Written by Nick Ackerman.

For some background on this monthly publication, here is my view on dividend growth stocks:

Dividend growth stocks aren’t always the most exciting investments out there. They often aren’t grabbing the headlines, and they aren’t the stocks running up hundreds of percentages in a year. In fact, they are often some of the least exciting stocks. And that is precisely their strongest selling point. With such a vast world of dividend growth stocks available out there, it is important to screen through to see if there are any worthwhile investments to explore.

They are stocks that provide growing wealth over time to income investors. Dividend growers are often larger (not always), more financially stable companies that can pay out reliable cash flows to investors. Some are slower growers than others. Some are going to be cyclical that require a strong economy. Some are going to be secular, which doesn’t generally rely on a more robust economy.

Dividend growth can promote share price appreciation. Of course, that is if these companies are growing their earnings to support such dividend growth in the first place. Trust me. There are yield traps out there – I’ve owned a few that I’m not particularly proud of.

I like to think of investing in dividend stocks as a perpetual loan of sorts. Essentially, every dividend is a repayment of your original capital. Eventually, holding long enough, you have the position “paid off.” It is all returned back into your pocket from that point forward.

All of this being said, it is important to understand my approach to dividend stocks and why screening dividend stocks can be important for income investors. As with any initial screening, this is just an initial dive – more due diligence would be necessary before pulling the trigger.

The Parameters For Screening

I’ll be using some handy features that Seeking Alpha provides right here on their website for this screen. In particular, I will be screening utilizing their quant grades in dividend safety, dividend growth and dividend consistency.

Dividend Safety is relatively self-explanatory. These will be stocks that SA’s quant shows to have reasonable safety compared to the rest of their various sectors. The grade considers many different factors, but earnings payout ratios, debt and free cash flow are among these. This category will be stocks with A+ to B- ratings.

For the dividend growth category, we have factors such as the CAGR of various periods relative to other stocks in the same sector. Additionally, the quant also looks at earnings, revenue and EBITDA growth. As we will see, this doesn’t mean that every stock with a higher grade has the growth we are looking for. This just factors in that the dividend has grown or earnings are growing to support dividend growth possibly. For these, the grades will also be A+ through B- grades.

Finally, for dividend consistency, we want stocks that will be paying reliable dividends to us for a very long time. In particular, hopefully, they are raising yearly, though that isn’t an explicit requirement. We will also include stocks with a general uptrend in dividend payments, which means there could have been periods where they paused increases for a year or two.

After looking at those factors alone, we are left with 535 stocks at this time from the 522 listed last month. I’ll link the screen here, though it is a dynamic list that constantly updates regularly. When viewing this article, there could be more or less when going to the link.

From there, I wanted to narrow down the list a lot more. I then sorted the list by forward dividend yield, from highest to lowest. Since these will be safer dividend stocks in the first place, screening for those among the higher payers shouldn’t hurt.

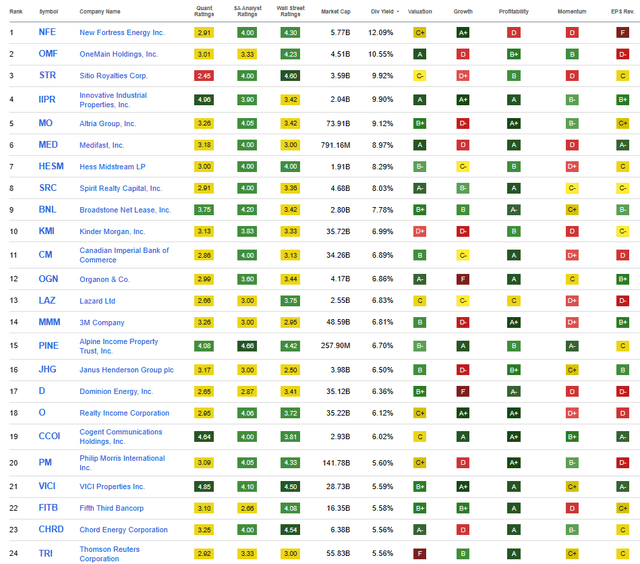

I will share the top 24 that showed up as of 10/05/2023.

