Robert Half (NYSE:RHI) provides talent solutions on a global scale. The company has achieved quite stable earnings along with moderate growth in its long-term history. On a more recent timescale, Robert Half has experienced difficulties in keeping up a good earnings level as Q3 results saw a large decrease both in the company’s revenues and operating margin. I believe that the financial turmoil is priced into the stock already and have a hold rating for the stock.

The Company & Stock

Robert Half provides talent solutions through the Contract Talent Solutions and Permanent Placement Talent Solutions. Of the two, the Contract Talent Solutions represents a clear majority with around 87% of the Talent Solution segment’s complete revenues. In addition, the company has the Protiviti segment, which offers an array of consulting services.

The company is a particularly large operator in the hiring industry in the United States, and has a good foot hold internationally. Robert Half was incorporated in 1948, giving the company time to scale into its current form. The company’s large scale is demonstrated by the company’s amount of employees – in Robert Half’s 2022 year report, the company boasts full-time employees of 16300 across around 400 locations. I believe that the large scale provides Robert Half with benefits in terms of industry knowledge as well as because of the networking effect.

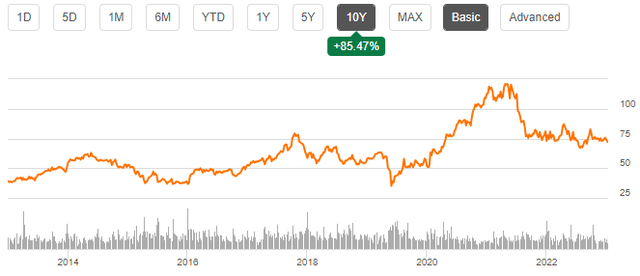

Over the past ten years, Robert Half’s stock has appreciated at a CAGR of 6.4%. On top, the company has had a growing dividend for the past 17 years, with the current yield being 2.66%. In total, the company’s return has been very decent.

Ten-Year Stock Chart (Seeking Alpha)

Financials

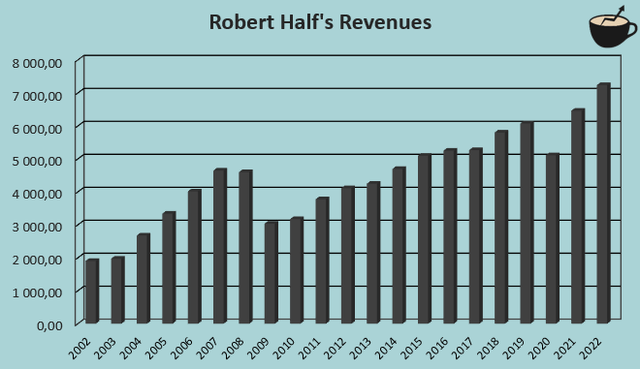

Robert Half has a good financial history in terms of revenues. The company has achieved a compounded annual growth rate of 6.9% from 2002 to 2022 with mostly stable increases:

Author’s Calculation Using TIKR Data

The exceptions to the revenue growth trajectory have mostly been due to global crises – revenues saw decreases only during the great financial crisis in 2008 and 2009, and during the Covid pandemic in 2020. As a third exception, Robert Half is currently facing a tough period as customers are prolonging the decisions around hiring; for 2023, analysts currently expect revenues to decrease by 11.3%.

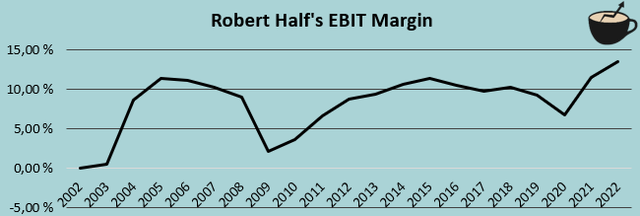

The company’s margin history has been mostly good, although the company did see EBIT margin decreases from 2015 to 2019 on top of the financial crises:

Author’s Calculation Using TIKR Data

From 2002 to 2022, Robert Half’s average EBIT margin has been 8.3%. The margin history has been mostly growing, as in 2022 the company achieved an EBIT margin of 13.5%. Currently, the margin is seeing some pressure as revenues are decreasing, but I believe that the margin should eventually recover along with revenues.

I believe that Robert Half’s balance sheet is even unnecessarily strong. The company doesn’t have any interest-bearing debt, and the company currently has a cash balance of $729 million. Robert Half hasn’t been active in acquisitions, so I don’t see it probable that the company uses the cash balance in a strategic acquisition. The company does pay out a dividend and has some share buybacks, but dissolving the cash balance seems to progress rather slowly. Also, drawing long-term debt could provide a cheaper form of financing for the company, which I would like to see from Robert Half.

Reported Q3 Results

Robert Half reported the company’s Q3 results on October 24th in the post-market. The reported earnings were very poor, yet in line with analysts’ already low expectations. The company had revenue decreases of -15% and an EPS decrease of -41%. The company’s issues stem from the current economic uncertainty – in Robert Half’s Q3 earnings call, the company’s CEO related the issues to hiring caution and a decrease in career moves.

