Overview

My recommendation for Persimmon Plc (OTCPK:PSMMF) is a buy rating, as I expect the stock to trade back to a historical PB multiple as gross margin recovers to a historical level eventually. Management’s hard stance on prioritizing gross margin over growth is certainly encouraging, and I believe the market is reacting positively to this, with the stock up by 7% since the low in August 2023.

Business

Persimmon plc is in the business of building houses. The business has a couple of Our Brands, with the main one being Persimmon, Westbury, and Charles Church. The business focuses on the United Kingdom with nationwide presences and is pretty much tied to the health of the country’s economy cycle as they sell a product that comes with a heavy price tag. In particular, mortgage rates movement impacts the business heavily.

PSN

Recent results & updates

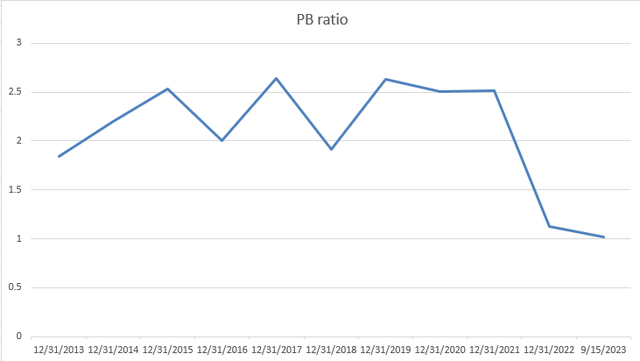

Looking at the PSMMF stock chart, the share price has received a good amount of beating since the early part of this year, dropping from 1531 pence to 1071 pence today, a 33% drop. I believe the stock has dropped to a level where it has become cheap, especially when viewed from its P/B ratio, currently at 1x book vs. the average of 2.1x book over the past 10 years. Based on the 1H23 results and management commentary, I believe the upside case for PSMMF is quite appealing, and I will discuss the positives and negatives ahead.

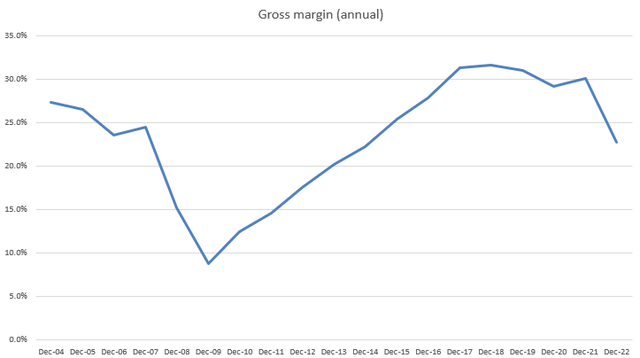

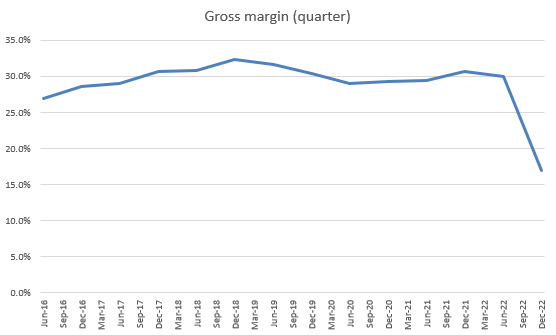

The first and most important point to mention is that management is finally going to prioritize gross margin over growth. Historically, the business has always printed strong gross margin improvements over the years, but has since faced pressure starting in FY19 and during the COVID situation. My thoughts are that this has contributed to a lot of investors’ worry about management’s willingness to chase growth but give up on margins.

Author’s valuation model

Author’s valuation model

Fortunately, in the 1H23 earnings report, management communicated a shift in their priorities. They are no longer emphasizing volume growth at the expense of profit margins. Their focus for the near future is on cost control, but they aim to strike a careful balance between expanding outlets and implementing their restructuring strategy to avoid hindering future growth prospects. This signals to the market that forthcoming growth will be both sustainable and profitable.

