While Street Earnings overstate profits for the majority of S&P 500 companies there are many S&P 500 companies whose Street Earnings are lower than their Core Earnings.

This report shows:

- The frequency and magnitude of understated Street Earnings in the S&P 500.

- Five S&P 500 companies are likely to beat 3Q23 earnings.

Street Earnings refer to Zacks Earnings, which are adjusted to remove non-recurring items using standardized sell-side assumptions.

Street EPS Are Lower Than Core EPS for 136 S&P 500 Companies

For 136 companies in the S&P 500, or 27%, Street Earnings are lower than Core Earnings in the trailing-twelve-months (TTM) ended 2Q23. In the TTM ended 1Q23, Street Earnings were understated for 146 companies.

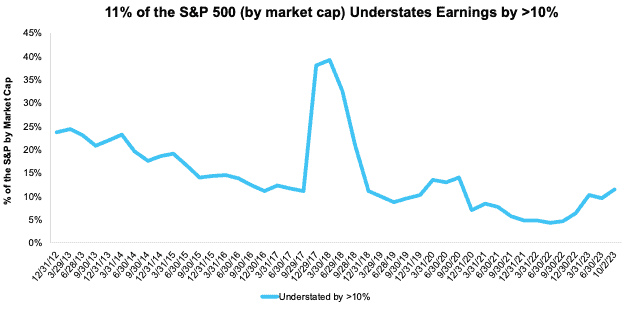

The percentage of the S&P 500 where Street Earnings understate Core Earnings by more than 10% fell to 9% (47 companies) in 2Q23, which is down from 10% (51 companies) in the TTM ended 1Q23.

Those 47 companies make up 11% of the market cap of the S&P 500 as of 10/2/23, which is up from 10% of the market cap in 1Q23, measured with TTM data in each quarter. See Figure 1.

Figure 1: Understated Street Earnings by >10% as % of Market Cap: 2012 through 10/2/23

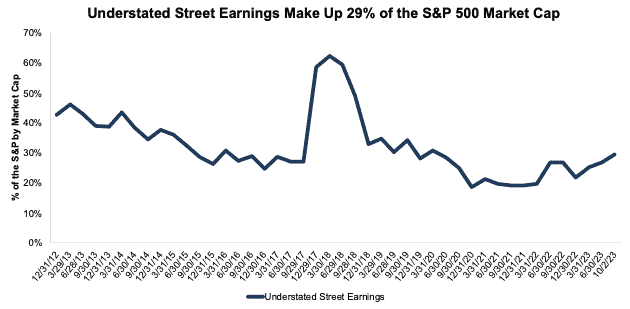

The 136 companies with understated (by any amount) Street Earnings represent 29% of the market cap of the S&P 500 as of 10/2/23, which is up from 27% in the TTM ended 1Q23. See Figure 2.

Figure 2: Understated Street Earnings as % of Market Cap: 2012 through 10/2/23

When Street Earnings are lower than Core Earnings, they are understated by an average of 28%, per Figure 3.

Figure 3: Street Earnings Understated by 28% on Average in TTM Through 2Q23

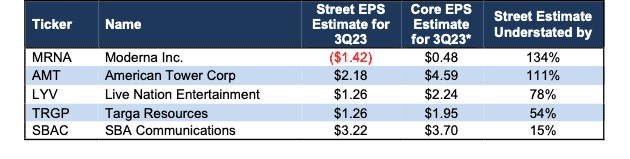

Five S&P 500 Companies Likely to Beat Calendar 3Q23 Earnings

Figure 4 shows five S&P 500 companies likely to beat calendar 3Q23 earnings because their Street EPS estimates are understated. Below we detail the hidden and reported unusual items that caused the understated Street Earnings in the TTM ended 2Q23 for American Tower Corp (AMT).

