Investment thesis

Our current investment thesis is:

- SWK is a high-quality business, with a strong portfolio of brands, a reputation for quality and durability, a diversified revenue profile, and a strong capital allocation strategy that involves supporting organic growth with M&A.

- The business has faced significant headwinds in recent quarters, contributing to a decline in growth and margins, as spending declines and inventory has built up. We expect issues to remain in the near-term, until uncertainty around rate/inflation subsides.

- We expect the business to focus on margin improvement and deleveraging in the coming years, before enjoying an improvement to growth through industry tailwinds.

- SWK’s valuation does not suggest sufficient upside currently to currently compensate for the risk associated with immediate financial improvement.

Company description

Stanley Black & Decker (NYSE:SWK) is a leading global provider of hand tools, power tools, and engineered solutions for various industries. Headquartered in New Britain, Connecticut, the company operates through three business segments: Tools & Storage, Industrial, and Security.

Brands (SWK)

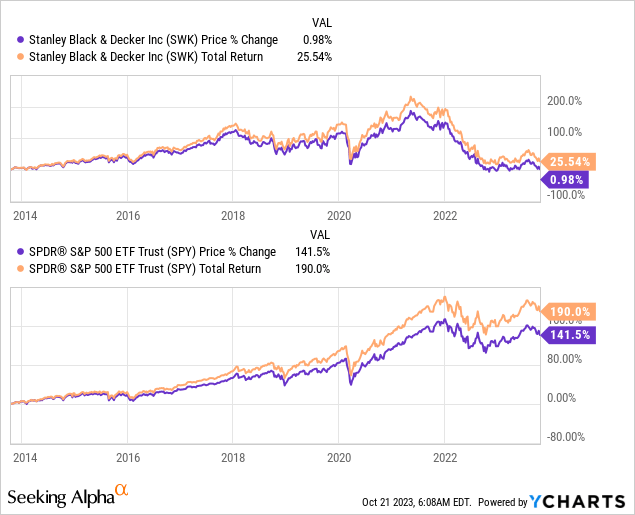

Share price

SWK’s share price performance during the last decade has been underwhelming, with a significant underperformance relative to the S&P. The share price was on an impressive trajectory into 2022, driven by strong financial performance, but this has subsequently deteriorated following a softening of the market.

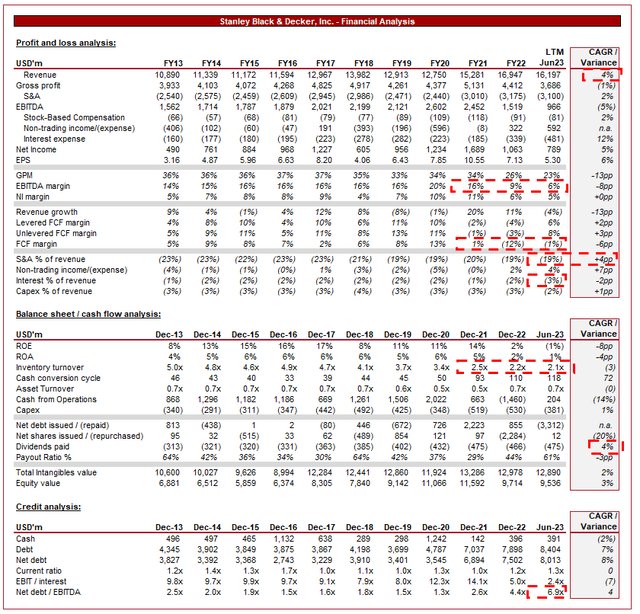

Financial analysis

Stanley Black & Decker Financial analysis (Capital IQ)

Presented above is SWK’s financial performance in the last decade.

Revenue & Commercial Factors

SWK’s revenue has grown at a healthy CAGR of 4% during the last 10 years, with generally consistent growth Y/Y, barring 2 fiscal years of negative growth (excl. pandemic-impact years). M&A has materially supported this growth trajectory, with over $8bn in cash spent during this period.

Business Model

SWK’s business model centers around delivering innovative tools and solutions to its customers.

