Investment thesis

NewLake Capital Partners (OTCQX:NLCP) is a high-risk – high-reward investment case that I consider a candidate just for a small portion of my portfolio. NLCP:

- has a high (100%) occupancy rate and solid WALT (14.1 years)

- has healthy liquidity supported by cash position and undrawn credit facility with negligible debt outstanding

- operates within a unique property sector with attractive growth prospects and highly favourable supply-to-demand relationship

However, the Company still falls on the risky side of entities covered within the Cash Flow Venue due to the cannabis sector’s specificity, dependence on the regulatory environment, and high tenant concentration.

Nevertheless, I believe that NLCP offers the potential for double-digit total returns resulting from:

- high dividend yield

- multiple appreciation

- further investment activity and contractual rent escalations

Introduction

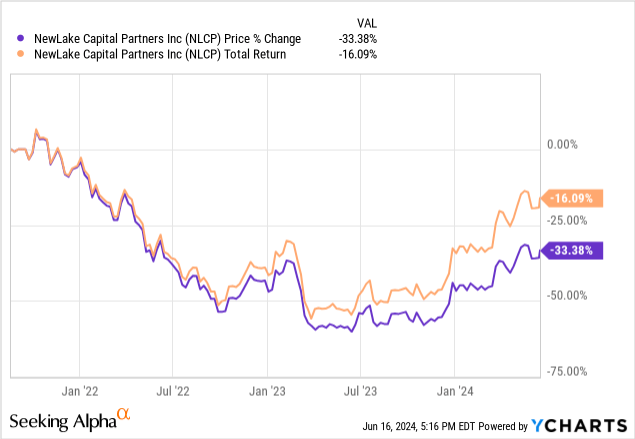

NLCP is a triple net lease REIT that concentrates on properties leased to US-licensed cannabis operators (including cultivation facilities and dispensaries). The Company was founded in 2019 and had its IPO in 2021. It currently holds 31 properties across 12 states (1.6m sq. ft.). Since its IPO, NLCP brought negative price-oriented and total returns equal to -33.4% and -16.1%, respectively. To provide some colour on this, apart from the general weakness of the REIT sector during the period, the weakness of NLCP’s stock has been magnified due to some tenant-related issues and difficulties within the cannabis industry.

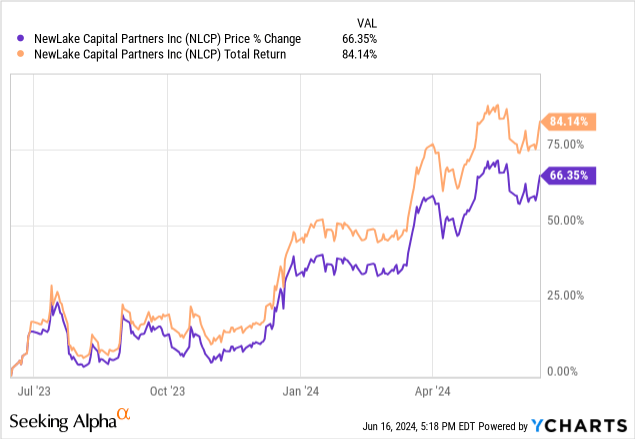

However, NLCP has been impressively rewarding for investors who allocated their capital around a year ago as the Company solved its tenant issues and the cannabis sector is undergoing some supportive regulatory changes.

Such a dynamic stock price increase on a year-over-year basis may lead investors to believe that the business is overvalued. However, I don’t think so – let me present my rationale for that. Enjoy the read!

Why NLCP is still a buy?

#1 Unique property sector with underlying growth prospects

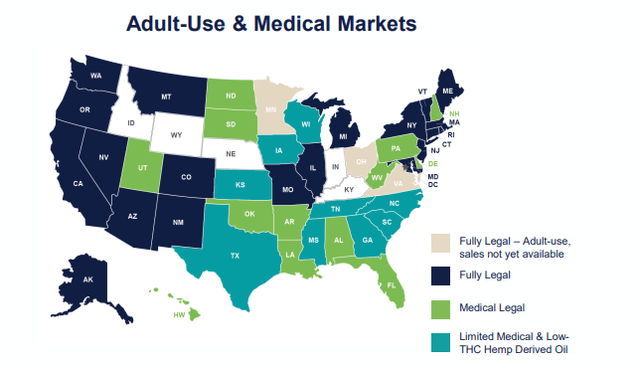

The scope of legalization of cannabis usage continues to increase across the US, with ~90% and ~52% of the US population residing in the medical-use and adult-use markets, respectively. While the cannabis sector had its struggles in recent years, consumer demand continued to grow – the cannabis sales dynamic accelerated entering 2024. There’s still a lot of room for legalization and thus – further growth of the industry that could include:

