By Tony DeSpirito

Q4 for the win? 2023 has offered ample fodder for bears and bulls alike, with each quarter nudging toward the latter. Which will prevail in the year’s final months? As Q4 begins, we see:

- A slim output gap arguing for continued prudence

- Wider gaps in profitability and valuation favoring selectivity

- AI fueling dispersion, disruption, and opportunity

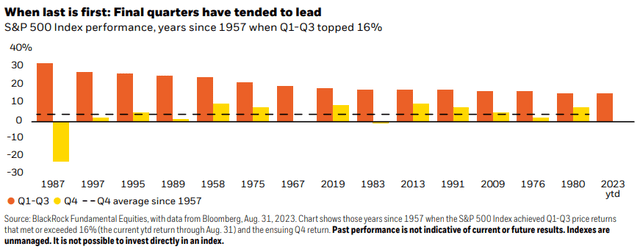

U.S. stocks typically post their best returns in the final quarter of the year. Our review of S&P 500 performance since the index’s inception in 1957 found an average Q4 uptick of 4%. (Q1 was next best at an average of 2%.) In years when performance in the first three quarters came in at or above where we sit year-to-date, index moves in the final quarter were positive in all but three instances, with the October 1987 stock market crash making that year an outlier. See chart below.

We are cautiously optimistic for Q4 2023. The market has already defied expectations and the economy is operating on a slim output gap – meaning all resources are running near full potential. This argues for a continued focus on resilience in equity allocations. Still, because much of the market’s return this year has been driven by a handful of mega-cap stocks in the “tech-plus” sectors, we believe there is an opportunity to uncover those next-level stocks that have yet to be fully rewarded for their fundamentals.

We see smaller reward in making bold calls on the big picture and much greater potential from making good calls on individual stocks.

Tony DeSpirito, Global Chief Investment Officer, Fundamental Equities

Mind the (output) gap

Stock markets turned decidedly more upbeat in July as many strategists adjusted their projections away from recession and toward a “soft landing” scenario for the U.S. economy. While we do not foresee a deep recession, we maintain our view that this is still a late-cycle investing environment and, as a result, a focus on resilience is still warranted in equity portfolios.

The output gap of the U.S. economy, which represents the difference between the economy’s actual versus maximum potential output, is very narrow. The economy is making very efficient use of its existing resources to power the flow of goods and services, with little room to do more and take off running. A key variable is the labor picture, which is quite tight. The unemployment rate stood at just 3.8% as of August. Absent a burst of productivity, the U.S. lacks sufficient additional workers to increase the economy’s output beyond current levels without risking inflation.

GDP figures have held in, inflation readings are coming down and the economy has so far managed to avoid a recession. Yet we still see potential for waning excess consumer savings and the lagged effects of the Fed’s rate-hiking campaign to pinch economic growth and make it harder for companies to grow earnings in the near term.

Late-cycle playbook

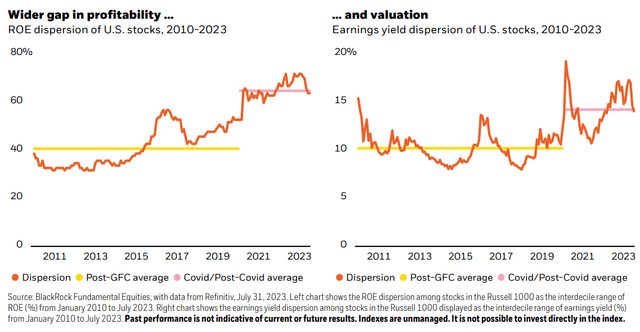

Against this backdrop, we believe it is prudent to stick with the late-cycle playbook in equities, as the economy has yet to embark on a new cycle of post-recessionary growth. This implies diversifying risk exposures and focusing on companies with solid balance sheets and durable business models. The key, and the complication after the market’s strong run year-to-date, is to find them at attractive valuations. The good news is that the very narrow market that had prevailed in the first half, with the seven largest stocks dominating S&P 500 return, has started to broaden – a healthy sign for the market and a good environment for stock picking. Year-to-date, some of the weakest performers with the most compressed valuations have been low-volatility, low-beta stocks.

We also observe a trend toward increased market dispersion. This is evident in returns – a larger gap between top and bottom performers – but even more so in the return on equity (ROE) and valuations across individual stocks, a phenomenon not isolated to the U.S. The charts below show the uptick in dispersion since the period of moderation (low rates, inflation, and volatility) after the Global Financial Crisis (GFC) and the new investment regime in formation since the Covid crisis. Skilled stock pickers can capitalize on these growing gaps in seeking to identify and populate portfolios with shares of companies that demonstrate the fundamental wherewithal to deliver growing earnings across time.

Generative AI essentials for investors

Generative AI (genAI) has commanded attention and moved markets this year, earning comparisons to the internet and smartphone for its transformative potential. We believe genAI is also setting up to be a key contributor to market dispersion, as it has the potential to send some businesses soaring while disrupting or displacing others. We sponsored some internal debate on the topic and offer the following observations on this critical innovation:

Worthy of excitement

Universal application

Unlike other technology innovations that had fleeting fame before fading to the background, we see genAI having farreaching and lasting impact. Leaders of our technology team believe its usage is poised to be unprecedented relative to prior innovations with more limited scope (e.g., 3D printing, augmented reality, metaverse). The key distinction: GenAI is a platform with elements of humanlike intelligence that give it universal applicability that can extend across industries, businesses, and disciplines.