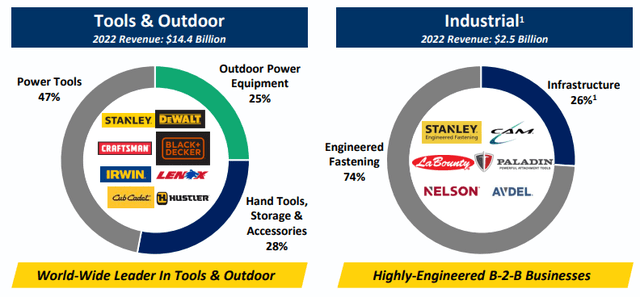

SWK operates in multiple business segments, including Tools & Storage, Industrial, and Security.

- The Tools & Outdoor segment focuses on hand tools, power tools, and storage products for both professional and consumer markets.

- The Industrial segment offers engineered fastening systems and infrastructure solutions.

This diversified portfolio enables the company to operate a high-quality revenue profile, serving various industries and customer segments, reducing reliance on any single market. This diversification is achieved through SWK’s brands, allowing each business to specialize in an industry/segment, while also developing its brand through an expansion of products.

Reach (SWK)

SWK faces intense competition from both established players and emerging companies in its various markets, particularly from low-cost producers from the far east. This competition has threatened pricing and market share, although the trajectory of margins and growth in the run-up to 2020 implies SWK has successfully responded to this.

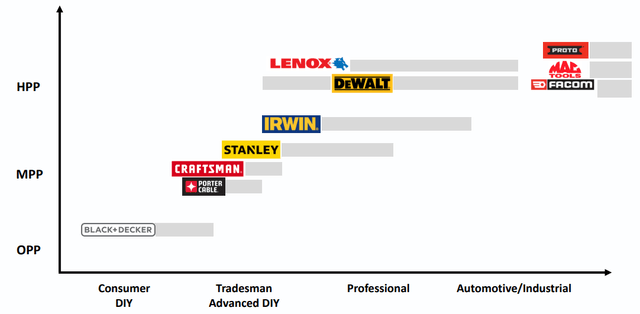

SWK owns a portfolio of well-established and trusted brands, including Stanley, Black & Decker, DeWalt, Craftsman, Lenox, and more. These brands are known for their high-quality, durability, and range of products. This contributes to customer loyalty and recognition, enhancing the company’s competitive advantage in the market. The creation of tools, to an extent, is commoditized, especially in the affordable (DIY) segment. Brand value contributes a significant degree to SWK’s competitive position relative to other factors.

Brands (SWK)

These brands operate on a global scale, with a large portion of its revenue earned from outside the US. This positions the business well for international expansion and supports the continued development of its brands. Many of the global production businesses will default to leading brands, such as SWK’s. With continued economic development and infrastructure spending in emerging markets, SWK is positioned well to seeing improving growth.

Geographical (SWK)

The company emphasizes innovation and invests significantly in research and development to introduce new and improved products. Continuous innovation helps Stanley Black & Decker stay at the forefront of technological advancements, driving customer demand and market differentiation. This is a critical component to maintaining its current trajectory, with its size and relative spend ensuring the business always stays ahead.

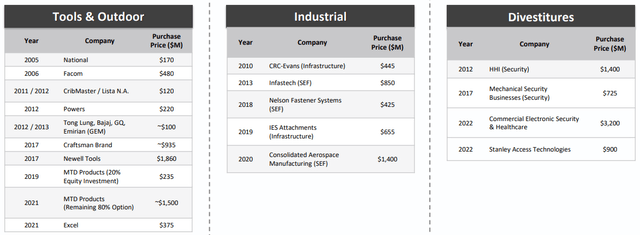

Over an extended period, SWK has made numerous acquisitions to expand its product portfolio and global footprint. The successful integration of acquired businesses is essential for sustainable growth, given the maturity of the industry.

