Introduction

It’s time to talk about Nasdaq, Inc. (NASDAQ:NDAQ). On August 31, I wrote an article titled Top-Tier Financial Dividend Growth With Nasdaq, aimed at explaining how Nasdaq is growing beyond traditional stock exchange services, building a financial powerhouse with next-gen capabilities.

The company’s transformation, marked by investments in cloud computing, AI innovation, and strategic acquisitions like Adenza, positions it for significant growth.

Nasdaq’s ability to capitalize on market modernization, ESG trends, and anti-financial crime initiatives enhances its cross-selling potential.

Nasdaq’s lower valuation and optimistic growth projections present an attractive opportunity for long-term investors.

The company just reported its earnings, confirming that its strategy is paying off. The company is seeing growth across the board, with new segments offsetting some weakness in traditional services.

I believe that Nasdaq remains a Buy, as we’re seeing an attractive mix of strong company fundamentals and market headwinds that keep the stock at an attractive value.

So, let’s dive into the details!

Nasdaq Is Growing Fast

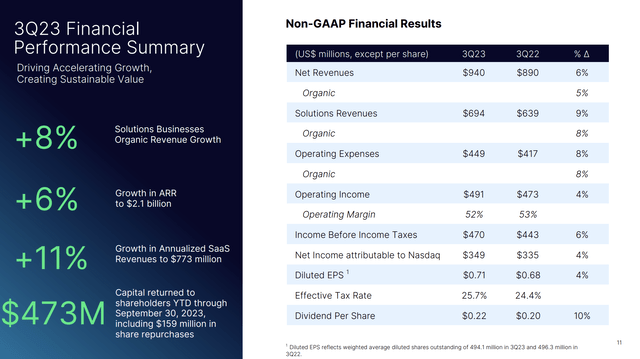

In the third quarter of this year, Nasdaq reported a rock-solid financial performance.

They achieved $940 million in net revenues, a 6% increase compared to the previous year, with a 5% organic growth rate.

Revenues from their Solutions businesses reached $694 million, up 9% YoY and 8% organically. Total ARR (annual recurring revenue) increased by 6% to $2.1 billion, with SaaS revenues now comprising 37% of the total company ARR.

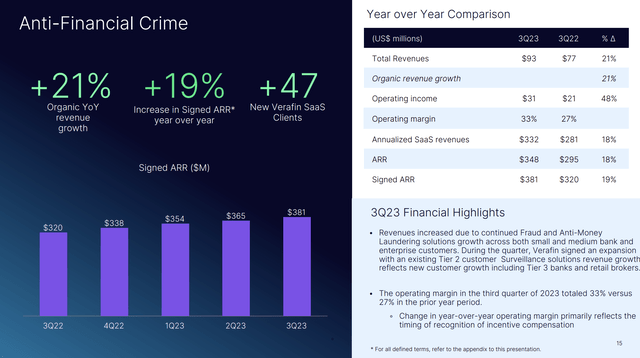

This growth was primarily driven by the continued strength in the Anti-Financial Crime division, reflecting a robust demand for Nasdaq’s services.

Nasdaq Inc.

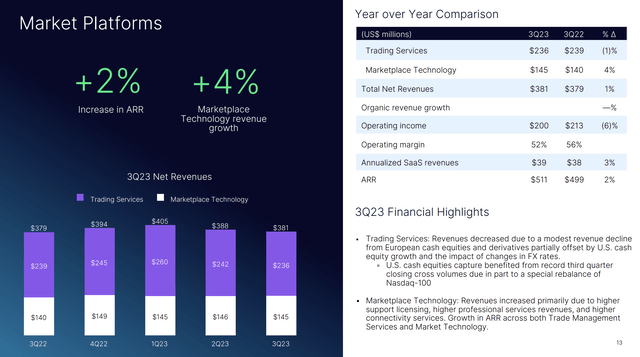

Revenues in the Market Platforms division increased by $2 million, driven by changes in FX rates. Trading Service’s organic revenue was down 2%, largely due to lower European trading revenues, although better cash equity revenue capture offset mostly flat U.S. revenues.

Nasdaq Inc.

Market Technology showed 3% organic revenue growth, though this growth was lower than earlier in the year. ARR totaled $511 million, showing a 2% increase.

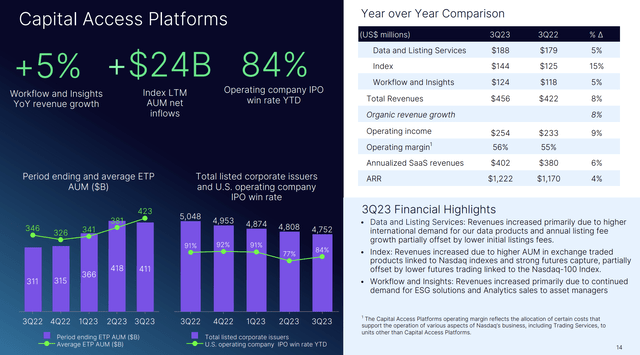

Revenues in the Capital Access Platforms division increased by $34 million or 8%, with strong performance in the Index, driven by a 15% increase in Index revenue.