Companies selling the “picks and shovels” of the AI gold rush are the initial beneficiaries. The early rewards for users are likely to take the form of cost savings – eliminating some jobs while making humans more efficient at others. Later in the AI evolution, we expect to see the emergence of new revenue-generating business models.

Investment opportunity now – and for years to come

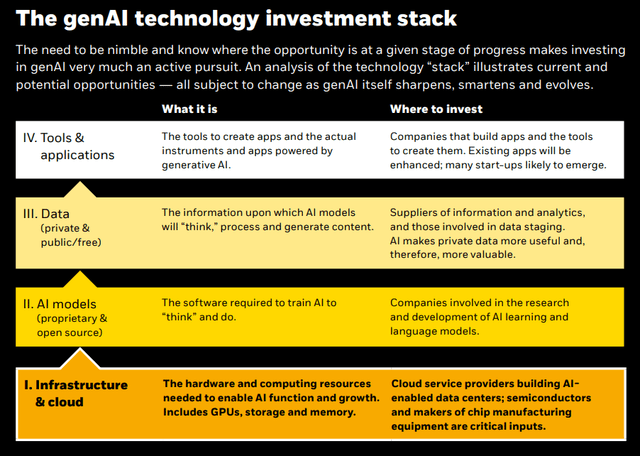

GenAI is evolving and the realization of its full merit will take time, making this a multi-decade opportunity. Yet companies are spending real money on genAI now in an effort to harness its enormous potential. In the building phase, the investment opportunities reside primarily in the technology space. The key is to know where we are in the AI lifecycle and what portions of the technology “stack” may be positioned to benefit.

One case in point: The substantial investment in the current internet, which is powered primarily by CPU chips, will transition toward GPUs (the graphics processing units that are optimized for AI). We see the creation of an AI-supported web driving years-long investment opportunities.

Not a tech-only story

Beyond the impacts and opportunities in the technology sector are the eventual use cases for AI that will emerge throughout the economy. Call centers will likely be replaced. Elsewhere, the uses may be less transformative and more nuanced, such as an AI-powered co-pilot added to an existing software package. We see public and private investment opportunities from AI, with many early-stage opportunities perhaps best expressed through private investments.

Warranting awareness

Great expectations

Given high valuations in the first part of the technology stack, some AI-related stocks could be vulnerable to disappointment, even from just a slowdown in the rate of growth. A shortage of critical chips (GPUs) has allowed companies that make them to temporarily earn an abnormally high margin, posing a risk once supply catches up to demand and competition kicks in. Business history is riddled with stories of supply shortages that eventually turned to supply gluts.

In general, the early stages of a technology hype cycle include a lot of excitement and speculation, yet innovations in their infancy are difficult to value. Constant monitoring is required to assess whether expectations are aligned to the financial and fundamental realities. Questions around the unknown but inevitable regulation of AI globally also complicate the calculus.

Build it and they will come?

In past cycles, new technologies were not always fully utilized after the structures to support them were built. AI’s universality could make this time different. Another critical element to the functioning of AI for enterprises and organizations is data. While AI models can be trained on public data, that data must be enriched with the proprietary kind to make decisions for a particular business. This is an area where many organizations are hamstrung due to insufficient, unorganized, or siloed data, potentially slowing or limiting AI uptake.

Capital chasing the unknown

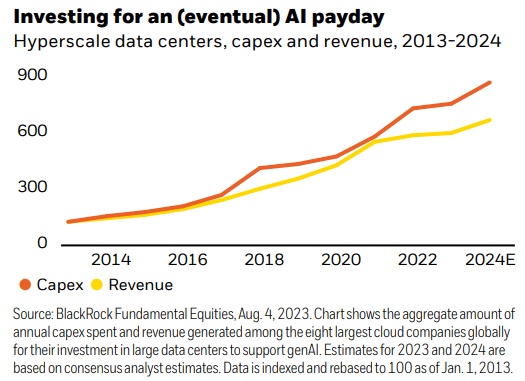

Capital expenditures on genAI have increased in advance of the revenue it generates. See chart on the following page. A key question is whether companies will follow through and use the services to sustain the wave of spending. Some of the early investment may constitute FOMO (fear of missing out) – companies don’t want to fall behind if they fail to invest in a winning innovation. But businesses will have to assess whether AI, for the productivity boost it offers, is worth continuous spend – investing less on hype and more on ROI (return on investment) calculations.

Regardless of whether there is a near-term hiccup, the long-term potential for AI is bright. As the amount of data increases and the cost of processing it comes down across time, we expect AI will continue to grow. Yet AI applications will ultimately meet with varying degrees of success, suggesting genAI could contribute to dispersion across individual companies and their stock prices.

Final reflections

We see generative AI on an improvement curve with prospects to transform businesses around the world, much like the internet has over the last quarter of a century. Yet it is precisely because genAI is new, exciting, and evolving that we cannot take a static approach to the investment thesis. As fundamental-based stock pickers, we are continually fact-checking the investment case as the cycle around generative AI advances from peak expectations to enlightenment and productivity. The genAI story has only just begun and, we expect, will be written for many years to come.

The development of AI is as fundamental as the creation of the microprocessor, the personal computer, the Internet, and the mobile phone. Entire industries will reorient around it. Businesses will distinguish themselves by how well they use it.

– Bill Gates, “The age of AI has begun,” March 2023

This post originally appeared on the iShares Market Insights.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here