Transactions (SWK)

The business has a strong execution track record, with M&A underpinning its overarching growth strategy. The business looks to acquire businesses that support its current portfolio, allowing for shared competencies and other economies of scale, as well as synergies. Further, where the business is expanding its industry reach, SWK will seek related segments to ensure it maintains a good understanding of the market it is entering. Our expectation is for continued capital allocation to this segment, with Management’s objective being 1/2 of FCF.

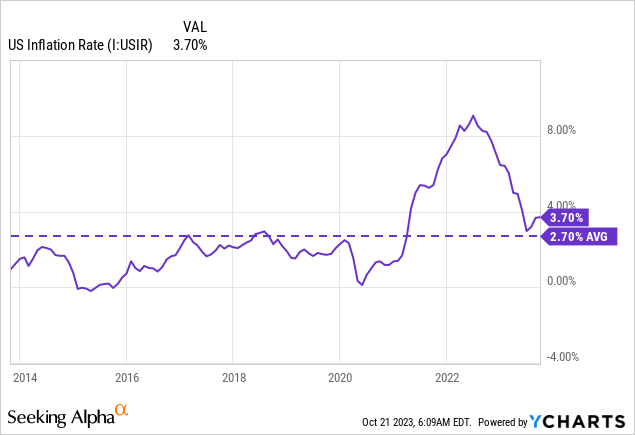

In some of SWK’s core markets, such as the tools and power equipment segment, there is increased saturation, limiting opportunities for significant growth. For this reason, the ability to outperform is predicated on the successful execution of M&A and exploitation of growth opportunities. The average US inflation rate during the last 10 years was 2.65%, implying a modest level of outperformance through M&A given the level of competition.

Economic & External Consideration

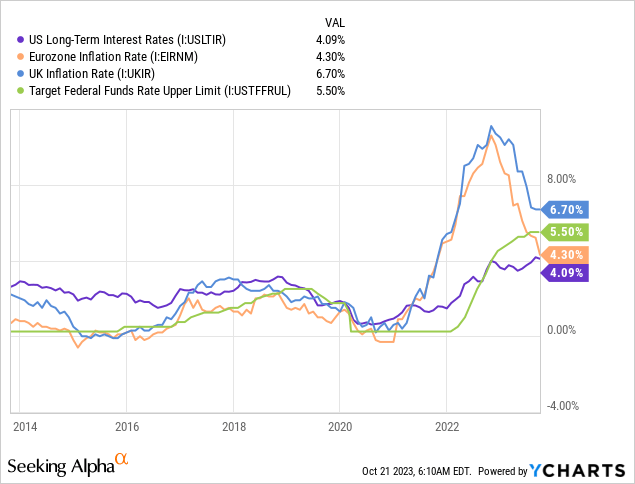

SWK is facing short-term headwinds due to current economic conditions, defined by high inflation and elevated interest rates. This has contributed to a rapid change in conditions following a decade of record low rates, with the cost of borrowing substantially higher and consumers facing a squeeze on finances.

This has contributed to reduced spending by consumers on large ticket purchases, seeking to defend finances. Further, corporations and governments are reducing capital expenditure, owing to both affordability and outlook.

This has negatively impacted SWK as the business is inherently cyclical, benefiting from economic development and driving capital spending on infrastructure.

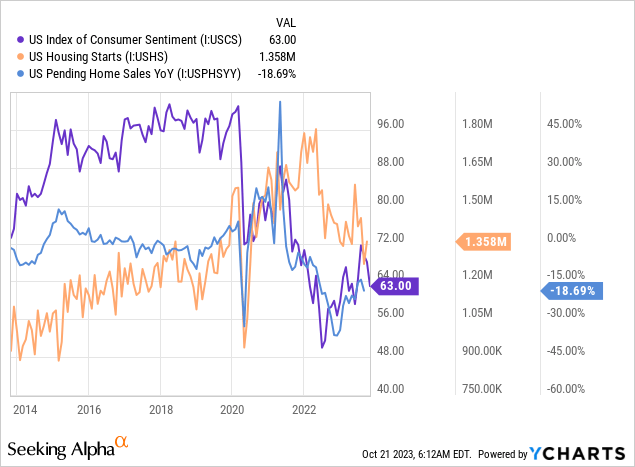

The home building/renovation industry is particularly important to the growth of SWK. With consumer sentiment low and financing costs high, we have seen a sharp reduction in home sales and new housing starts. As a result of this, the demand for equipment will likely remain low in the short term.