Top 24 (Seeking Alpha)

This month, we’ll be giving some quick updates on OneMain Holdings (OMF), Innovative Industrial Properties (IIPR), Hess Midstream (HESM), Broadstone Net Lease (BNL) and Alpine Income Property Trust (PINE). These are all names that we have seen show up on this list previously.

Several names rank higher currently on this list, but we have covered them recently, or they aren’t actually showing a trend of consistently growing dividends despite showing up in the screening and despite the dividend growth criteria.

A big drop across equities this month helped drive the lowest yielder we’ll be discussing today, up to 6.70%. Last month, the number five name we discussed was at a 5.31% yield. This is a dynamic list, and we make sure not to cover the same names too frequently, so that plays a role in the names we touch on. However, this is also reflecting how far equities fell last month. In particular, REITs were hit, and we are touching on three of those today alone.

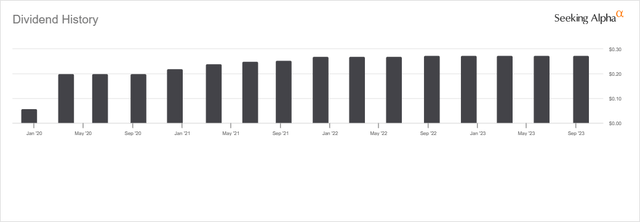

OneMain Holdings 10.82% Yield

OMF has consistently made this list for the past year now, with the last time we touched on the name being in our June 2023 piece.

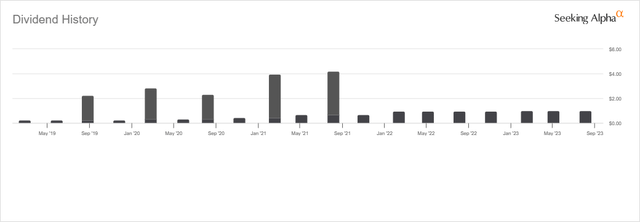

OMF is one that has always caught my attention as being an interesting, high-yield name to consider. They are pushing a double-digit yield and have consistently grown its dividend for several years – though they don’t have too long of a dividend history. They also were able to pay out significant special dividends when times were booming in 2020 and 2021. Despite business slowing down, they still managed to raise their dividend heading into this year.

OMF Dividend History (Seeking Alpha)

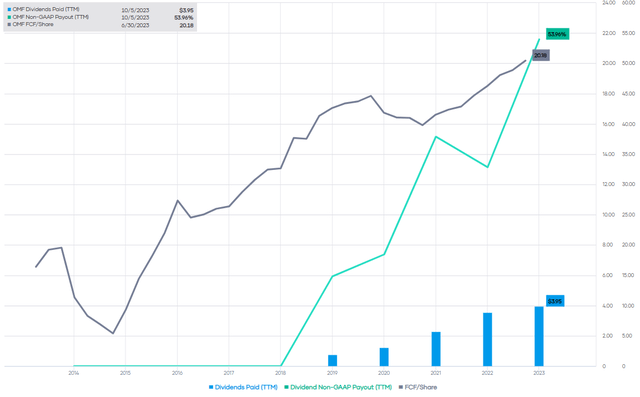

The company has a solid earnings payout ratio and pumps out tons of free cash flow.

OMF Dividend Coverage and FCF/Share (Portfolio Insight)

That being said, one of the major drawbacks or risks here that have continued to keep me out is their business is largely sub-prime lending. There is definitely a need for their business, and that drives profits clearly. However, the downside is that it can make them much more sensitive to economic conditions. With the Fed increasing interest rates, the likelihood of a recession grows as each Fed rate hiking cycle is usually ended due to a recession.

