Reviva Pharmaceuticals Holdings (NASDAQ:RVPH) is a biotech developing the antipsychotic brilaroxazine. The antipsychotic activity of the drug demonstrated in prior clinical work has led the company to run a phase 3 clinical trial in schizophrenia, that is set to produce results in October, 2023. That trial, and RVPH’s financial situation are the focus of this article.

The RECOVER trial

On September 25, RVPH announced it had evaluated the last patient in its phase 3 RECOVER trial of brilaroxazine in schizophrenia. To make predictions about whether or not the study will succeed, it is worth looking at the phase 2 data for brilaroxazine.

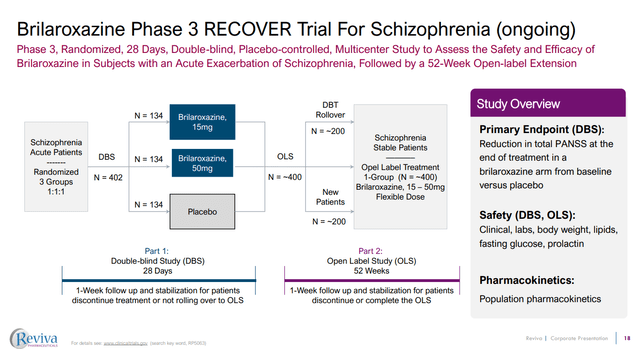

Figure 1: Design of the RECOVER phase 3 study of Brilaroxazine. (RVPH Corporate Presentation, September 2023.)

The phase 2 study

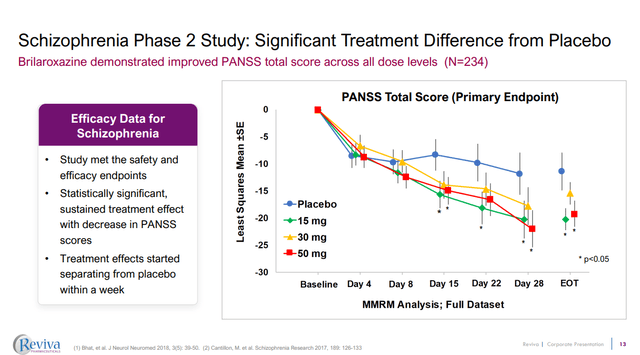

In a previous phase 2 study the company randomized 234 patients with schizophrenia or schizoaffective disorder to 15, 30 or 50 mg brilaroxazine, aripiprazole (Abilify) or placebo in a 3:3:3:1:2 ratio. The company obviously wanted to collect more data with brilaroxazine while having only a small aripiprazole comparator arm. As a result the number of patients in each group was 58, 59, 58, 20 and 39. Having just 20 patients in the aripiprazole might be what led to an interesting result.

The primary endpoint was the change from baseline to day 28 on the Positive and Negative Syndrome Scale (PANSS) total score. The placebo group saw a -11.41 point change from baseline to day 28, while the 15 mg brilaroxazine (-20.23 point change) and 50 mg brilaroxazine (-19.21) groups saw significantly greater reductions than placebo. The aripiprazole (-9.32) did not beat placebo, even numerically. It is a bit funny for an approved antipsychotic not to beat placebo but again, having only 20 patients in this group might be part of the problem. RVPH doesn’t plot the aripiprazole date in its recent corporate presentation, perhaps it has previously, but they can be found in the publication of the trial results. Notably, even the 30 mg brilaroxazine group, while not being statistically different to placebo, still achieved a -15.42 point change. A further potential reason for aripiprazole failing to separate from placebo could be a higher baseline PANSS total score (91.7 for aripiprazole vs 89.9 for the placebo group).

Figure 2: Results on the primary endpoint from a phase 2 study of brilaroxazine. (RVPH Corporate Presentation, September 2023.)