- expansion programs of limited medical-use markets

- transition to the adult usage of the leading medical-use markets

- enabling sales with the adult-use markets with no sales available, which include Ohio, Minnesota, and Virginia

- further growth supported by the favourable supply-to-demand relationship within adult-use markets

The changes are progressing, as the Company’s Chairman – Gordon DuGan mentioned during the Q1 2024 Earnings Call:

Recent news regarding the DEA’s forthcoming proposed rule to reschedule cannabis from Schedule I to Schedule III has created significant buzz around the industry and on Capitol Hill. While there is still a lot of work to be done by the DEA before their proposed rule becomes final, it is a very significant milestone for the cannabis industry and those serving it such as NewLake.

Such regulatory changes naturally have a direct translation into the financial and credit stance of the cannabis industry players and, thus, the real estate providers such as NLCP. As NLCP’s CEO – Anthony Coniglio mentioned in reference to the proposed reschedule:

This proposed rescheduling is a significant milestone for cannabis reform and removing the onerous Section 280E taxation would provide meaningful tailwind to the cannabis sector. A final rescheduling to Schedule III would instantly improve the credit quality and cash flow position for our entire tenant portfolio by reducing the taxes they pay.

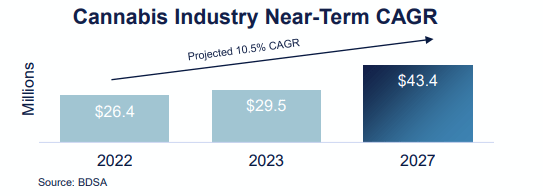

All these catalysts support further market growth. According to the data presented in NLCP’s Investor Presentation, the cannabis industry will mark an impressive 10.5% CAGR during the 2023 – 2027 period (with 2022 as a base year). The data is a little bit outdated; however, the study gathered by Statista (published by Marijuana Business Daily) assumes that the sales of legal recreational cannabis will mark a similarly impressive CAGR of 11.1% during the 2024 – 2028 period.

NLCP’s Investor Presentation

NLCP’s Investor Presentation

To summarize, NLCP’s property sector is accompanied by a highly favourable supply-to-demand relationship with still undersupplied leading markets and ever-increasing consumer demand, and thus, cannabis operators’ demand for real estate. There’s still plenty of room for further growth that could be a result of several catalysts.

#2 Great business metrics and strong leases

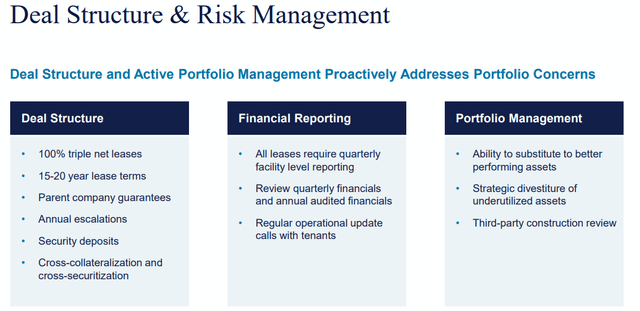

In order to properly interpret NLCP’s business metrics, let’s compare them to its noticeably larger competitor – Innovative Industrial Properties (IIPR). As of March 2024, NLCP owned 31 properties with a total of 1.6m sq. ft., while IIPR owned 108 properties with ~8.9m rentable sq. ft. Both entities are generally 100% triple net lease REITs, which is the most favourable type of agreement from the landlord’s perspective. For instance, it involves the tenant covering a substantial number of costs related to operating and maintaining the property (maintenance costs, taxes, insurance, operating costs, repairs, etc.). Moreover, these agreements are usually subject to contractual rent escalators typically ranging from 1% to 2%, however, NLCP is capable of securing more attractive conditions with 2.6% annual rent increases. It’s a solid level, especially attractive under the triple-net lease structure, as these single-digit escalators tend to add up over time and heavily impact the bottom line.