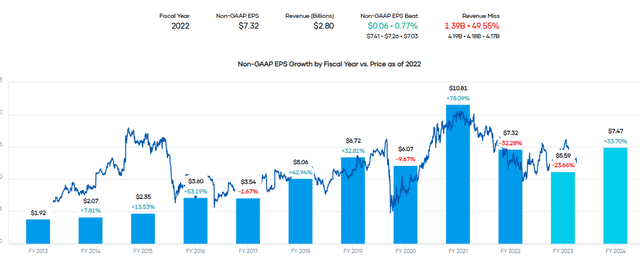

With earnings expected to drop through this year, some of this is being reflected in the weaker economic outlook expected. Shares are trading at a forward P/E of just 6.7x; it is certainly cheap. However, the expected recovery in earnings into 2024 is suspect, in my opinion. Therefore, I believe it could get cheaper going forward and could be worth picking up when we are in a full recession panic drop when volatility spikes.

OMF Earnings History and Projections (Portfolio Insight)

Innovative Industrial Properties 9.99% Yield

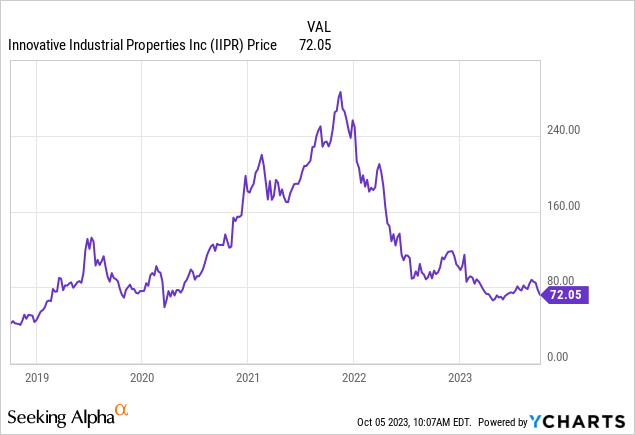

IIPR has been another regular on this list, with the last time we touched on it being in July 2023. This REIT is one that I own in my portfolio as a speculative position. It had gone from being one of my best-performing picks ever to being only mediocre. This was the case as the share price soared and then came back down dramatically due to tightening financial conditions.

YCharts

Not only are interest rates impacting the REIT itself by requiring a higher dividend yield to compensate for the greater risks as an income-oriented investment, but tighter financial conditions mean their tenants are also in a much tougher environment. Through 2020 and 2021, funding for Cannabis companies was plentiful and easy to come by. Now, with tighter conditions in the market, we are seeing cracks and that could impact rent payments to IIPR; thus, why we have seen such a dramatic fall in the share price happen in a short time span.

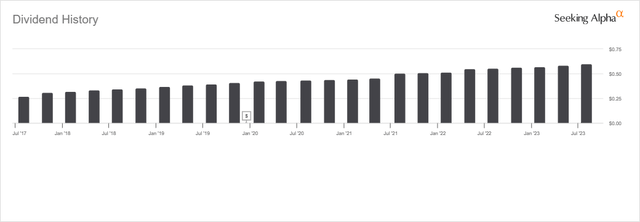

I’m still willing to ride out this speculative industrial REIT play as the dividend remains generous. They recently declared another $1.80 quarterly payment, and that’s now five quarters in a row at the same rate. Of course, given the pressures in the industry currently, I didn’t anticipate an increase – nor do I anticipate one coming in the short term either.

That said, based on forward estimates of FFO, the payout ratio remains covered at around 88%. It’s not the most comforting coverage level, but it is being covered, and that’s another reason why it’s a speculative position all around.

More conservative investors might be interested in the 9% Cumulative Preferred Series A (IIPR.PR.A). It’s currently trading slightly above par but remains at an attractive yield of 8.84%.