Following this period of cost management, I anticipate improvements in profit margins due to management’s dedication to streamlining operations and enhancing efficiency. For example, they have identified opportunities for efficiency enhancement, including £25 million in savings over 2 years by reducing specifications that hold lesser importance for customers, in addition to the planned £25 million in overhead savings resulting from a hiring freeze. Moreover, management is currently evaluating sub-contractor pricing, which is expected to yield further cost reductions as sub-contractors participate in the effort to contain expenses.

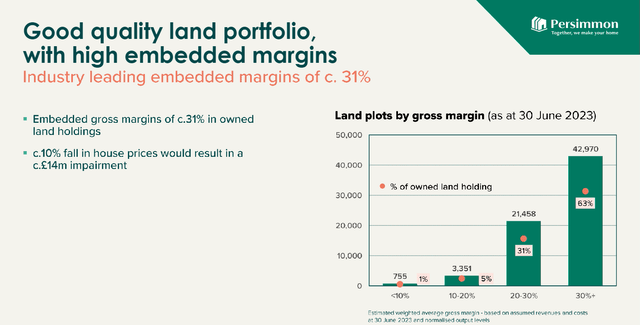

Delving further into the gross margin outlook, I expect PSMMF to experience organic gross margin enhancements, mainly because the gross margins within their landbank remain robust. During the discussion, management underscored that the embedded gross margin within the landbank had risen to 31%, and only a minimal 6% of plots had a gross margin lower than 20%. Furthermore, it caught my attention that PSMMF didn’t place significant emphasis on its reliance on legacy sites. This indicates to me that the quality and depth of their land bank have allowed them to diversify away from these legacy sites. This development is promising because it expands the company’s potential customer base, especially when the economy rebounds.

PSMMF

The unpredictable summer buying season, which is affected by weather, holidays, and product availability, is a near-term risk that could prevent the valuation from recovering. As a result of these factors, it has been observed that sales rates have dropped by 20% to 40% compared to May 2023 levels, albeit being higher than 4Q23 levels.

We’re now in the typically slow summer selling period and our sales rate of 0.41 over the last five weeks reflects that. But pricing has however remained resilient with private average selling prices up 0.9% since the start of the year.

We have over 90% forward sold the market the market is variable. At the moment, we are seeing a summer slowdown, which is perhaps more acute than normal, but it is bouncing around. I mean, for instance, last week we were at 0.53. from: 1H2023 earnings call

Valuation and risk

Author’s valuation model

I value PSMMF on a PB basis, which is now trading at 1x book value. I expect this valuation to revert back to its historical rate of near 2x book value (10-year average) as the business finds its way back to historical gross margin levels. There should be no issues with this happening, as 31% of the landbank has a medium gross margin of 25% and 63% of the landbank has more than 30% gross margin. If we average it out, it suggests a gross margin level of 30% (63% x 35% [my assumption] + 31% x 25% gross margin [mid-point of 20 to 30%]), which is the historical gross margin. Gross margin could even exceed this if the cost savings initiatives play out as expected. Assuming a reversion of the PB ratio from 1x to 2x, PSMMF should be worth 2140 pence in FY25.

The risk is that Europe’s recession just keeps getting worse from here, with no light at the end of the tunnel. This would likely result in a further increase in interest rates, which is not healthy for the industry as the cost of construction and everything else related gets more expensive.

Summary

My recommendation for PSMMF is a Buy rating, driven by the expectation that the stock will return to a historical PB multiple as gross margins recover. Management’s shift towards prioritizing gross margins over growth is a positive development, with the stock already showing a 7% increase since August 2023. Despite the recent stock decline, PSMMF’s current PB ratio of 1x book value appears undervalued compared to the 10-year average of nearly 2x. This undervaluation is expected to correct as the company aims to regain historical gross margin levels. A significant portion of the landbank maintains robust gross margins, which reinforces this outlook.

However, near-term risks include the unpredictable summer buying season and economic uncertainties in Europe. If the European recession worsens, it could lead to increased interest rates, impacting construction costs.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here