Note:

I have covered Performance Shipping (NASDAQ:PSHG) previously, so investors should view this as an update to my earlier articles on the company.

Last year, small Greece-based tanker operator Performance Shipping joined peer Imperial Petroleum (IMPP, IMPPP) and sister company OceanPal (OP) in relentlessly diluting common shareholders at a tiny fraction of net asset value (“NAV”) for the sole purpose of growing their respective fleets.

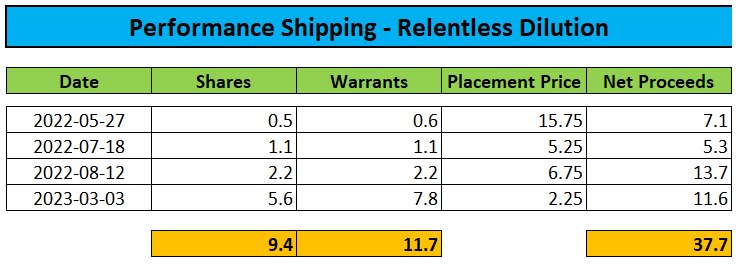

Over the past 18 months, Performance Shipping has raised approximately $37.7 million in net proceeds from a series of equity offerings including warrant sweeteners:

Regulatory Filings

Please note that common shareholders suffered additional dilution (albeit to a lesser extent) from share sales executed under two recent at-the-market offerings.

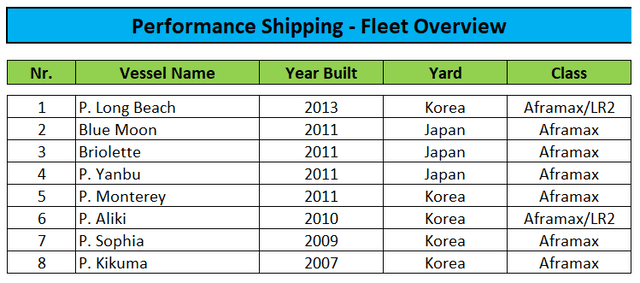

The company has used the funds to expand its tanker fleet to eight vessels with an estimated market value of approximately $350 million:

Company Presentation

In addition, Performance Shipping has ordered a newbuild Aframax/LR2 tanker for a purchase price of $62.2 million with delivery expected in Q4/2025. In April, the company paid the first installment of $9.5 million.

Like other tanker companies with a focus on the spot- and short-term time charter markets, Performance Shipping has benefited heavily from elevated charter rates caused by recent geopolitical events.

In H1/2023, the company generated a whopping $40.8 million in cash from operating activities.

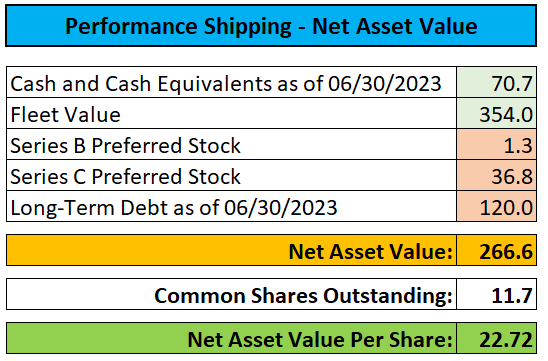

Despite the favorable market environment, Performance Shipping continues to trade at an eye-catching 90% discount to net asset value (“NAV”) as investors remain wary of the company’s tainted past:

Regulatory Filings

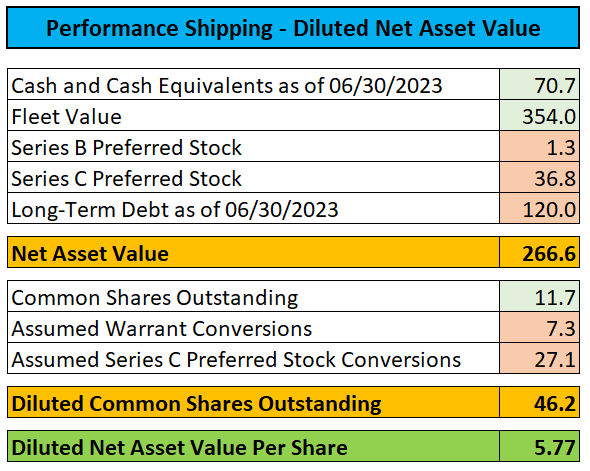

Unfortunately, this number remains subject to material dilution from potential warrant exercises and Series C Convertible Preferred Stock conversions with fully-diluted NAV per share estimated to be below $6:

Regulatory Filings

However, even after the recent rally in the shares, the discount to fully-diluted NAV still calculates to more than 60%.

Over the past couple of months, notorious Greek shipping magnate George Economou has accumulated close to 10% of the company’s common shares in a series of open market purchases and stated his intention to engage in a proxy fight.