In any case it seems pretty clear brilaroxazine is an active antipsychotic, which isn’t that surprising given it is a chemical relative to aripiprazole and brexpiprazole (Rexulti), two marketed antipsychotics, and share features in terms of its pharmacology that make it similar to many other antipsychotics.

The largely ex-US recruitment of patients to the phase 2 study should also be noted; India (46%), The Philippines (26%), Malaysia (18%), Moldova (5%), and the US (5%). RVPH’s phase 3 study is referred to as “global” in its September 25, press release. The US clinical trials entry for the RECOVER trial only lists US sites, 18 to be exact, but a search of the EU Clinical Trials Register for “brilaroxazine” brought up an entry for the phase 3 study in Bulgaria, where it appears there are 8 sites, and it also mentions the study being run in India and the United States.

The phase 1 study

In an earlier phase 1 study in stable patients with schizophrenia (n=32) patients received brilaroxazine at 10 mg (n = 8), 20 mg (n=6), 50 mg (n=6) and 100 mg (n=6), or placebo (n = 8), but only for 10 days. A publication discussing the clinical experience with brilaroxazine thus far notes that while the brilaroxazine patients when pooled as a group, didn’t separate from placebo on the PANSS total score, there were some subgroups that demonstrated efficacy.

Notably, in those with PANSS total score ≥ 50 at baseline, the drug seemed to show some benefit on PANSS positive scores. A baseline PANSS total score of 50 is still well below what was seen in the phase 2 study, where the average baseline score was closer to 90. As such comparing the phase 1 data to the phase 2 data simply shows that running a small study in stable patients (PANSS score > 90 were excluded in the phase 1 work) for 10 days isn’t going to be a great way to show off antipsychotic efficacy. I don’t think the phase 1 efficacy data is worth getting into more because of that.

RECOVER is likely to hit the primary endpoint

Regarding the potential for success of the phase 3 study, beating placebo in a phase 3 trial with a drug closely related to other antipsychotics, that has already shown antipsychotic efficacy itself, doesn’t seem too farfetched. I don’t know how much of a rally that alone would provide to the stock, since there are other antipsychotics out there.

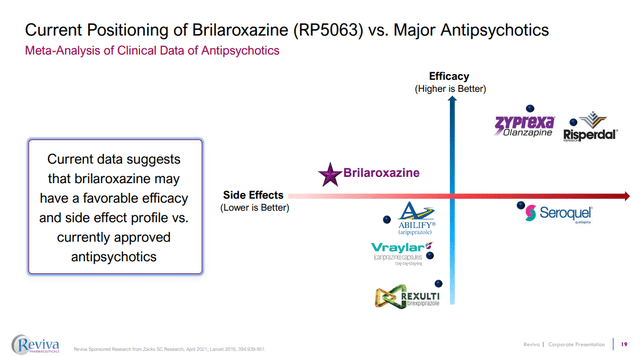

Figure 3: RVPH’s brilaroxazine may offer a unique profile in terms of side-effects to efficacy compared to other popular antipsychotics. (RVPH Corporate Presentation, September 2023.)

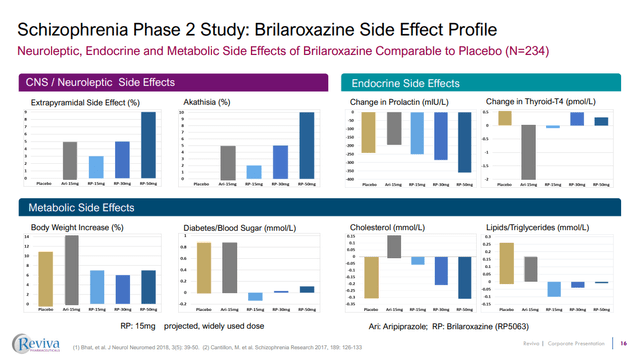

RVPH is clear however that what brilaroxazine might have to offer is a differentiated profile in terms of side effects, whilst still offering the efficacy of many other antipsychotics. For example, the phase 2 work showed that while body weight increases were seen in patients treated with placebo, aripiprazole and brilaroxazine, the increases were less in patients treated with brilaroxazine.