Hess Midstream LP 8.60% Yield

HESM is a name we last had an update on in May 2023. As we noted previously, they issue 1099 for tax purposes as that is important for some investors:

An important distinction is that HESM is a midstream C-Corp for tax purposes, which means a 1099 and no K-1. Some investors find the additional paperwork of a K-1 off-putting. Although, I think investors should make investment decisions on fundamentals and not because of a tax form. Still, that should open up HESM to a wider investor audience.

Since that time, the company has been fairly steady in terms of share price, and even the yield has been fairly stable, too. HESM has been raising its distribution every quarter, so the dividend saw a 2.73% increase since our last update. Though, this is also one of those companies that doesn’t necessarily have the longest history behind them.

HESM Dividend History (Seeking Alpha)

Overall, they are targeting distribution growth of 5% annually through 2025. Along with this target, they are stating that they expect to see the distribution coverage at 1.4x, which is right where coverage was as of their last earnings report. That leaves their balance sheet with some flexibility with cash to be able to use for growth.

For an investor looking for some midstream exposure, HESM remains an interesting name to consider. The high yield and reasonable forward EV/EBITDA of 5x make it a reasonable choice.

Broadstone Net Lease 7.85% Yield

BNL isn’t a name that always pops up on this list. In fact, this is the second time, with January 2023 being the first. On a YTD basis, the shares have fallen nearly 12%. However, a lot of that was in the last month or so alone.

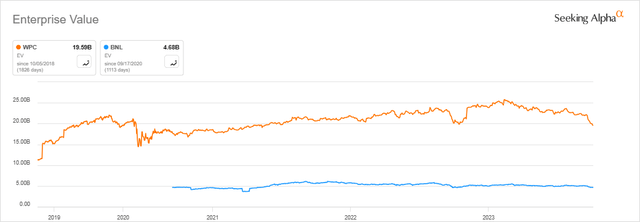

BNL is another REIT that has faced significant pressure due to rising interest rates, and that has pushed its price down significantly. I also believe that W. P. Carey (WPC), its larger diversified REIT peer, also put pressure on the space when it announced a shift in their dividend policy to ‘”reset” it lower last month. WPC is over four times larger than BNL in terms of enterprise value.

BNL EV (Seeking Alpha)

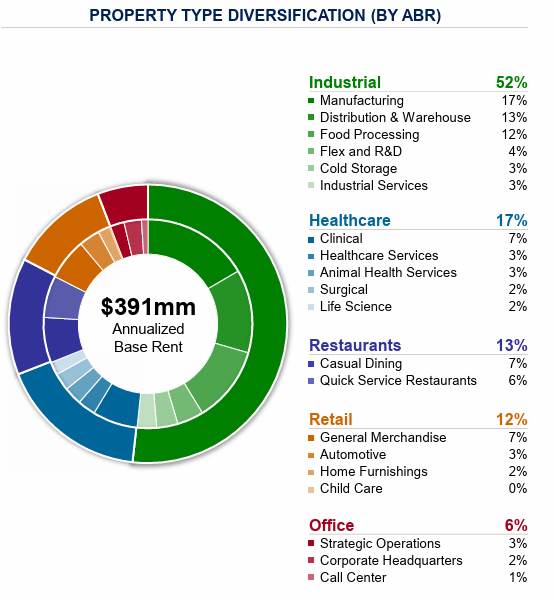

BNL owns 801 properties across 44 states. Additionally, some of those properties are also in four Canadian provinces as well. Some of their properties are office-related, but it is the minority sleeve of their operations. The largest being dedicated to industrial puts them in a good spot exposure-wise.

BNL Property Types (Broadstone Net Lease)

Again, BNL is another name this month that doesn’t have a long history. In fact, it is even shorter than the other three names that we have touched on above. Still, they have been increasing the dividend fairly regularly despite the significant pressures the space is currently facing.