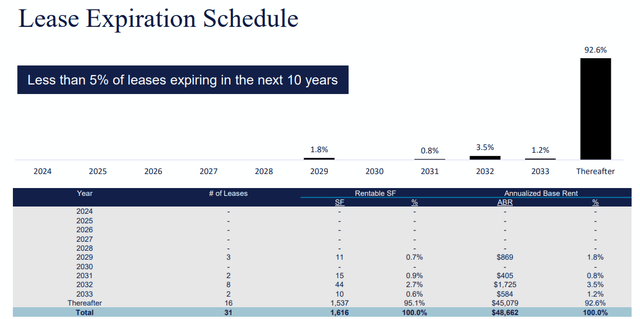

Occupancy rate and weighted average lease term (WALT) are important metrics that reflect the overall quality of the portfolio. Investors may be misled when it comes to the occupancy rate if they focus too much on the historical median occupancy rate for an S&P 500 REIT, equal to 94.8% – according to Realty Income (O). There are, however, many REITs that are capable of upholding occupancy rates at a much higher level, and NLCP is one of them. According to its Investor Presentation, as of March 2024, its occupancy rate amounted to 100%, which is as good as it gets. For reference, IIPR’s occupancy rate amounted to 95.2% when considering 103 operating properties out of a total 108 property portfolio. When it comes to WALT NLCP has a solid metric that stood at 14.1 years (for reference, IIPR’s WALT stood at 14.8 years).

NLCP’s Investor Presentation

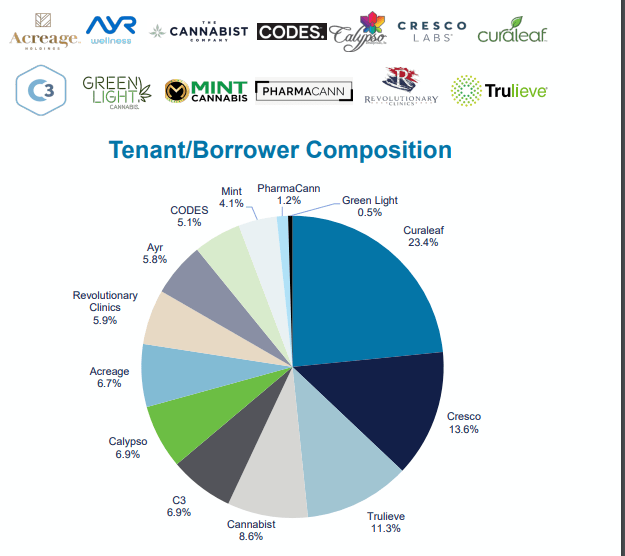

However, there’s a factor that can be considered a weak spot of NLCP’s business, also when compared to IIPR – the tenant concentration. As of March 2024, NLCP’s largest tenant was responsible for 23.4% of ABR, while over 50% of ABR was derived by the Top 4 tenants. IIPR has a better tenant structure, with Top 1 responsible for 16.9% of ABR and Top 4 responsible for 42.1% of ABR. Nevertheless, one should not compare this metric to the tenant concentration of (for example) retail/service-oriented REITs due to the specific nature of the cannabis industry.

NLCP’s Investor Presentation

#3 Financial stance

The high-interest rate environment has a limited impact on NLCP’s financial performance as the Company has negligible debt maturities in the upcoming years, with only $4m debt outstanding as a result of its revolving credit facility. The Company has high liquidity and is well-positioned to pursue upcoming investment opportunities, as its CFO, Lisa Meyer, commented during the Q1 2024 Earnings Call:

As of March 31, 2024, we continue to have a strong balance sheet with $420 million in gross real estate assets and only $4 million of debt outstanding on our $90 million credit facility. We have $107 million of liquidity comprised of cash and the remaining availability under our credit facility and the company is well positioned to execute our business strategy to grow earnings for investors as we deploy this capital.

