Earlier this year, we covered Realty Income (NYSE:O) in an article titled: “Realty Income: Over 30%+ Upside To Fair Value“.

The main thrust of that article was that the company was significantly undervalued vs. cash flows on a straightforward basis.

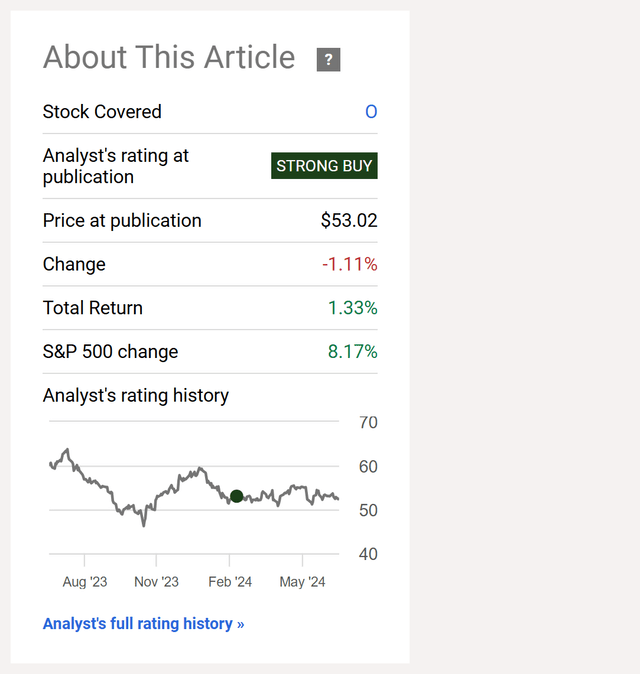

While the company has produced a positive total return since our ‘Strong Buy’ rating, it’s trailed the S&P 500’s appreciation of 8%+ over that span:

Seeking Alpha

Fast-forward to the present, and the company continues to grow top line and bottom-line results at a solid pace, but the stock remains stuck around the $50 mark. This is likely frustrating to investors who have been watching other sectors like big tech race higher for the first half of this year.

Despite this, we still think O is one of the most compelling opportunities on the market.

Today, we wanted to revisit the company, examine O’s growth prospects, and ultimately explain why we still believe in the story and consider O a ‘Strong Buy’.

Let’s dive in.

O’s Financials

In case you’re new to O (which is unlikely), the company is a popular Real Estate Investment Trust, which is a specific type of corporation that owns and invests in real estate.

O’s core business is commercial real estate, with a focus on retail. This means the company owns buildings that mostly house grocery stores, convenience stores, dollar stores, drug stores, quick service restaurants, and the like.

The company currently owns 16,414+ properties, which are spread across the US, UK, and Europe.

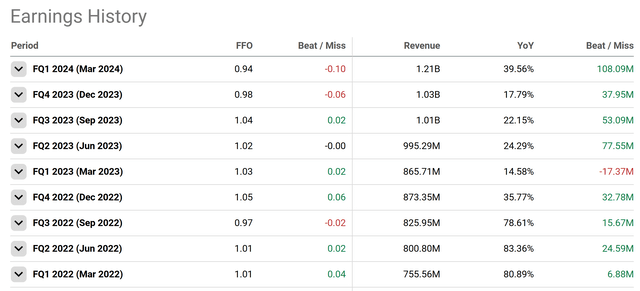

Since our first article, O released Q1 earnings, which missed on FFO but beat on top line revenue:

Seeking Alpha

While the FFO miss was largely disappointing, YoY revenue growth of nearly 40% was a welcome beat on the back of portfolio expansion, high rent recapture rates, and continued execution on the part of management.