This has contributed to a decline in SWK’s revenue, with successive quarters of negative growth and 7 successive quarters of operating profit declining. We expect this to continue in the near term as conditions remain difficult, unwinding in 2024.

There are reasons to be bullish in the medium term, however, as Western Governments and Corporations push for new infrastructure spending (Cloud infrastructure, Semiconductor production facilities, Battery factories, etc), led by the US Infrastructure Bill. This has the potential to drive industry tailwinds with increased spending in the West, supporting what should be strong demand in Emerging markets (Such as much of Asia, India, and LatAm).

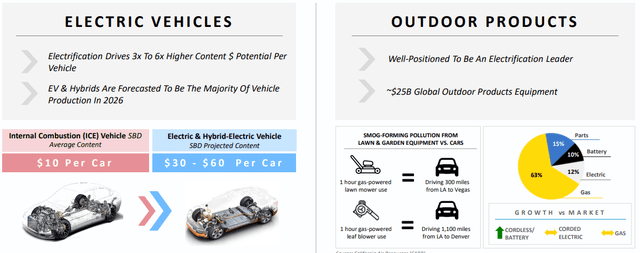

Further, the business has positioned itself well for the electrification transition, currently led by the EV segment, with growth driven by replacement expenditure.

Electrification (SWK)

Margins

SWK has seen a dramatic decline in margins, with EBITDA-M falling from 20% in FY20 to 6% in LTM Jun23. During most of the decade, however, margins had been trending up, peaking in FY20.

The decline in margins is driven by a number of factors. Firstly, rising raw material and labor costs due to inflationary pressures, as well as the build-up of inventory.

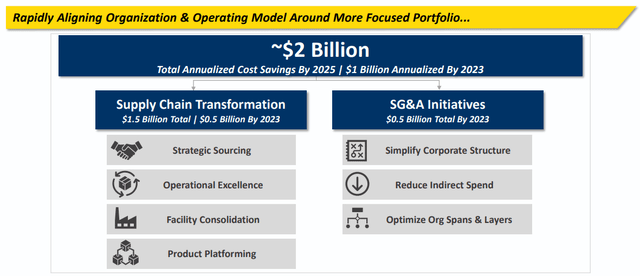

Management is committed to a rapid turnaround, and much of this will be quickly won back as headwinds subside and demand improves. Further, with a continued focus on direct-to-consumer e-commerce sales, the business will enjoy an upswing. However, it remains uncertain where the business will land following this.

Cost-saving initiatives (SWK)

Balance sheet & Cash Flows

The inventory build-up is illustrated by its turnover, which has declined from 4.7x in Dec19 to 2.1x in Jun23. Management continues to net dispose of stock QoQ, alleviating cash flow constraints at the cost of margins but this level remains far too low. Management must bring this in excess of 3.5x quickly, otherwise may need to raise more debt to find cash flows.

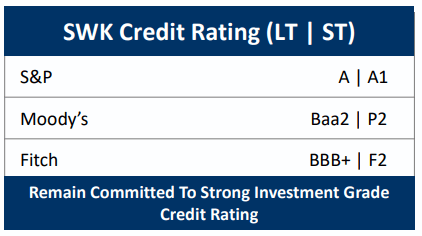

SWK has found itself bloated with debt, with a ND/EBITDA ratio of 7x. This was done to cover the cash flow deficit in recent years, as well as to maintain its current distributions and M&A strategy. This leaves the business forced to rapidly deleverage during a period of economic weakness and high debt costs. Fitch recently downgraded the business to a BBB+, with interest coverage at a measly 2.4x.

