“I believe in analysis and not forecasting.” – Nicolas Darvas

Through September the economy remains solid, but there are formidable headwinds in the months ahead. Currently with the funds rate at 5.5% and the core CPI at 4.1% the real funds rate is 1.4%. That seems to be roughly in line with the level that in the past has significantly slowed the U.S. economy. The Fed may well have to raise the funds rate further in the months ahead but, if inflation continues to shrink slowly, the peak in rates is not far distant.

The Fed can resume its fine-tuning operation later if the need arises, but the general feeling is the Fed does not have far to go. I’ll agree that the bulk of the Fed’s work is done, BUT I don’t believe we can say there is clear sailing ahead on the U.S. economic front.

Government Shutdown

While a last-minute deal helped the US government avert a shutdown, the bad news is the threat of another shutdown has not fully receded. The first-ever removal of the Speaker of the House recently has thrown more uncertainty into the mix-raising the odds of a government shutdown in mid-November. While this situation won’t affect the MACRO view it adds to the uncertainty of many issues that will.

The political dysfunction is coming at a time when debt dynamics, fiscal spending, and an overwhelming amount of Treasury supply are creating worries for investors, rating agencies, and voters. Now to be fair, the government’s deteriorating fiscal outlook should place some upward pressure on bond yields-the market’s way of sending a message to Washington that they need to get their house in order. And, the longer the Fed keeps rates elevated to offset the government’s out-of-control spending, the worse the situation will get.

In an era of low inflation and zero/low interest rates, Congress was able to spend freely with limited consequences. No so today with inflation still hanging on and with the 10-year Treasury yield now hovering around 4.9%. With debt servicing rising at an alarming rate, Congress is either going to have to change its spending habits or the US is going to experience more economic pain down the road.

Here is the dilemma. If a new era of fiscal responsibility is born, fiscal austerity would become a near-term headwind for growth which could ultimately place some downward pressure on interest rates. However, that assumes Inflation is down to or very close to the 2% target, so this growth/inflation/interest rate issue isn’t going to be so easy to solve. However, as I will explain later, an era of fiscal responsibility can NEVER be achieved with the policies and agenda in place today. Now we are faced with other outside forces that are certain to stretch the US fiscal scene to levels never experienced before.

Labor Strife And Higher Wages

The auto workers union is making (in my opinion) some outrageous demands. They are asking for a 40% increase in wages over 4 years, a 20% reduction in the workweek from 40.0 to 32.0 hours, and a guarantee of some job security during the transition to the production of all-electric vehicles. The fact that the administration tossed its full support behind the union and its demands, poisoned any good-faith negotiations between the UAW and the automobile manufacturers because union workers will now believe that their proposals might be attainable.

At the moment anything less than their demands might be deemed unacceptable to rank-and-file union members. The auto manufacturers will probably feel that they are no longer bargaining in good faith because one side has the support of the President. Against this background, it is inconceivable to me that the strike can be settled quickly. As it progresses, the inventory of unsold vehicles will dwindle while sales and revenues slip. The negative impact on the economy will soon be apparent.

Soft Landing?

While investors seem to be pricing a “soft landing,” history is not on their side. The Fed has raised rates at the fastest pace in modern history, and the market is still trying to absorb the impact. This likely will create higher dispersion between companies and asset classes alike, with the volatility offering investors the potential to find companies that are positioned well but negatively impacted by near-term macro events. As rates have spiked, so too have long-term yields.

Yield spreads also bear monitoring. The spread, or difference, between 2-year and 10-year Treasury yields, has been negative all year, i.e., an inverted yield curve, but has narrowed from a record -110 basis-point inversion in March to only 30 basis points today-not positive, but it’s progress. Dating back to 1990, when an inverted yield curve has gone positive it can spell trouble for equities. It is not until the curve goes positive by about 125 basis points, do equities form a bottom and a rally ensues. I suspect we are a very long way from a yield curve that will be that positive.

Geopolitical Turmoil

The past two weeks investors were reminded that they are operating in a world full of turmoil. We spoke about the terrorist attack in Israel last week, and as I’ll speak to later markets tend to eventually calm and overlook these situations. The MACRO scene, however, has been impacted, especially when it comes to the U.S. and its Debt situation. No doubt the US will pitch in with armaments and aid to Israel in what is their “911” event. Add that to the ongoing Ukraine situation and the spending/debt debacle in our economy, the “rubber band” gets stretched once again. The U.S. has pledged to Ukraine and now the administration plans to ask Congress for an “unprecedented support package for Israel’s defense”. Israel that they will “get what they need” to defend themselves.

I’m not suggesting anything be done differently with Ukraine or Israel, but I am citing the facts and reality of the situation. These events along with the continuing overhang of the China/Taiwan situation come at a time when the U.S. finds itself in the weakest fiscal situation since WWII. In the meantime, taxpayers continue to hear the same rhetoric regarding “spending”, as Treasury Secretary Yellen announced that the US can certainly afford two wars. Perhaps that might be true if they were the only issues that require boatloads of money to process. However, they are not.

