Investment Rundown

Investing in the natural gas business I think will remain very appealing for decades to come. There is a push towards renewables, but it’s not fast enough to push aside companies like ONE Gas Inc (NYSE:OGS). The company still has a strong asset base and customers are expected to grow further in the coming years much thanks to the metropolitan increased coverage in areas like Austin Texas.

Even with a strong and appealing dividend, the company does not display any value right now in my opinion. For investors who seek a value play in the natural gas industry, I don’t think OGS is there yet. For those who hold shares in the company and want the additional dividend income, I think the fundamental demand and growth trajectory of natural gas prices is going to make that sustainable. This concludes me rating OGS a hold for now.

Company Segments

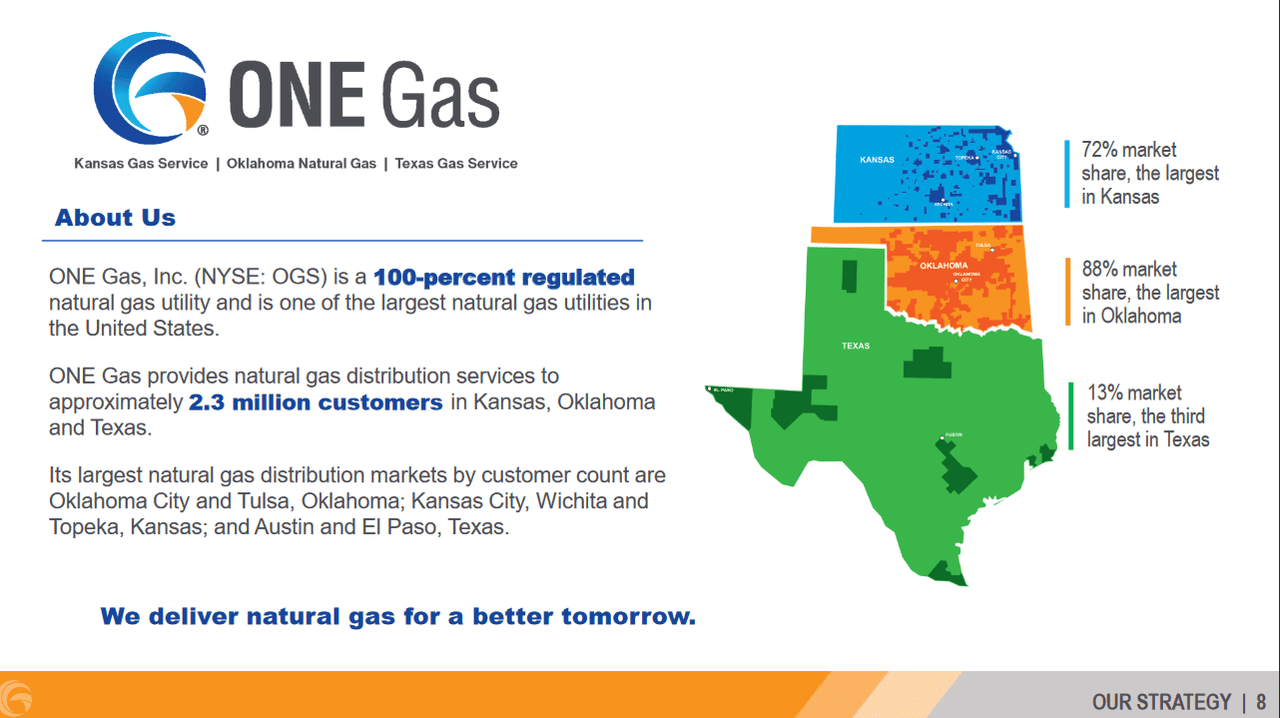

OGS is operating in the regulated natural gas utilities sector within the United States. It operates primarily in regions encompassing Texas, Oklahoma, and Kansas, making it one of the noteworthy pure-play natural gas utility providers nationwide. With a dedicated focus on serving its customers, ONE Gas extends its natural gas distribution services to approximately 2.3 million individuals in total across the regions of operations it has. This diverse customer base includes residential, commercial, and transportation consumers, highlighting the extensive reach and impact of the company’s operations.