In the company’s Q3 earnings call, the management also provided a guidance for Q4. The provided guidance is revenues of $1.415 billion to $1.515 billion, corresponding to a year-over-year decrease of -15% with the middle point of the guidance. The guidance also includes an EPS guidance of $0.75 to $0.89, with the middle point EPS of $0.82 representing a year-over-year decrease of -40%; Robert Half’s financials turmoil is far from over.

Valuation

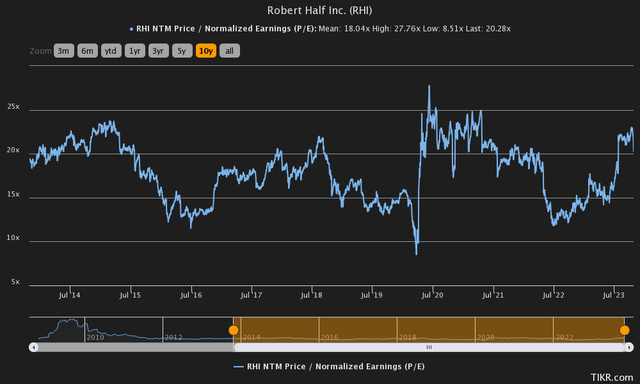

Currently, Robert Half trades at a forward P/E of 20.3, slightly above the ten-year average of 18.0:

Historical Forward P/E (TIKR)

The ratio seems rather high as considering the current interest rate and Robert Half’s financial turmoil. The ratio is partly explained by analysts’ expectations, though – currently, analysts still estimate the company’s financials to be very significantly below Robert Half’s level before the revenue decreases. With a sustainable long-term earnings level, the P/E ratio would seem more reasonable.

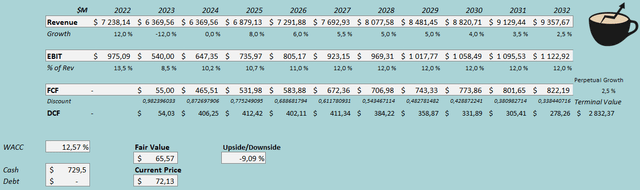

I constructed a discounted cash flow model to further analyse the valuation and to estimate a rough fair value for the stock. In the model, I estimate Robert Half to hit its Q4 guidance representing revenue decreases of -12% for the entirety of 2023. In 2024, I still estimate Robert Half’s market to stay difficult at least in the first half – I estimate revenues to stay stable in the year. In 2025 and beyond, I expect the company to recover and to get back into the company’s historical growth. I estimate a growth of 8% for 2025 that slows down in steps into a perpetual growth rate of 2.5%.

Robert Half is currently facing pressures to the company’s margin. For 2023, I estimate the company’s EBIT margin to decrease by five percentage points into a figure of 8.5%. After 2023, I believe that Robert Half should be able to scale its margins back into a level that’s closer to the achieved 2022 level. For 2024, I estimate a margin of 10.2%, that increases further in 2025 and beyond into an EBIT margin of 12.0% in 2027.

The mentioned estimates along with a cost of capital of 12.57% craft the following DCF model with a fair value estimate of $65.57 around 9% below the price at the time of writing, representing a very slightly overvalued stock:

DCF Model (Author’s Calculation)

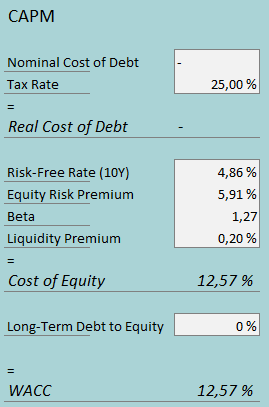

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

Robert Half doesn’t leverage debt in its financing and hasn’t done so in a very long period on a significant level. I believe that the company should leverage debt as a method of cheaper financing than equity financing, but I don’t see the company drawing debt in the foreseeable future; I have a long-term debt-to-equity ratio estimate of 0%.

On the cost of equity side, I use the United States’ 10-year bond yield of 4.86% as the risk-free rate. The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the US, made in July. Yahoo Finance estimates Robert Half’s beta at a figure of 1.27. Finally, I add a small liquidity premium of 0.2% into the cost of equity, crafting a cost of equity and WACC of 12.57%.

Takeaway

Robert Half is currently facing a tough market as customers are prolonging hiring decisions and the labor market is slower than in previous years. As the issues subside, I believe that the company should be able to grow back into its previous earnings level and continue on the modest growth path. Yet, I don’t expect too much of an opportunistic future from Robert Half – the company doesn’t leverage debt in its operations, and doesn’t seem to be active in M&A as the company no significant cash acquisitions from 2013 forward. Currently, the stock seems to be priced fairly, constituting a hold-rating.

Read the full article here