Novartis (NYSE:NVS) recently completed the spin-off of Sandoz which transformed the company into a pure-play biopharma company with higher margins and a somewhat improved growth profile. The stock is also down 12% since my previous neutral/hold article and the lower valuation coupled with improved margins and growth prospects put the company in a better position to increase shareholder value. Given the company’s size and growth profile, I do not expect miracles going forward but do believe the stock can compound at least in the high single digits over the medium and long term.

Sandoz spinoff

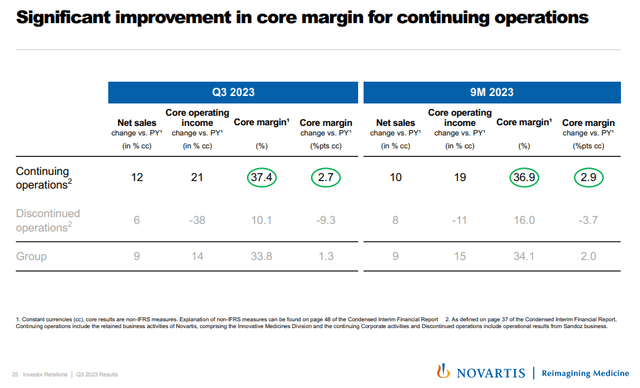

Novartis executed the spin-off of Sandoz in early October. Sandoz was a drag on margins and revenue growth and its spinoff created a “clean” biopharma business for Novartis. You can see from the slide below how all the metrics for the continuing operations look a lot better than the Sandoz unit – higher revenue growth, higher core margin, and improving margins versus worsening margins.

Novartis investor presentation

The spinoff could also lead to somewhat improved sales and earnings multiples in the medium to long term. It could happen in the near term as well, but probably not until we see industry sentiment improve.

Pharma business momentum

The biopharma business is in good shape with several existing high-growth products and several pipeline products and label expansion opportunities for existing products.

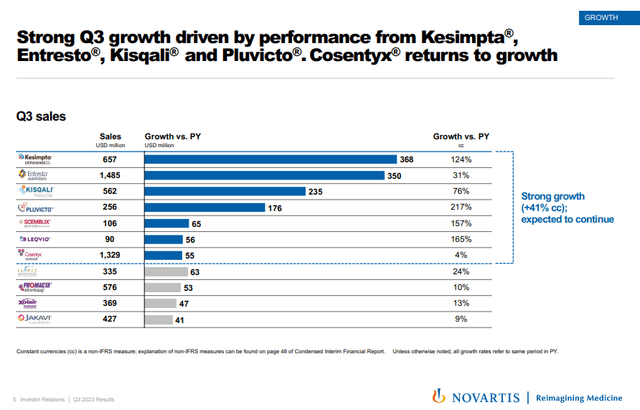

Kesimpta, Entresto, Kisqali, Pluvicto, and Leqvio are among the key approved products that are showing strong growth.

Novartis investor presentation

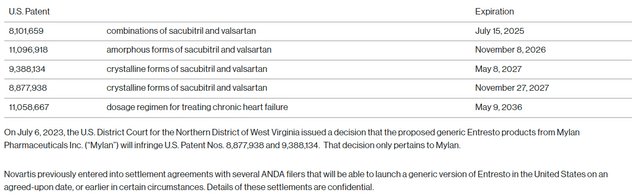

Entresto is the only product with an uncertain future due to the potential generic competition. Novartis has appealed to reverse the negative US District Court decision on the combination patent covering Entresto and other combinations, which expires in July 2025 (including pediatric exclusivity). Entresto is still Novartis’ largest product with global sales likely reaching $6 billion this year, and the patent situation and the associated lawsuits are complex and with an unknown outcome. This is also not the only issued and valid patent on Entresto and others expire between 2026 and 2037.

Novartis press release

Other major products do not have medium-term patent exclusivity issues.

Kesimpta and Kisqali remain the other key growth products and have delivered 124% and 76% Y/Y growth in Q3, respectively and the two products combined now have an annualized net sales run rate of nearly $5 billion.

Pluvicto, Scemblix, and Leqvio have continued to generate triple-digit Y/Y growth in the third quarter, but have a much smaller revenue base than the other three products.