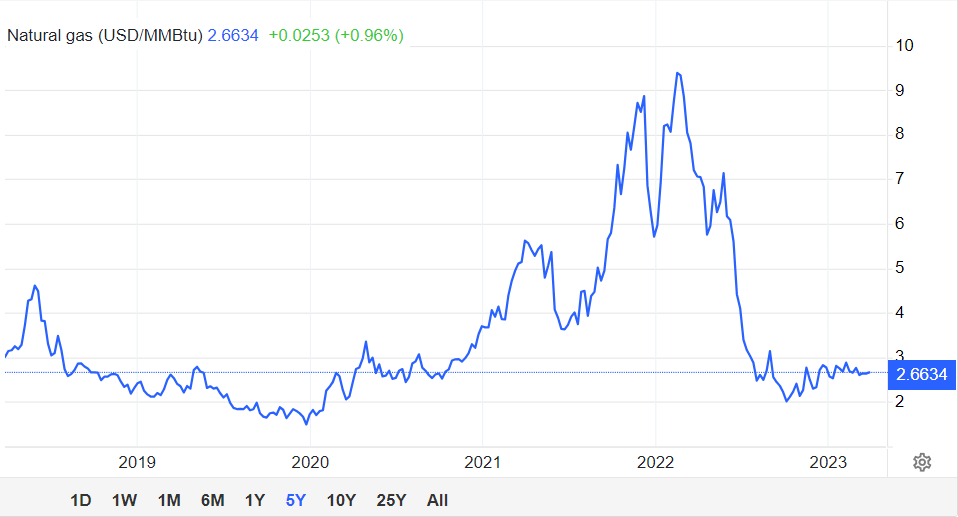

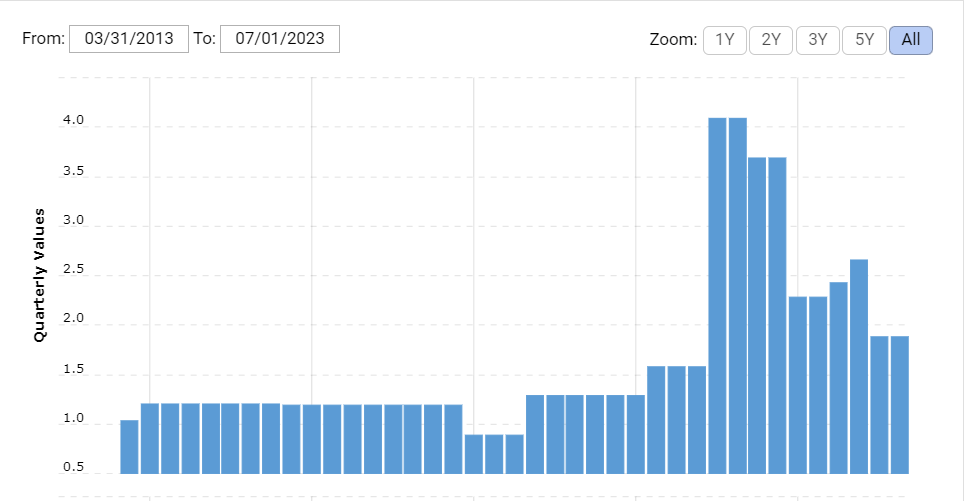

Natural Gas Price (Trading Economics)

Commodity prices such as natural gas are heavily inclined to some sort of volatility and I think the last 12 months have showcased that. What I find very reassuring about the chart above is the stable prices that have occurred in the last couple of months. Given that a large part of the operations with OGS circles around consistent and stable cash flows, that becomes ever so more predictable when prices are like this. The company has grown into a strong dividend-distributing company that can deliver significant shareholder value through the commodity cycles.