Nasdaq Inc.

This division saw $24 billion in net inflows over the past 12 months, although AUM was negatively impacted by recent market trends.

In the Data and Listing Services division, revenue grew by 5%, with organic growth at 4%. This was attributed to the strength of the Data business and the impact of de-listings and a subdued IPO environment on Listing revenue growth.

Furthermore, as I already briefly mentioned, Anti-Financial Crime revenue showed an impressive 21% increase compared to the previous year. This growth was driven by strong demand for Fraud Detection and Anti-Money Laundering solutions and SaaS-based Surveillance Solutions.

Nasdaq Inc.

Nasdaq also welcomed 83 new operating company IPOs year-to-date, maintaining a strong win rate, which is somewhat unusual in this market environment.

Shareholder Returns & Growth Progress

Thanks to a strong financial performance and a healthy balance sheet, NDAQ shareholders remain in a great spot.

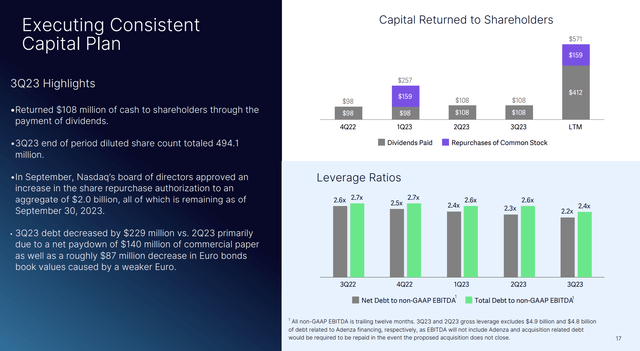

The company’s adjusted total debt to EBITDA ratio dropped to 2.4x. The net leverage ratio (gross debt minus cash) is expected to end this year at 1.6x EBITDA.

The company paid common stock dividends of $108 million during the third quarter and increased its share repurchase authorization to a total of $2 billion. This translates to 8% of its current market cap!

Nasdaq Inc.

With $1.6 billion in free cash flow on a trailing 12-month basis, Nasdaq believes it remains well-positioned to support organic growth, execute its deleveraging plan, increase the dividend payout ratio over time, and repurchase shares to minimize dilution.

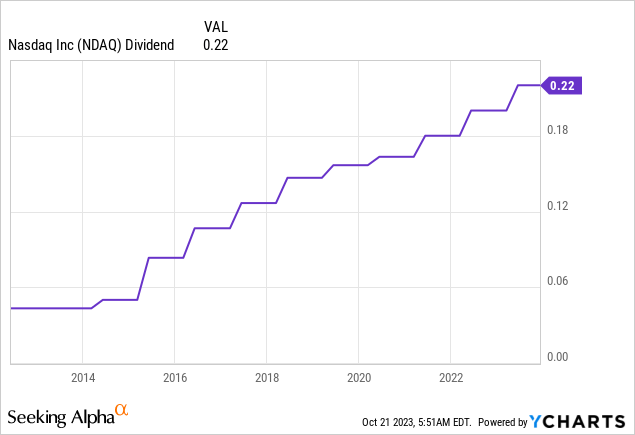

On April 19, the company hiked its dividend by 10% to $0.22 per share per quarter. This translates to a yield of 1.7%. This dividend comes with a 31% payout ratio and a five-year CAGR of 9%.

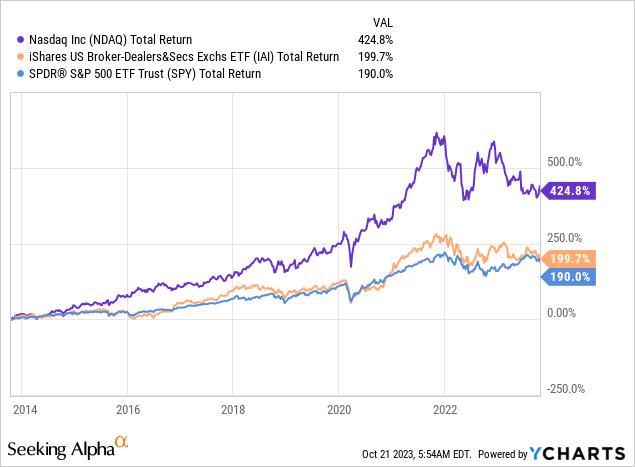

Consistent growth has allowed NDAQ to outperform both the market and its stock exchange peers over the past ten years.

In order to remain on top, the company is consistently innovating, building on the strong foundation we just discussed.