On Wednesday, Mr. Economou surprisingly launched a tender offer to acquire all of Performance Shipping’s outstanding shares for $3.00 in cash per share thus causing the stock price to jump by almost 30%.

Investors should note that the offer is subject to a large number of conditions with the majority being solely within the control of the company and its Board of Directors.

Among other things, the offer is conditional upon:

- Mr. Economou being offered the majority of all issued and outstanding common shares on a fully-diluted basis.

- The company removing its poison pill.

- Cancellation of the company’s Series C Convertible Preferred Stock which is controlled by Chairwoman Aliki Paliou and her spouse, CEO Andreas Michalopoulos.

- Mr. Economou being handed over control of the Board of Directors.

But with Ms. Paliou and Mr. Michalopoulos commanding approximately 90% of the voting rights, there’s basically no way for Mr. Economou’s hostile offer to succeed.

Not surprisingly, Performance Shipping is defending vigorously against Mr. Economou’s demands (emphasis added by author):

(…)

Performance Shipping regularly engages with investors and is open minded with respect to value creation opportunities. In that light, we are deeply concerned by the actions taken by Sphinx and its principal George Economou.

Over the last several weeks, Sphinx stealthily took a large position in our stock and has proceeded with increasingly aggressive actions towards the Company, including demanding to somehow eliminate the rights of a broadly-held class of shares, seeking to change our corporate structure, nominating a director candidate to our Board, proposing to remove other directors and demanding a review of our books and records. To date, we have responded promptly, noting our disagreement with Sphinx’s baseless allegations.

Sphinx has done all of this without stating their intentions. We are open to engaging with Sphinx and Mr. Economou as we would with any shareholder. However, given they have taken these steps without being clear about their goals and while hiding behind their lawyers, we can only assume the worst.

Mr. Economou’s record of destroying shareholder value and enriching himself through self-dealing and poor corporate governance speaks for itself. We note that the nominee proposed by Sphinx, John Liveris, has aided Mr. Economou in some of his most egregious transactions, including at Ocean Rig and OceanFreight.

Nonetheless, we stand by to engage constructively with Sphinx to better understand their intentions and our Board will review their proposals and nominees through our normal corporate practices and standards. Assuming the relevant legal requirements are satisfied, our shareholders will have the opportunity to vote on Sphinx’s nomination and proposals at our 2024 annual meeting of shareholders.

It is important to understand that Performance Shipping is building a strong company with significant growth and value creation opportunities. Our Board of Directors comprises highly qualified directors, the majority of whom are independent and all of whom are committed to exercising their business judgment and acting in accordance with their fiduciary duties to the benefit of the Company and all shareholders.

In light of our relatively small market capitalization and to ensure shareholders have the opportunity to realize the full upside potential of their investments in our Company, we established our corporate structure with a classified Board to protect against the types of coercive and hostile actions we are seeing from Sphinx. (…)

At this point, I just don’t see a viable path for George Economou to gain control of Performance Shipping without the consent of the company and its controlling shareholders.

With Mr. Economou’s offer representing an almost 50% discount to fully-diluted NAV, there’s simply no basis for Performance Shipping’s controlling shareholders to consider a deal. On the flip side, there’s no sense in acquiring the company at a price close to NAV so I do not expect Mr. Economou to raise his offer materially.

At least in my opinion, the only way for George Economou to potentially get his hands on Performance Shipping would be to challenge the company’s ownership structure in court which would likely result in a protracted battle with limited prospects of success.

Bottom Line

Things continue to escalate at Performance Shipping with George Economou surprisingly launching a hostile tender offer to acquire all of the company’s outstanding common stock for $3.00 per share in cash.

Please note that the offer is conditional upon the company removing all obstacles to the proposed acquisition which at least in my opinion is not going to happen.

Given this issue, investors shouldn’t bet on the share price approaching the proposed takeover price anytime soon.

Shareholders considering to accept Mr. Economou’s offer should contact their broker in order to make sure that the November 8 deadline will be met.

With little prospects of George Economou succeeding in his battle for control of Performance Shipping and the stock price up by almost 200% since my “Speculative Buy” recommendation in late June, I am downgrading the company’s shares from “Speculative Buy” to “Hold“.

Investors should note that George Economou has also accumulated a sizeable stake in OceanPal, another Palios family-controlled shipping company that was spun off by Diana Shipping (DSX) last year and trades at a similar discount to NAV. However, in contrast to Performance Shipping, Mr. Economou has yet to state his intentions regarding OceanPal.

Risk Factors

Besides a potential deterioration in tanker market conditions, key risks for Performance Shipping’s shareholders are further dilution and particularly George Economou abandoning his current efforts to take control of the company.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here