PureCycle Technologies, Inc. (NASDAQ:PCT) commercializes ultra-pure recycled resin (UPR) processed from polypropylene plastic waste. The company’s proprietary technology stands out by removing all impurities resulting in a UPR resin that is indistinguishable from chemical-based virgin polypropylene. The attraction here is the strong demand by manufacturers across several industry verticals for renewable alternatives.

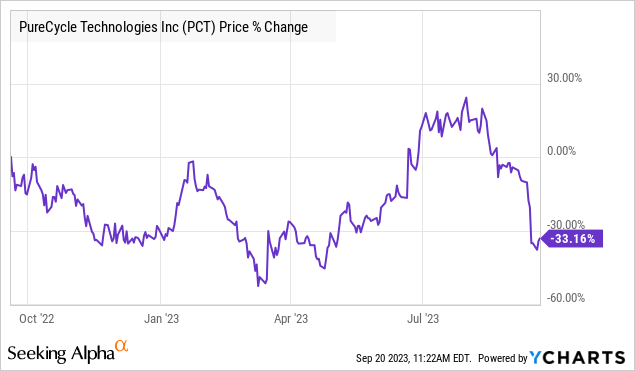

The first point here is that PureCycle’s first facility in Ironton, Ohio is operational, with a future capacity of more than 100 million pounds of UPR representing a major growth runway. On the other hand, profitability remains elusive with cash flow concerns weighing on shares as PCT is down by more than -30% over the past year.

There are plenty of risks but we also see an interesting setup here following the recent selloff. 2024 will be a critical year for the company reaching several operational and financial milestones as a potential catalyst for the stock. Plans for a second site in Georgia while moving forward with an international expansion keep shares interesting.

How is PCT Doing?

PCT reported its Q2 results back in early August with effectively zero revenues and a net loss of -$56 million. That being said, the bigger highlight of the update was on the operational side.

The company began producing the first batch of UPR pellets at the Ironton facility in June in a test run while reiterating a plan to reach 50% capacity by the end of September. This is an important step as PureCycle transitions to a revenue-producing entity with the Q3 data reflecting initial sales.

source: company IR

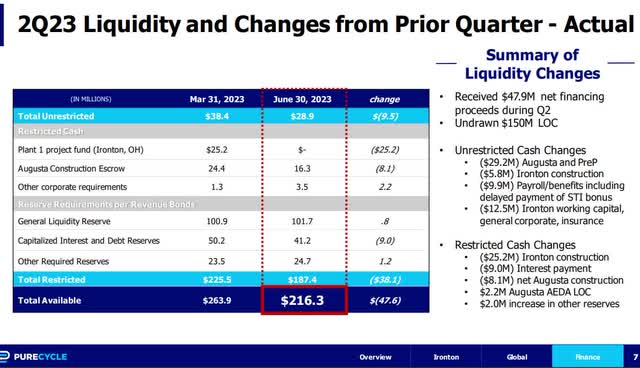

The other key development has been efforts to secure financing. A $150 million revolving line of credit has been extended through March 31, 2025. This is incremental to the $216 million in balance sheet liquidity at the end of the quarter against $247 million in total long-term debt.

Separately, the company raised an additional $215 million in August through the issuance of convertible green notes with favorable terms directed at eligible environmental-related projects. In this case, PureCycle is targeting the development of a new plant in August Georgia with construction activities set to begin in Q4. Overall, management believes it is well-positioned to continue its growth strategy, eyeing the improvement in cash flows going forward.

source: company IR

What’s Next For PCT?

We view PureCycle’s business model as embodying the adage, “If you build it, they will come.” In this case, renewable UPR pellets can be a hot commodity companies are more than willing to embrace at a premium to traditional polypropylene as a productive step to reduce their carbon footprint and reach corporate environmental goals.

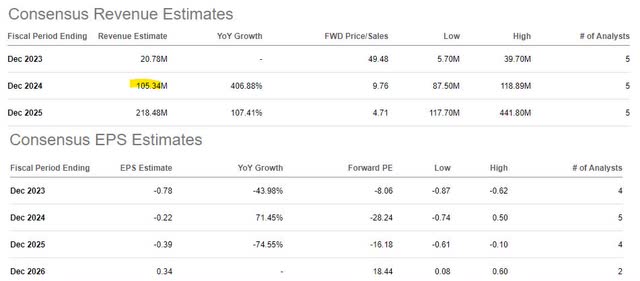

The question becomes how long will it take for PureCycle to reach a scale level where the economics begin to make sense. According to consensus estimates, the forecast is to reach $20 million in revenue this year, which accelerates toward $105 million next year. The net income loss is seen narrowing through this period, with a path to potentially break even or turn positive by 2026.

It’s fair to be skeptical regarding these metrics, but the point is that the expected growth trends are impressive and moving in the right direction.

Entering 2024, a scenario where PureCycle is hitting these benchmarks as hard evidence the strategy is working, we sense that the market would reward the stock with a higher growth premium.

Currently, the forward sales multiple of 10x into the 2024 estimate is elevated, but also reasonable in the context of a company generating over $100 million in sales, that could double again into 2025. There are plenty of companies trading at a higher P/S multiple doing much worse. The momentum narrows that further down to 5x by fiscal 2025 according to market revenue projections.

Seeking Alpha

PCT Stock Price Forecast

We’re bullish on the stock because we believe there are plenty of positive developments that can work as catalysts for the stock. Getting into the Q3 and Q4 update, the potential that management issues forward guidance with 2024 financial targets would go a long way in cementing the commercialization success story.

From the stock price chart, it’s encouraging to see that shares have rallied above the $6.00 price level maintaining a market value above $1 billion. On the upside, we wouldn’t be surprised if shares can retest recent highs above $10.00 given the extreme range of volatility observed over the past year. PCT is speculative, but the bullish case is that the risk-adjusted return potential can justify a position.

Still, the reality here is that there are significant uncertainties in performance metrics like margins and cash flow trends that will start to matter sooner rather than later. The biggest risk facing PureCycle is an execution lapse where a milestone timetable either at Ironton or Augusta gets pushed back. Production volumes and shipment updates will be key monitoring points.

Seeking Alpha

Read the full article here