Investment Thesis:

The market is underestimating the exciting prospects of NICE’s cloud business. This business has a strong balance sheet position, a long history of serving the market and is positioned to benefit from the AI wave. At 11x EV / 2027 Adj. EBIT projections, I believe this investment offers a good risk/reward profile.

The Business Model

NICE Ltd (NASDAQ: NICE) is one of the leading providers of enterprise software solutions enabling organizations to manage and improve customer experience, ensure compliance, battle financial crime, and safeguard people and assets. Under its current structure, the company has three reportable segments and three business units. The reportable segments are Cloud, Product and Services, while the business units are Customer Engagement, Financial Crime & Compliance, and Public Safety & Justice.

The most innovative cloud solutions segment includes revenue from cloud-based solutions such as CXone (customer experience platform), X-Sight (a cloud platform for financial crime detection and compliance) and Evidencentral (a cloud-based public safety & justice platform). This is the fastest-growing segment and the one this article will focus on. According to the company’s disclosures, it serves 10/10 top U.S healthcare Insurers, 5/5 Top U.S Telcos, 9/10 Top Global Financial Services firms and 6/10 Top Fortune 10 companies. The industry-leading CXone platform is a Contact Centre as a Service (CCaaS) in a cloud and scalable format.

The second segment, named product, consists predominantly of professional services and consulting fees related to implementing and optimizing NICE’s solutions.

The third and final segment is product revenue, which consists of on-premise software licenses (old school) and hardware sales.

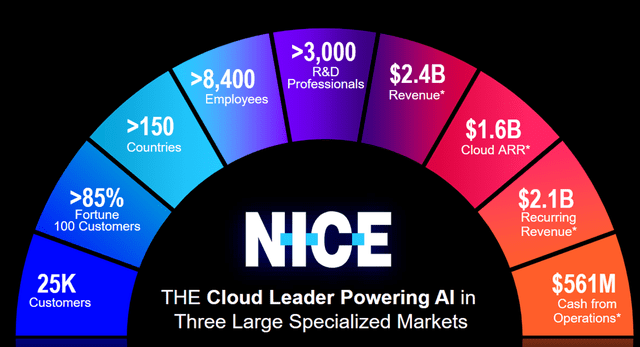

NICE Ltd Investor Presentation

The Growth Supercharger

The first and most apparent commercial use-case of Large Language Models (LLMs) and Generative Artificial Intelligence is the streamlining and effective resolution of customer service interactions. Particularly the low-hanging fruit of simple customer questions that eat up the time of humans that are capable of resolving the tougher requests. Evidence of productivity improvements are rare to find, but Klarna’s ground-breaking announcement has set the bar high. Recently, Klarna announced that it handled 2/3rds (roughly 2.3 million) of customer service chats within the first month of operation. It’s estimated that it has done work equivalent to 700 full-time customer service agents and reduced the resolution time from 11 to less than 2 minutes. If that was not enough, it also achieved satisfaction rates on par with human agents and reduced repeat queries by 25%. According to its mother company, this customer service efficiency is expected to drive a $40 million profit improvement for Klarna in 2024.

Klarna’s data has shocked the enterprise world, and many organisations are scrambling to plan for Customer Service automation. NICE will benefit from this wave as it offers a comprehensive suite of solutions that help organisations deliver customer services across multiple channels. The CXone platform helps customers with seven capabilities:

- Omnichannel routing: Customer interactions are directed to the most appropriate and capable agent, depending on the demanded request.

- Self-service: Virtual assistants powered by AI. These are tailored by customers to fit the purpose.

- Workforce Engagement: Forecasting and scheduling for contact centre workforce optimisation and utilisation.

- Analytics & Reporting: Insights into customer interactions, agent performance and KPIs for improved decision-making.

- AI & Automation: Real-time suggestions to agents during interactions.

- Integration APIs: CRM, ESP and third-party data sharing.

- Compliance & Security: Adhering to regulatory standards such as PCI-DSS, GDPR and HIPAA for customer data protection etc.