Debt rating (SWK)

We do not like the position SWK finds itself in and will likely mean the coming 3-5 years are spent slowly righting the problems created in recent years. If we look at FY19’s cash flows, it is clear this debt can be wiped out quickly if margins return to a good level, but this will take time in itself to achieve.

Industry analysis

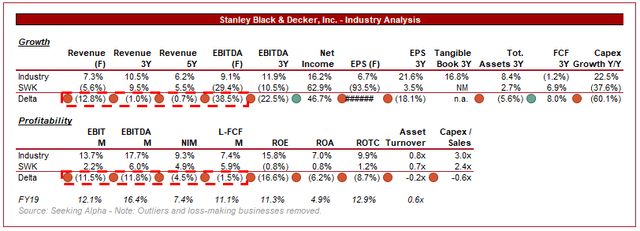

Industrial Machinery Stocks (Seeking Alpha)

Presented above is a comparison of SWK’s growth and profitability to the average of its industry, as defined by Seeking Alpha (55 companies).

Note, a comparison of SWK’s margins at its current level will not look good due to the current depression in its margins. This is not a sustainable level and so partially an unfair comparison. For this reason, we will refer back to its FY19 level, a level SWK will seek to get back to quickly.

SWK’s revenue growth has marginally lagged the industry average, a good level in our view when considering the size of the business relative to its peers. For context SWK is the second largest business in the cohort, contributing to increased difficulty with achieving growth in a mature industry.

As discussed, SWK’s margins are noticeably below the average. If we compare SWK’s FY19 level, the company is far closer to the average, although remains below. This is a reflection of the products it sells, with value driven purely by its brand. This compares to many of its peers who sell highly specialized products and so have a greater weighting toward innovation.

Valuation

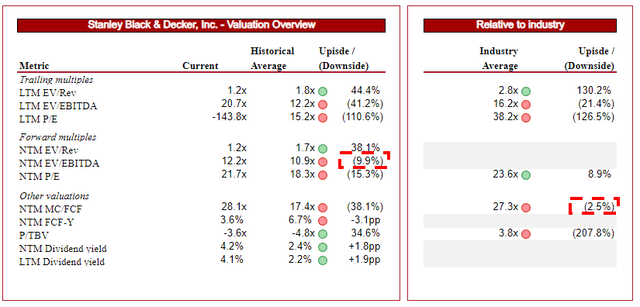

Valuation (Capital IQ)

SWK is currently trading at 21x LTM EBITDA and 12x NTM EBITDA. This is a premium to its historical average.

Once again, given the margin issues faced in recent quarters, we do not consider the LTM metrics to be useful in the slightest, so will be ignored.

On a NTM basis, SWK is trading at a premium to its peer group (MC/FCF) and historical average. We struggle with the size of this premium. If we rewind time to before margins declined, there is a strong argument to suggest SWK warrants a premium to its historical average. Tailwinds are ahead in the industry, margins were on an upward trajectory, M&A was supporting growth well, and the company’s other financial metrics were strong. This is still the reality of the business, but not today. Once it can improve margins and deleverage, which we believe it will, SWK can return to this trajectory. Now, however, investors face execution risk and must be compensated for that.

The peer group comparison is more difficult to assess. The business is slightly lacking in both margins and growth, but compensates for this in size we feel. Many of its peers are restricted somewhat by the niche nature of what they produce. SWK on the other hand has a far longer runway. For this reason, we would suggest a small premium to the market.

Based on this, SWK looks reasonably valued. At a ~10% NTM EBITDA premium to its historical average and a ~3% premium to its peer group’s NTM FCF multiple, we see the stock slightly undervalued 5-10% (essentially pricing in minimal execution risk).

Final thoughts

SWK is a great business which at any other point in time, we would strongly argue is a staple in any portfolio. Consistent dividend growth, strong M&A execution, gradual margin improvement, industry tailwinds, and a strong competitive position.

Unfortunately, the metaphorical wheels have come off and the business is a mess. We do not doubt Management’s ability to execute a turnaround, but there is lasting damage. Deleveraging is needed in order to provide the flexibility to allow M&A to continue alongside distributions.

We suggest patience

Read the full article here