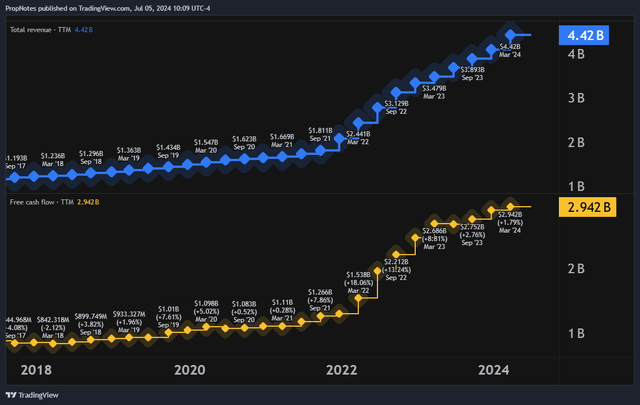

Zooming out somewhat, you can see the impact of recent M&A on O’s financial growth, which has been robust:

TradingView

Top-line growth has been strong, and AFFO has been climbing as O’s portfolio has swelled with new properties that have begun producing cash flows.

Stepping back for a second, there are a number of things that you could look for when analyzing a stock, but for us, in this case, there are three core reasons we like O as a ‘Strong Buy’ investment:

Best in class diversification.

Best in class growth.

A multi-decade low in the multiple.

Add these up, and we think there’s serious upside room here.

Let’s start with O’s diversification.

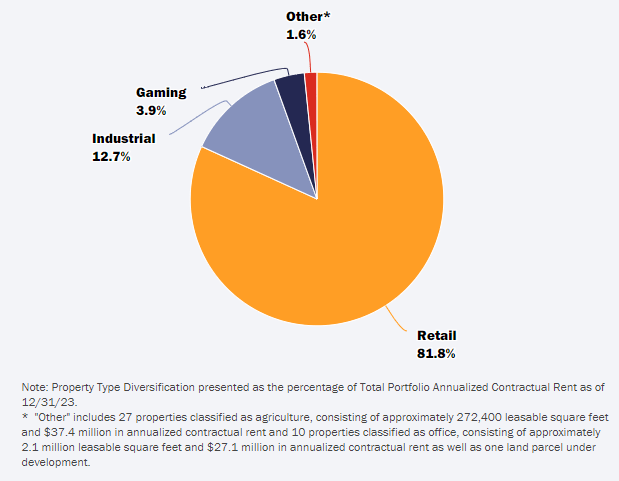

While we mentioned that the company owns a lot of property, we didn’t touch on many specifics, so let’s take a look at that now. As we stated in our first article, the real estate that O owns is generally well diversified across industries and geographies:

The company owns 15,450 commercial properties across the USA, UK, Ireland, Spain, and Italy, primarily in the retail segment, although the company does maintain some industrial & gaming (Casino) exposure as well:

Realty Income

From these properties, O generates revenue and cash flow from long term (15 year+) lease agreements, which has remained both a lucrative and stable business model over time.

The business model has led to very high tenancy and collection rates, even throughout downturns, and as the portfolio continues to grow, we only see this (dare we say ‘fortress’) balance sheet getting stronger.

No tenants account for more than 1% of revenue, which is highly impressive in the real estate world, and only 5% of tenants are on some sort of credit watch list.

In our view, the current portfolio is absolutely top tier when it comes to size and safety.

However, aside from the top-level portfolio stats, management has proven themselves to be opportunistic, which is a strong leading indicator that we really like.

Of the recent investments made by O in Q1, a good chunk of them were focused on the UK and Europe. Some may view this as a bad move given the weaker overall economic situation in those regions, but we see it as a ‘buy low’ opportunity.

You can see this bear out in the stats, as O was able to secure higher yields on these investments vs. domestic deal flow:

During the first quarter, we invested $598 million at an initial weighted average cash yield of 7.8% across three property types: retail, industrial and data centers. Over half of this volume representing approximately $323 million was invested in Europe and the U.K. at an 8.2% initial weighted average cash yield.

This proves to us that O continues to hunt for the best uses of capital and is willing to make disciplined investment decisions with shareholder money over long stretches of time. For a long-term investment, this is exactly what you’re looking for.