In the most recent Q4 2023 results, NICE reported 20% YoY cloud revenue growth and a whopping 300% growth in the number of AI deals in 2023. The gross margin for Cloud revenue is about 66% (71% non-GAAP), showing software-like characteristics but with further upside to follow. Management is guiding for 15% revenue growth and 19% Adj. EPS growth midpoint for the full year 2024. The guidance assumes a conservative deceleration of cloud growth to 18% for the full year, excluding the LiveVox acquisition. Management is likely downplaying Cloud’s growth potential for 2024 as the segment has grown 30%, 31%, 27% and 22% for 2020, 2021, 2022, and 2023 respectively. If something, this segment is gaining steam with all the inbound interest relating to AI.

The company’s documents stated that management expects the Cloud TAM to grow at an annualised rate of 18% from about $8 Billion in 2023 to $22 Billion in 2028. Currently, only 5% of interactions contain conversational AI, and only 20% of the business has migrated to CCaaS. A Gartner study forecasts that by 2025, 80% of customer service organisations will be applying generative AI technology in some way to amplify agent productivity.

NICE has the upper hand in CCaaS

Assuming that the market grows at an annualized rate of 18%, I think NICE’s cloud division will grow faster than the market, aided by its competitive advantages from operating in the customer experience industry for over 35 years. The CXone platform has been crowned the industry leader for CCaaS by Forrester Research, Ventana Research, Opus Research and the Garner Magic Quadrant. The company has a data advantage over its competitors as it has long-term records built over many years of resolving customer queries. 85 of the Fortune 500 companies transact with NICE Ltd, and management invests 12-14% of revenues in R&D to innovate its current product offerings.

NICE has developed longstanding customer partnerships and solved the reliability puzzle for data, security, and case resolution. Leading IT services players such as Cognizant, Infosys and Microsoft have partnered with NICE to offer frontier CCaaS solutions to their customers. Large organisations favour partnering with large vendors like NICE instead of trusting small vendors to handle their interactions with valued customers. An example of what can go wrong in the automated handling of customer queries is the Air Canada case, where the passenger was promised a non-existent discount. This case falls under AI hallucination, where AI chatbots can provide inaccurate information.

Valuation:

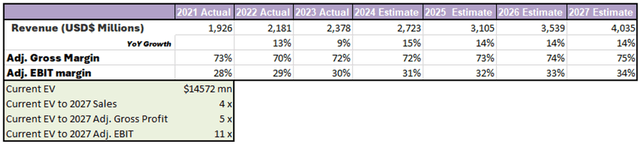

Author’s projections

Based on the reasoning I remarked earlier, I assume the cloud revenues will continue outgrowing the Services and Product revenues. This will drive the company’s annualized revenue growth closer to 14-15% until 2027. As the Cloud business expands, the company’s fundamental profile will steadily morph into software-like businesses with high gross margins and improving operating leverage, subsequently pushing margins higher. These assumptions yield an attractive valuation of 11x my 2027 Adj. EBIT projections.

Risks:

Artificial Intelligence is an expensive pursuit, and projects relating to its applications are somewhat discretionary in the current environment. This exposes NICE to economic slowdowns that may delay discretionary spending. On the other hand, Klarna demonstrated that the cost savings from applying AI can be significant.

CCaaS is an attractive and lucrative industry that may attract new competitors. For example, recently, RingCentral announced a new CCaaS offering that will compete against NICE. It is essential to monitor the competitive landscape as the technology is being deployed at large.

Conclusion:

NICE’s 35-year history in the customer experience industry put it in pole position to leverage the data advantage it has cultivated in enduring relationships with its customers. The growing wave of AI and Generative AI will play a catalytically important role in supercharging growth for the Cloud segment. The 11x EV to my 2027 Adj. EBIT projection is a good multiple for a business with an excellent competitive position, net cash balance sheet, and benefits from AI.

Read the full article here