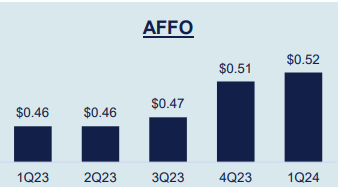

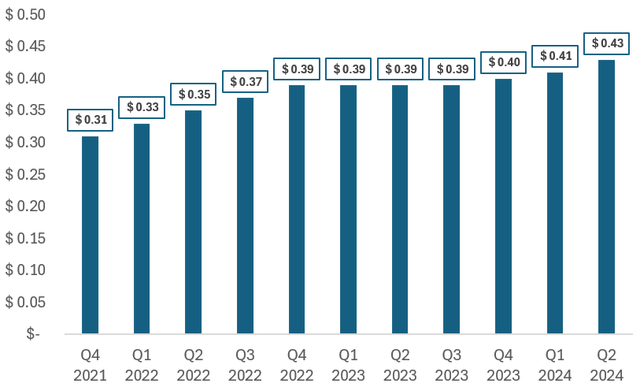

In 2023, the Company generated $1.89 AFFO per share (up 6.8% year-over-year), marking a CAGR of this metric equal to 15.1% during the 2021 – 2023 period. Moreover, during Q1 2024, NLCP generated $0.52 AFFO per share (13% upside compared to Q1 2023 and 2% growth on the Q4 2023 level), as presented within its Investor Presentation. NLCP continues to grow its quarterly dividends and has recently announced a dividend increase to $0.43 per share. The dividend is well-covered with a reasonable forward-looking AFFO payout ratio of ~78.5% and is currently yielding an attractive ~8.2%.

NLCP’s Investor Presentation

Chart 1: NLCP’s dividend per share

Own compilation based on NLCP

#4 Valuation outlook

As an M&A advisor, I usually rely on a multiple valuation method that is a leading tool in transaction processes, as it allows for accessible and market-driven benchmarking.

In its Investor Presentation, NLCP provides optimistic P/AFFO multiple comparisons to IIPR and “non-cannabis REIT peers”. However, the only rationale I can see for comparing NLCP to NNN Reit (NNN), NETSTREIT (NTST), Essential Properties Realty Trust (EPRT), or VICI Properties (VICI) is the triple-net lease structure of their agreements. Considering the specificity of the cannabis industry, I don’t believe that is enough reason to compare NLCP to the above entities. Therefore, let’s concentrate on comparing NLCP to its closest competitor – IIPR:

- NLCP currently trades at a forward-looking P/FFO multiple of ~9.9x

- IIPR currently trades at a forward-looking P/FFO multiple of ~13.0x

Both entities will likely benefit from the underlying value drivers of the cannabis industry and the proceeding regulatory changes. NLCP has solid business metrics with attractive rent escalators, occupancy rate and WALT either better or comparable to IIPR, and essentially no debt outstanding. Some investors may consider the size of IIPR as an advantage, however, it’s a double-edged sword as the smaller size allows the REIT to remain more selective with its capital allocation as each investment moves the needle for the company in a more noticeable manner. The only major weakness business-wise is the tenant concentration described earlier, however, the NLCP proved its capabilities in navigating potential tenant issues (described in its Q4 2023 results release statement).

NLCP’s Investor Presentation

Therefore, I believe that NLCP offers not only potential returns resulting from attractive dividend yield, further investments, and contractual rent escalations but also from potential upside derived from the multiple appreciation. Given the circumstances described above, I believe that NLCP’s repricing to reach an 11.0-12.0x P/FFO range is a highly realistic scenario, given no material adverse changes. Reaching a lower end of the indicated range would already unlock ~10% upside potential resulting from just a P/FFO appreciation.

Risk factors

While the risk of a high-interest rate environment remains limited in the case of NLCP due to negligible debt outstanding, the relatively high cost of capital access limits the company’s ability to pursue larger investment volumes. Nevertheless, NLCP is well-positioned to act on attractive investment opportunities.

NLCP is still exposed to any potential tenant issues, which could have a significantly negative impact on its financial performance due to the high tenant concentration.

Moreover, the Company operates within the specific property sector that is highly dependent on the regulatory environment, which could not only accelerate but also limit NLCP’s growth prospects.

Key takeaways

NLCP is a nice addition to a well-structured portfolio. It has healthy liquidity, attractive dividends, and solid business metrics. The Company operates within a unique property sector with several growth catalysts and a favourable supply-to-demand relationship. It offers a potential for double-digit total returns resulting from:

- high dividend yield

- multiple appreciation

- further investment activity and contractual rent escalations

However, I only regard NLCP as a candidate for a small portion of my portfolio due to the high-risk – high-reward character of the business and some noticeable risk factors that NLCP is accompanied by.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here