BNL Dividend History (Seeking Alpha)

Based on the expected FFO going forward, BNL’s dividend coverage comes to around 72%. That is actually closer to what WPC is now targeting going forward after their office spin-off. I guess that puts BNL one step ahead of its significantly larger peer. For now, WPC’s dividend yield is higher than BNL’s, but once the cut is in place, it could come in quite similarly.

Additionally, BNL is trading slightly cheaper than WPC on a P/FFO basis at around 9.22x compared to WPC’s 10.04x. Both were hammered, but BNL continues to remain an interesting name to consider for investors looking for diversified REIT exposure. They might not have the same track record as WPC in terms of operations, but if we are looking at a track record of dividends, WPC is basically resetting itself on that front to the same level as BNL.

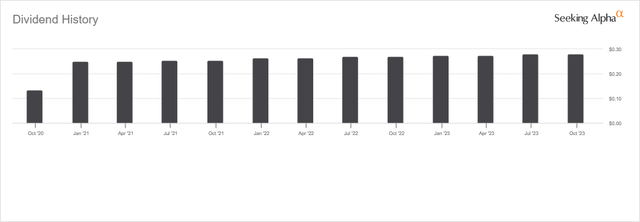

Alpine Income Property Trust 6.70% Yield

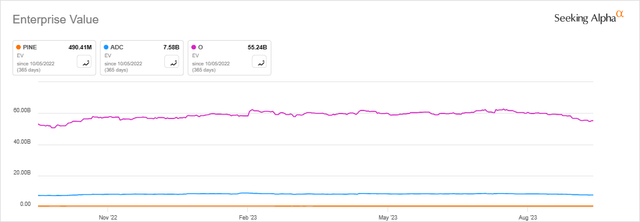

Speaking of interesting REIT names that are getting crushed but are looking attractive, we see PINE show up on this list once again. Another regular name that we touched on just in our June 2023 piece. If we are looking at peers, as a retail REIT, Agree Realty (ADC) and Realty Income (O) would quickly come to mind. Both ADC and O are significantly larger than PINE, as PINE is a small-cap REIT. They hold a portfolio of 143 properties located in only 34 states.

PINE EV (Seeking Alpha)

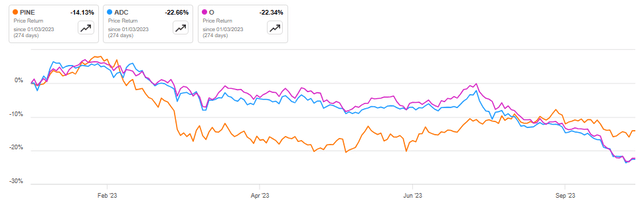

In terms of damage this year, PINE has actually seen itself fall less than these larger peers. Though their losses came earlier this year, ADC and O felt more damage recently to outpace it to the downside. PINE, with its forward P/FFO of 10.83x compared to ADC’s 13.84x and O’s 12.04x, is likely helping support the current price, relatively speaking.

PINE YTD Price Performance (Seeking Alpha)

PINE is externally managed, but that isn’t necessarily all bad news in this case. CTO Realty Growth (CTO) is their manager. The manager carries a 7.8% ownership interest, which should keep them pretty well aligned with other shareholders. They are also looking to internalize the management once it reaches “critical mass.” I’m not sure exactly what that level is, but it’s something that is in the blueprint going forward.

They’ve been able to grow their dividend, with it trending higher since launch. However, they have held the dividend flat now for five quarters in a row. That being said, dividend coverage based on forward FFO estimates remains fairly solid at a payout ratio of only ~72%.

PINE Dividend History (Seeking Alpha)

Despite PINE being the cheapest compared to peers ADC and O, ADC and O are also attractive and have a solid track record with internal management. That likely warrants the premium pricing. As they’ve both also collapsed, PINE, while being quite interesting, doesn’t quite interest me enough.

Read the full article here