Figure 4: Comparison of side effects following treatment with brilaroxazine, aripiprazole or placebo. (RVPH Corporate Presentation, September 2023.)

The problem I see there is that RECOVER doesn’t include an aripiprazole arm and so we’ll be left with cross-trial comparison to see how brilaroxazine looks versus other antipsychotics. Still I do think some cross trial comparisons are pretty obvious and if brilaroxazine causes less weight gain than placebo, then it is going to look better than a lot of antipsychotics which show more weight gain than placebo. As such, RVPH does have a chance to point out some clear points of difference for brilaroxazine.

Financial Overview

RVPH finished Q2’23 with $11.15M in cash and cash equivalents and reported a net loss of $12.44M for the quarter. R&D expenses were $8.99M in Q2’23 and G&A expenses were $3.08M in the same quarter. Net cash used in operating activities was $13.27M in the first six months of 2023 and so at the current rate of burn, RVPH would be out of cash by the end of the year. Of course completing the clinical trial should greatly reduce R&D expenses and allow RVPH to continue along a little longer if it needed to. That discussion would of course be moot if RVPH impresses the market with its phase 3 results allowing it to raise more cash, but if the trial fails, RVPH thinning out its remaining funds is relevant.

There were 22,650,266 shares of RVPH’s common stock outstanding as of August 11, 2023, corresponding to a market cap of $108.95M ($4.81 per share). At June 30, there were 6,325,000 shares worth of public warrants outstanding (RVPHW, exercise price $11.50), another 1,939,712 shares worth of private warrants (substantially similar to the public warrants), 6,645,041 shares worth of investor warrants (exercise price $4.125), 1,383,399 shares worth of private pre-funded warrants and 120,456 shares worth of assumed warrants. These warrant types are discussed further in RVPH’s recent 10-Q.

Figure 5: Potentially dilutive securities as of June 30, 2023 (left most column). (RVPH 10-Q for Q2’23.)

Along with ~1.5M shares worth of options and 1M shares worth of shares issuable for earnout, there are over 17M shares worth of dilution outstanding. That being said, the exercise of these warrants, except the prefunded warrants, can serve as a substantial source of funds for RVPH. For example, during Q2’23, 1,976,285 shares worth of warrants associated with a 2022 private placement were exercised resulting in proceeds of $4.74M for RVPH.

In any case, it is possible RVPH conducts another private placement or some other sort of fundraising activity if it produces successful phase 3 data.

Conclusions and Risks

I see RVPH’s phase 3 RECOVER trial as having greater than a 60% chance of beating placebo, and it’ll probably do it at both doses. I think the drug looks good on its side effect profile too, and an obvious cross trial comparison on body weight, for example, might show the company has something. I rate RVPH a buy, but there are some downside scenarios that need to be considered.

Firstly, if the trial fails, the stock would probably fall to cash which is about 90% below current prices. If the drug doesn’t work, it is dead in the water. I view an outright failure, i.e., neither the 15 mg or 50 mg dose of brilaroxazine beating placebo, as unlikely. That is how I am able to rate the stock a buy, despite the potential downside of 90%. Nonetheless, an outright failure could occur.

Secondly, even if the drug succeeds at one or more doses on the primary endpoint, the side effect profile might show the drug doesn’t look as good as it did in the phase 2 study. The stock could still fall then, as while the company might claim positive results, criticism of the drug as being undifferentiated on side effects could see any pop from a “positive” press release as short-lived.

Lastly, RVPH could report positive efficacy findings and an apparently differentiated side-effect profile vs many other antipsychotics, but still fail to rally over funding concerns. Or an offering could be announced with the results that has already been priced at a price close to the current trade price.

Read the full article here