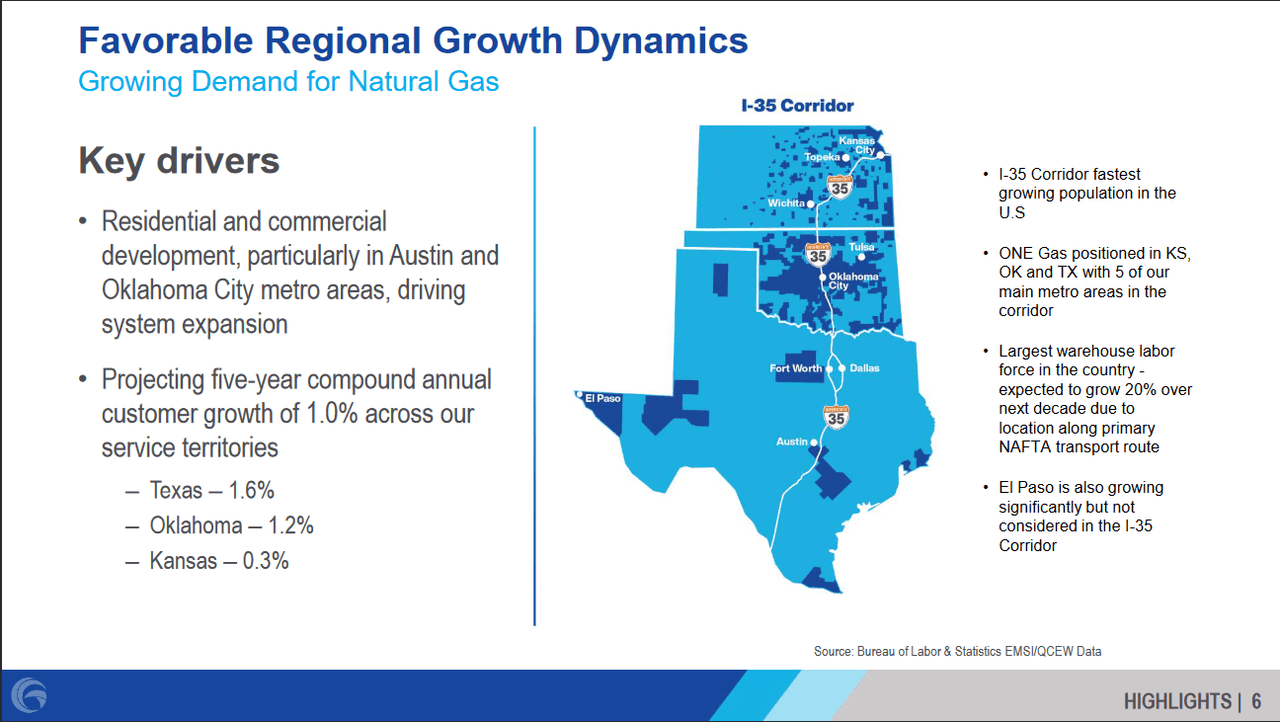

Markets They Are In

Company Overview (Investor Presentation)

The company is in a very favorable place right now as the houses being built in the regions that the company operates in are increasing. More and more commercial and residential buildings are started in Austin which is increasing the TAM that the company has. I think this will be a key driver of growth given the fact that OGS mostly serves those types of clients. A steady CAGR of 1% customer growth over the next 5 years is stable and should provide stronger earnings and FCF for the business.

Market Overview (Investor Presentation)

OGS boasts an expansive geographic service area, encompassing a vast rural expanse. Despite this vast coverage, its customer base numbers are approximately 2.3 million. While this count might not rival that of utilities serving densely populated cities, it still positions OGS as one of the country’s most prominent pure-play natural gas utilities, emphasizing its significance within the industry. The benefit of having a customer base like this is that it’s largely reliable over the long term. There isn’t perhaps a significant amount of build out or new construction projects like in major cities. This should hopefully yield some more reliable earnings for the company in my opinion.

Earnings Highlights

Income Statement (Earnings Report)

