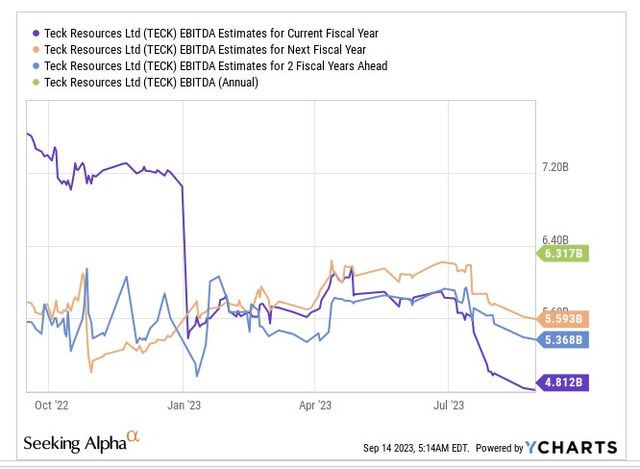

Note that even though production levels in H2-23 for both TECK’s copper and zinc operations will likely be better than what was seen in H1-23, that still won’t be sufficient to prevent what is likely to be a drastic contraction in the FY23 group EBITDA by 24% YoY. Granted, a lot of this is linked to factors beyond the company’s control, such as pricing effects (in Q2, pricing alone had a -47% YoY impact on group EBITDA), and IFRS-related accounting changes at the gross profit level, which would showcase a relatively higher threshold of unit operating costs for QB2’s production pickup.

YCharts

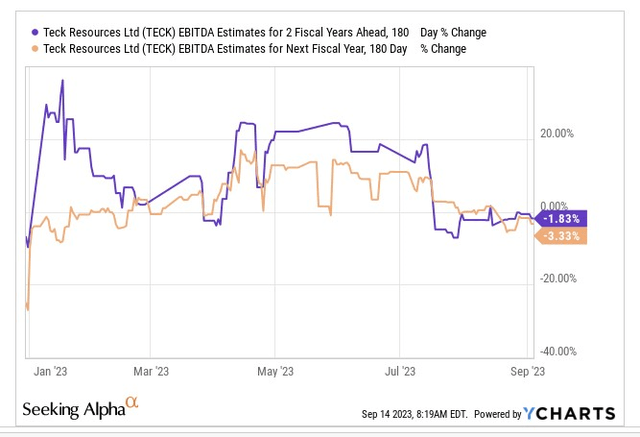

Given the low base effect from FY23, it is reasonable to expect some EBITDA growth in FY24 and FY25, but note that even by FY25, Teck’s group EBITDA threshold will still be around 12% short of what was seen in FY22. If TECK exits the coal business completely, as mooted recently in the press, the variance shortfall with the FY22 EBITDA number may only likely widen. One can infer that consensus is yet to make any major adjustments to the business without the coal portfolio, as over the last six months, their EBITDA numbers for FY24, and FY25 have barely moved.

YCharts

So, the question one ought to ask is, are you prepared to pay a higher multiple for what is likely to be a smaller business over the next few years?

YCharts

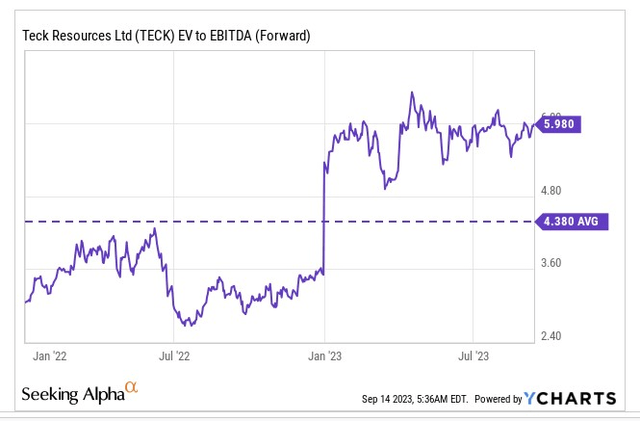

Do consider, that as things stand, the stock is already priced at a premium forward EV/EBITDA multiple of 6x, a +36% variance over its 5-year average. Admittedly, there will be some investors who are prepared to take the long view and pay a higher multiple for what is likely to be a less-diversified, low-carbon business over time, but this is a business that is characterised by regulatory, and construction roadblocks, and long gestation periods, and you’d want to think twice before paying top dollar.

Closing Thoughts – Charting Considerations

If you’ve followed our work for a while, you’d note that we typically use relative strength charts to ascertain the scope of mean-reversion of certain stocks within a certain sector. Ideally one wants to see the relative strength ratio of the stock as a function of that industry, to be trading well towards the lower half of its long-term range.

StockCharts

Well, in the case of TECK, we have the reverse picture, with the stock’s current ratio, relative to a portfolio of global metals and mining producers, trading at over 50% from the mid-point of its zone. Thus, as a rotational candidate within the global metals and mining universe, we don’t believe TECK is a suitable bet at this juncture.

Then switching over to TECK’s standalone price imprints on the weekly chart, what’s rather evident is that the stock is going through a bout of volatility contraction, with its range contracting over time, in the shape of a symmetrical triangle pattern. Note that the contraction in volatility is also validated by a drop-off in the 14-period average true range (ATR) indicator which is down by 23%, and now at levels seen in early February from where we saw a strong directional move. Don’t be surprised to see a similar scenario play out soon enough. Volatility contraction is typically followed by a strong one-way move in either direction, and the catalyst, in TECK’s case, could well be a definitive conclusion of Elk Valley’s next ownership regime.

Investing

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here