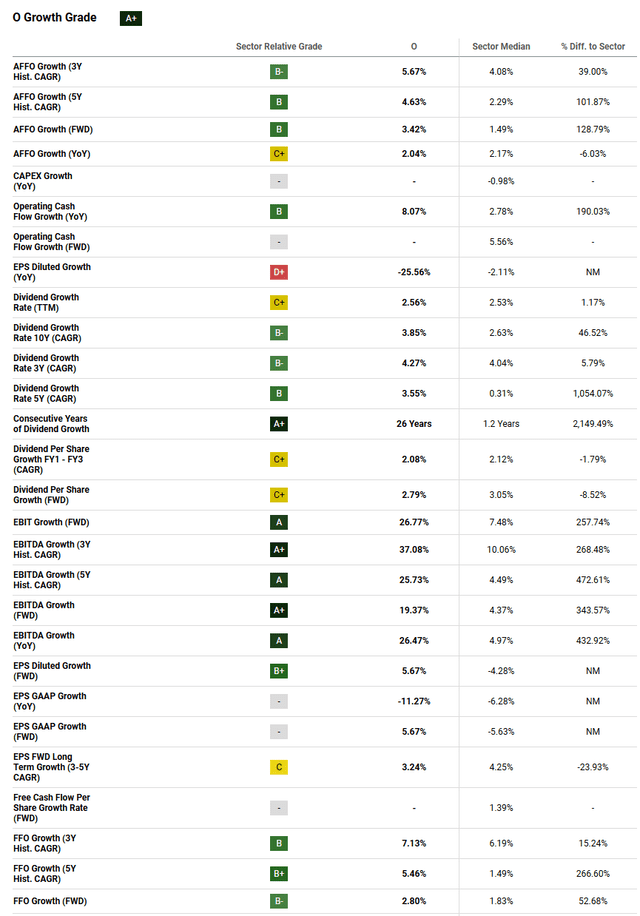

While O is clearly well diversified and de-risked, it may also surprise you that the company is delivering best-in-class growth:

Seeking Alpha

Seeking Alpha’s quant score rates O’s growth profile as ‘A+’, which means that it is one of the fastest growing companies within the Real Estate sector. The screenshot above doesn’t cover all of the growth metrics that SA’s system tracks, but we couldn’t fit it all in a picture.

Suffice it to say that growth rates across the board are strong.

Zooming in a bit, a perfect encapsulation of this growth can be found in O’s forward-looking AFFO growth figure, which stands at 3.42%. As fed interest rates have gone higher and the economy has worsened over the last 12-18 months, AFFO growth rates across the industry have dropped due to weaker pricing power on rents and higher costs of capital.

Right now, the industry average sits at around 1.5%, and so O’s expected growth rate is actually more than double the market on the most key metric for the sector.

Management appears even more bullish than analysts, but we think that the projected 4.3% AFFO per share growth will be difficult given the company’s high level of dilution:

Our projected 2024 operational return profile of approximately 10%, which comprises an anticipated dividend yield close to 6% and AFFO per share growth of approximately 4.3%, assuming the midpoint of guidance is a validation of our value proposition.

Either way, O’s big portfolio gives it a lot of scale advantages when it comes to reinvesting FFO and capital recycling that allow it to optimize at better-than industry rates.

Combined, O’s efficiency and diversification make it a tough company to match in the commercial real estate industry.

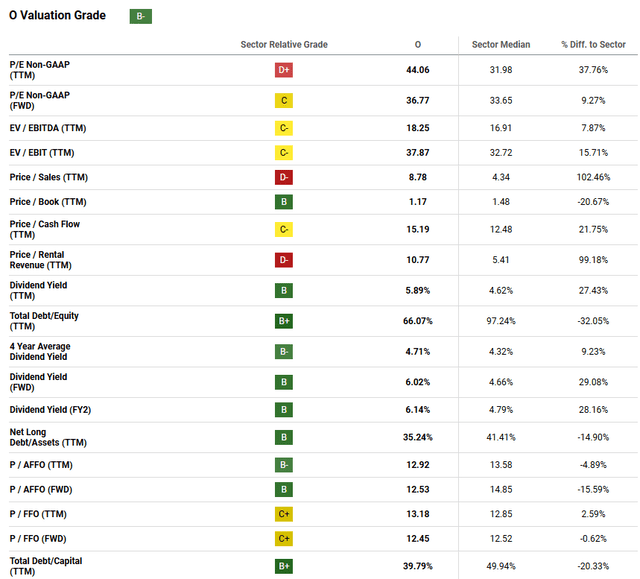

O’s Valuation

One would normally expect a company with this profile to come with a premium price tag, but this isn’t the case with O. Historically, the company has traded in the 17-20x AFFO range, which is a historical premium.