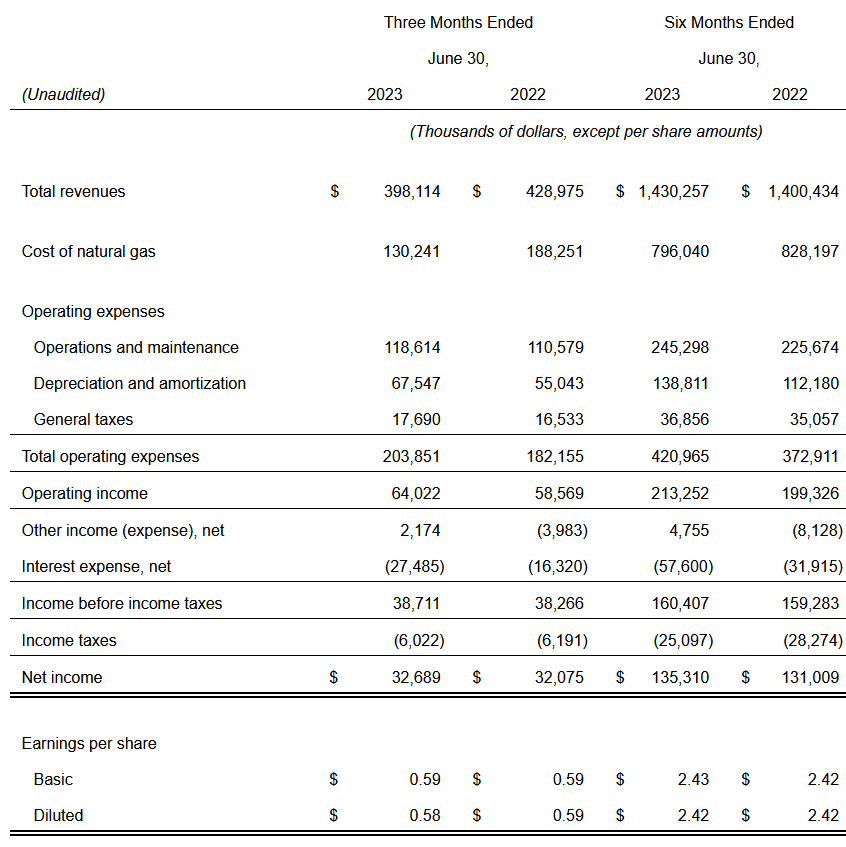

From the last earnings report, I think it becomes quite clear the OGS has been negatively impacted by the declining natural gas prices over the last 12 months. However, the bottom line remains very robust, and I think there is good reason to think that the dividend can be sustained even in these times. The TTM dividend paid out is $139 million, and with hopefully improving gas prices that can be sustained by the bottom line.

The growth of the company has been rather solid over the last several years. The revenues have grown by 5.4% annually in the last decade which I find very solid and underscores some qualities of the business throughout a longer period. As for the EPS, it has grown by 6.94% annually during the same period. Given that OGS is trading at a premium to the sector, I do find it the historical growth is not supportive of this. For OGS to reasonably trade at a premium I would be looking at a CAGR EPS growth of nearly double digits at least, and that it would continue that way as well. Paying a premium for a company growing in line with the market doesn’t seem like value to me, and reasons why I think a hold is the best course of action right now.

Valuation

p/e (Seeking Alpha)

As for OGS, I don’t think it displays the discount that I am looking for. When investing I seek a decent discount rate at least of around 10 – 15%, quite often based on earnings as that is a good indicator of the earnings potential for shareholders. It’s my margin of safety essentially. With a lower p/e than the sector I also get the bonus of a higher dividend yield, if the company is not lowering it of course, which I don’t think is the case with OGS. With this in mind, I think that my preferred price for OGS is around $57 per share, leaving a decent double-digit discount on the p/e metric to the sector.

Risks

Aside from the concern of interest-rate risk, a corporation must fulfill its regular debt payments to maintain its financial stability. Any adverse event that leads to a reduction in a company’s cash flow could potentially push it into financial distress, particularly if it carries a substantial amount of debt on its books. This risk highlights the importance of managing debt levels and ensuring a healthy cash flow to meet financial obligations effectively.

Debt Levels (Macrotrends)

When we look at how the company is leveraged though I think we are heading in the wrong direction right now. Given the rise in the debt levels, it has increased the net debt/EBITDA ratio to over 3. This is a number that I hold quite vital in terms of leverage. With almost any company I prefer a ratio below 3 at least to give me some margin of safety, the lower all the better. I think that given the leverage ratio the company has and the high valuation it is also trading at it’s a rather risky investment right now. Benefiting from the dividend is something that still makes sense in my opinion though, which translates to the hold thesis. Going forward though, watching the leverage of the business I think is incredibly important. Too much and too much of an earning premium could drastically increase the downside risk right now.

Final Words

For investors who are seeking to get more or start having exposure to the natural gas industry, I think there are frankly better options out there than OGS right now. The company has made a lot of contributions to growing the returns of shareholders through the dividends they have. However, the high amount of debt may one day lead to the dividend needing to remain flat to service those liabilities. Besides that, the earnings multiple exhibits a premium of nearly 10%. With depressed natural gas prices, I think that perhaps OGS will face difficulties in the coming years to raise the bottom line if the margins can’t rapidly expand. This leads me to have a more neutral stance on the business and rate it a hold.

Read the full article here