Cosentyx grew only 4% Y/Y in the third quarter but could get a new wind at its back if it is approved for the treatment of hidradenitis suppurativa this quarter. Humira is still the only approved treatment option and while its sales are not broken down by indication, I have seen estimates from various companies developing potential treatments for the condition of Humira doing at least $2 billion and up to $3 billion a year. It was approved in the EU for the treatment of HS in the second quarter and net sales grew 15% Y/Y versus a 3% decline in the United States. The U.S. approval could put Cosentyx back to double-digit growth in 2024 and beyond.

There are other shots on goal for Cosentyx as well as active late-stage trials in giant cell arteritis, polymyalgia rheumatica, and rotator cuff tendinopathy, that could further improve its growth rates in the second half of the decade.

And the future of Novartis’ cardiovascular franchise still looks good. I was impressed by the progress of Leqvio in the last few quarters. Global sales have reached $90 million in Q3 despite the lack of clinical data from a cardiovascular outcomes trial and those are not expected until at least 2026. I now expect Leqvio to become a blockbuster product before the outcomes trial readout and a multi-billion product by the end of the decade, assuming the results from that trial are positive.

One cardiovascular candidate that I believe is underappreciated is pelacarsen, in development for the treatment of patients with elevated lipoprotein A, or LP[a]. I wrote about LP[a] as a drug target in my November 2022 article on Arrowhead Pharmaceuticals (ARWR) and will borrow a few sentences (and should add that Arrowhead has since monetized its royalty stream on olpasiran while retaining the right to receive the remaining milestones from partner Amgen).

Lp[a] is a genetically validated target – a recent analysis from the UK Biobank with a diverse sample of 460,000 individuals showed that the risk of atherosclerotic cardiovascular disease (‘ASCVD’) associated with Lp[a] levels was log-linear for levels above the median, with increasing risk for higher Lp[a] levels. The standardized risk for ASCVD was “11% higher for each increment of 50 nmol/L, independent of adjustment for traditional risk factors, and with similar effect estimates in all race and ethnicity groups.”

While this sounds promising for Lp[a] as a therapeutic target, it is not a certainty that risk reduction will be achieved pharmacologically with drugs like pelacarsen or olpasiran and this is why these companies are conducting large cardiovascular outcomes trials.

Pelacarsen has a considerable head start over olpasiran and results from the cardiovascular outcomes trial are expected in the first half of 2025. If the results are positive, this could be one of the largest breakthroughs for cardiovascular disease drugs since the invention of statins, and I would expect pelacarsen to become a multi-billion product for Novartis by the start of the next decade, if not sooner.

And last, but not least, among the potential growth products is iptacopan, in development for the treatment of paroxysmal nocturnal hemoglobinuria (‘PNH’) and other complement-mediated diseases. I already wrote about iptacopan last year and should add that it met the primary endpoint at the interim analysis in the phase 3 trial in IgA nephropathy patients. Additional readouts in C3 glomerulopathy and aHUS patients are expected this quarter and in 2025, respectively.

Two pipeline candidates that I thought had decent potential and that I mentioned in my previous article are no longer part of Novartis’ pipeline. The company decided to end the collaboration with BeiGene (BGNE) which covered BeiGene’s PD-1 antibody tislelizumab and TIGIT antibody ociperlimab.

There are also other product candidates in the pipeline that I will not go over in this article that are also expected to drive additional growth in the following years, and we should expect the company to continue to add more assets through business development.

Overall, I believe the existing product portfolio and pipeline, along with additional assets that come through business development efforts can deliver at least mid-single-digit revenue growth rates and potentially high single-digit growth rates in the medium and long term. This is not exciting growth, but should be sufficient for Novartis to maintain a double-digit P/E ratio that could reach high double-digit in expansionary periods and I believe Novartis can deliver a long-term share price growth rate of at least 8% and up to 11-12%, but the higher end would need some larger pipeline wins, such as pelacarsen reporting robust treatment effect in patients with elevated LP[a].

Conclusion

The correction in the share price and the successful spin-off of Sandoz have brought Novartis to decently attractive levels. The company has a good collection of approved growth products and a few promising ones in late-stage development, and I would expect to see the portfolio expand through M&A in the following months and years.

Read the full article here