However, that isn’t the case right now.

Not only have shares come off of that range considerably, but they’re also lower than the market averages, which simply doesn’t make that much sense when viewing the company’s performance and capital allocation strategy in full:

Seeking Alpha

O receives a ‘B-‘ valuation rating from SA’s quant system, but we think that the grade should probably be a bit closer to an ‘A’ or ‘A-‘.

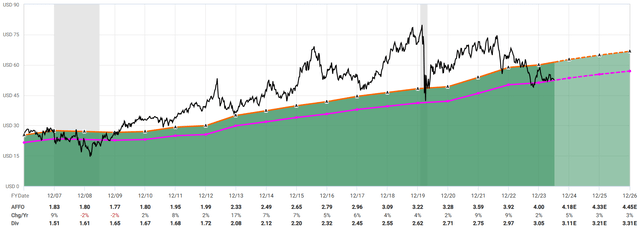

At 12.5x forward AFFO, O is trading at multi-decade lows that it hasn’t seen since the financial crisis.

Brad Thomas showed this in a recent article with a chart that we really liked, and so we’ve reproduced it for you below:

FAST Graphs

Here’s the thing – even during Covid, O didn’t trade at such a discount. This is a strong indication that now is the time to strike.

Broadly, we feel like there’s a general sense that investors are getting more skeptical about O’s dealmaking skills, but we believe there isn’t much data to back that assertion up. This perception has likely in part led to the discount.

Ultimately, if the market was perfectly priced all the time, there wouldn’t be any great opportunities.

Between the multi decade extreme on the multiple, the growth profile, and the incredible diversification, O appears to be very, very well positioned for long-term total returns that outperform the market.

Risks

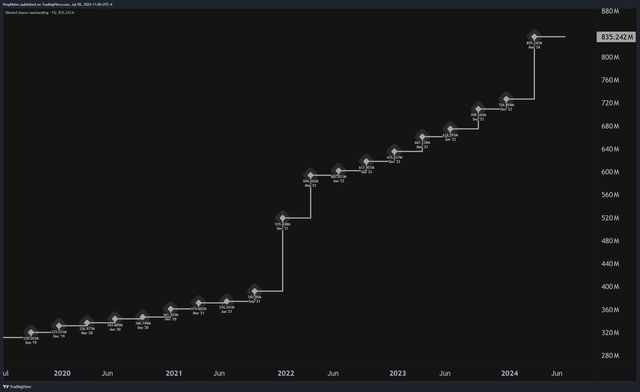

The key risk here is around dilution.

No matter how strong the financials are, or how high quality the asset pool is, if the company is funding growth with dilution, then it’s going to be an uphill battle for capital appreciation.

Since the merger in 2022, O has been favoring funding deals and new investments with dilution, which has weighed heavily on the stock price:

TradingView

As debt has gone out of style due to the interest rate environment, O’s constant tapping of the equity market has led to stagnant prices for investors.

Here’s the thing, though – even though the diluted share count has more than doubled over the last 5 years, we can’t argue that it’s been a misallocation of capital.

As O’s cost of capital has increased on the debt side, the company has increasingly looked at equity’s around 6% cost of funding as an attractive way to get deals over the line. It hasn’t been the best over the short term as far as supply and demand goes, but over the long term we think it’s actually not that big a deal and could be accretive to shareholder value.

Additionally, management has said that they likely won’t need to tap markets as frequently going forward:

This leaves us with approximately $63 million of outstanding equity available for future settlements. And when combined with approximately $825 million of annualized free cash flow available to us following the Spirit merger, and the disposition program that Sumit referenced, our $2 billion investment guidance for the year is one, we believe can be funded without having to tap the markets.

However, while management’s appetite for diluting shareholders does appear to be slowing down a bit, there’s no question that if it picks back up, then there could be more downside in the stock. This is a key risk to monitor, and ultimately, the cost of growth.

Summary

However, all in all, we think that O’s profile is incredibly attractive, and sustained double-digit returns into the end of this decade doesn’t seem like an ‘out of reach’ goal.

The stock has disappointed so far in 2024, but don’t let that distract from the excellent long-term opportunity with this real estate behemoth.