Figure 4: Five S&P 500 Companies Likely to Beat 3Q23 EPS Estimates

*Assumes Street Distortion as a percentage of Core EPS is the same in 3Q23 as the TTM ended 2Q23.

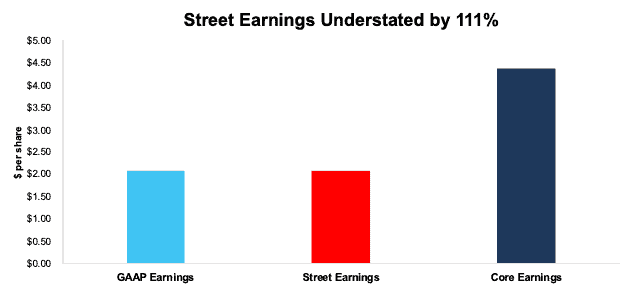

American Tower Corp: The Street Underestimates Earnings for 3Q23 by 111%

The Street’s 3Q23 EPS estimate of $2.18/share for American Tower Corp is $2.41/share lower than our estimate for 3Q23 Core EPS of $4.59/share. Large foreign currency losses and impairment charges included in historical EPS drive most of the difference between the Street and Core EPS estimates. After removing these unusual expenses, our analysis of the entire S&P 500 reveals American Tower Corp as one of the companies most likely to beat Wall Street analysts’ expectations in its 3Q23 earnings report.

American Tower Corp’s Earnings Distortion Score is Beat. Despite a short-term likelihood to beat earnings expectations, AMT does not provide quality risk/reward over the long term. American Tower’s Stock Rating is Unattractive, in part due to its low return on invested capital (ROIC) of 5%, negative economic earnings, and market-implied growth appreciation period (GAP) of >100 years.

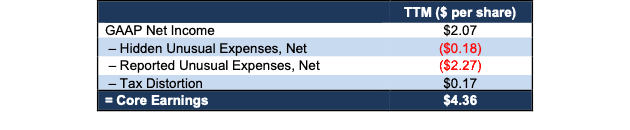

Below, we detail the unusual expenses that materially reduced American Tower’s TTM 2Q23 Street and GAAP Earnings. After removing all unusual items, we find that American Tower’s TTM Core EPS is $4.36/share, which is higher than the TTM Street and GAAP EPS of $2.07/share.

Figure 5: Comparing American Tower’s GAAP, Street, and Core Earnings: TTM Through 2Q23

Figure 6 details the differences between American Tower’s TTM Core and GAAP Earnings, so readers can audit our research. Given the small difference between GAAP and Street Earnings, the adjustments that drive the difference between Core and Street Earnings are likely mostly the same.

Figure 6: American Tower’s GAAP Earnings to Core Earnings Reconciliation: TTM 2Q23

More details:

Total GAAP Earnings Distortion of -$2.29/share, which equals -$1.1 billion, is comprised of the following:

Hidden Unusual Expenses, Net = -$0.18/per share, which equals -$85 million and is comprised of:

- -$85 million in acquisition and merger-related expenses and integration costs in the TTM period based on:

Reported Unusual Expenses Pre-Tax, Net = -$2.27/per share, which equals -$1.1 billion and is comprised of:

- -$656 million in impairment charges in the TTM based on -$656 million charge in the 2022 10-K.

- -$376 million in “other expenses” (which are mostly foreign currency gains/losses) in the TTM period based on:

- -$28 million loss on sale or disposal of assets in the TTM based on -$28 million loss in the 2022 10-K.

- -$0.7 million in loss on retirement of long-term obligations in the TTM period based on:

Tax Distortion = $0.17 per share, which equals $78 million.

The $2.29/share of Street Distortion in the TTM ended 2Q23 highlights that Core Earnings account for a more comprehensive set of unusual items when calculating American Tower’s true profitability.

Disclosure: David Trainer, Kyle Guske II, Hakan Salt, and Italo Mendonça receive no compensation to write about any specific stock, style, or theme.

Read the full article here