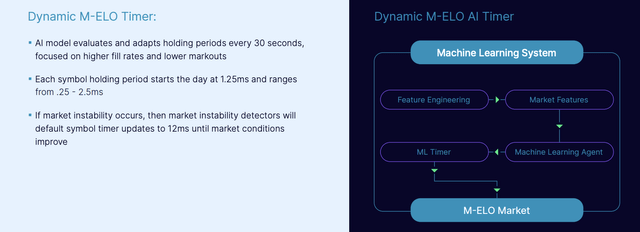

For example, the company is adopting technologies such as cloud and artificial intelligence. The company introduced a new AI-powered order type called Dynamic Midpoint Extended Life Order (Dynamic M-ELO).

Nasdaq Inc.

This order type aims to adapt holding periods throughout the trading day on a stock-by-stock basis to improve fill rates and reduce market friction.

They also launched Nasdaq Metrio, a SaaS-based solution integrating sustainability reporting and workflow offerings from Nasdaq and Metrio. This solution helps corporates collect, measure, and report sustainability data on a single platform.

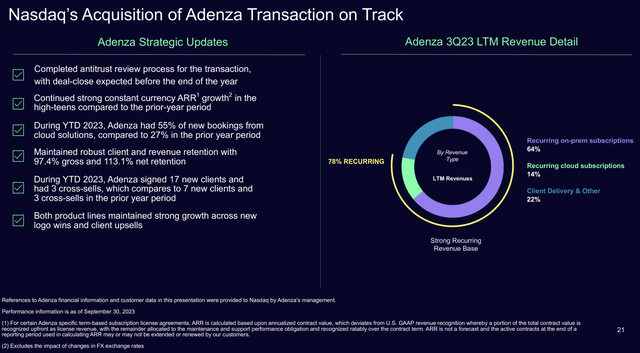

Furthermore, Nasdaq is progressing well toward the closing of the Adenza transaction, which I discussed in great detail in my prior article.

They have completed the anti-trust review, and Thoma Bravo is on track to obtain the remaining approvals from Nordic and Baltic financial regulators.

The transaction is expected to close in the fourth quarter of 2023.

Adenza’s performance in the third quarter was strong, with constant currency ARR growth in the high teens. They added 17 new clients and three cross-sells year-to-date, showing solid growth in net revenue retention.

Nasdaq Inc.

Furthermore, Adenza is making strides toward delivering its solutions through the cloud, with 55% of bookings being for cloud delivery solutions through the first three quarters of 2023.

Furthermore, close to 80% of Adenza’s revenues are recurring, which makes Nasdaq’s cash flows more consistent.

Valuation

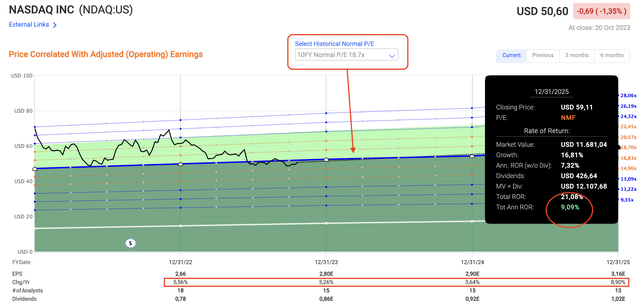

NDAQ is expected to remain relatively unharmed from the current macro environment of sticky inflation, elevated rates, and weakening growth. The company is expected to maintain mid-single-digit EPS growth through 2025, which I highlighted in the chart below.

I also highlighted that Nasdaq’s 10-year normalized P/E multiple is 18.7x. Right now, NDAQ trades at 18.3x EPS. When incorporating expected growth and its longer-term valuation, the stock has the potential to return 9.1% per year through 2025. This is in line with estimates for the broader market.

FAST Graphs

The current consensus price target is $60, which is 20% above the current price. This aligns with the expectations above.

If I were looking for NDAQ exposure, I would try to buy it close to $48, which seems to be an area of strong support.

The stock could go lower if the Fed struggles to contain inflation, which could increase stagflation risks, hurting investors’ risk appetite. Hence, I believe that gradually buying the stocks on our watchlist (like Nasdaq) is the way to go, as it lowers timing risks.

Takeaway

Nasdaq is making significant strides in its transformation into a financial powerhouse with next-gen capabilities.

With a strong financial performance, a focus on innovation, and strategic acquisitions, Nasdaq is well-positioned for growth.

The company’s expansion into areas like Anti-Financial Crime, cloud computing, and AI is paying off, leading to impressive revenue increases.

Nasdaq’s commitment to shareholder returns is supported through its consistent dividend hikes and share repurchases. The company’s financial strength and consistent growth make it an appealing option for long-term investors.

While the stock market environment remains uncertain, Nasdaq’s growth potential and attractive valuation suggest a promising outlook.

Read the full article here