There is a contingent, in which Ms. Yellen is a firm supporter, that wishes to spend trillions on “climate issues” and an “energy transition”. While the economy is doing well, welfare spending is near or at all-time highs. In fiscal year 2022, the federal government spent $1.19 trillion on more than 80 different welfare programs. That represents almost 20% of total federal spending and a quarter of tax revenues in 2022. That is for WELFARE in a supposedly economy that is “humming along”! The pandemic is over but the country’s food stamp program reached an all-time high in November 2022 and remains at that level.

Then there are the 6-7 million immigrants that have arrived, and they also come with a huge cost to social services, welfare, etc. Finally, the cherry on top of this debt cake. The cost of servicing the “existing debt” (not future debt) will be about the same as the existing Social Security program. In effect, we are soon going to be spending on TWO Social Security programs.

Therefore it is a HUGE “stretch” to assume the U.S. can afford the two wars and will ever be able to enter a period of fiscal responsibility that is so desperately needed.

Macro Summary

It doesn’t take a Wharton School graduate to realize that “other” spending must be curtailed. I realize I keep repeating that, but it is the lynchpin in this MACRO scene that will have the most impact. At some point, this notion that the climate is the BIGGEST threat to our economy has to be scrapped. If it isn’t then you can kiss global economic growth goodbye. Given all of the other existential threats that are REAL, some will slowly come to realize what the common sense crowd has said from day ONE. “The climate ISN’T the biggest threat to our economy”. The only question that remains is – is it already too late?

Between the “issues” at home and with events and threats presenting themselves on multiple fronts abroad, the geopolitical situation is as fragile as it has been in decades. For the U.S., the latter is a self-inflicted policy error that leaves the U.S. stretched and vulnerable like never before. At some point, this WILL have serious effects on the MACRO economic scene. That in turn will negatively impact the financial markets for what could turn out to be a period that is measured in “years”.

The Week On Wall Street

The 3Q23 earnings season ramped up this week with 11% of the S&P 500 market cap reporting results, traders entered the scene with a wait-and-see approach. Financials started the EPS parade and investors liked what they saw and pushed all of the indices to gains of 1+% respectively on Monday.

Tuesday rolled around and a “HOT retail sales number tossed cold water on the enthusiasm as Treasury yields spiked to 52-week highs. The resiliency of this market came to light as the indices staged a complete reversal to wipe out the early-day losses to close flat for the day. The Russell 2000 bucked the selling trend all day and posted a 1% rally.

Selling pressure was stepped up again on Wednesday in what turned out to be a complete wipeout with every index posting a 1+% loss with the Russell giving back all of the previous day’s gain, then adding another 1% to make it a 2+% loss for the day. Thursday was a replay with across-the-board losses in every index and sector finishing in the red.

A negative week ended on a negative note when the S&P posted its fourth consecutive day of losses. For the week, the index dropped 2.4% and that could be considered a fairly mild drawdown considering the negative backdrop. Since the July highs, this S&P pullback has now reached 7.9%.

Every major index closed in the red for the week. The NASDAQ was down for the second week in a row and the Russell 2000 small caps made it three straight weeks of losses.

The Economy

The U.S. leading index fell 0.7% to 104.6 in September. This is the lowest level since June 2020 and follows the 0.5% slide to 105.3 in August. The index has been in decline for 18 consecutive months and has not posted an increase since February 2022. That’s the worst since the 24 straight months of contraction from April 2006 through March 2009. The components were mixed with six making negative contributions. Three components made positive contributions.

LEI (www.conference-board.org/topics/us-leading-indicators)

Consumer

Consumers showed their steadfast resilience and kept spending in September despite grappling with higher prices, interest rates, and a host of other headwinds piling up.

Retail sales rose 0.7% in September, more than twice what economists had expected, and close to a revised 0.8% bump in August. Retail sales in August were inflated after gasoline prices spiked, however. That was not the case in September when gas prices began to ease.

A closely watched category of retail sales that excludes auto dealers, gas stations, and building materials and feeds into the gross domestic product jumped 0.6% last month compared to the prior month.

September’s uptick in retail sales, the sixth consecutive monthly gain, reflects how the U.S. economy has remained resilient despite attempts by the Federal Reserve to cool spending and hiring.

In the good news is bad news backdrop, this number was considered a negative as it potentially keeps the Fed engaged in the rising rate scene.

Manufacturing

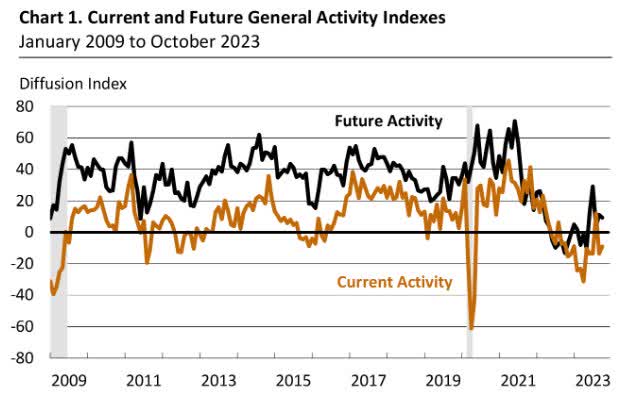

The Philly Fed index rose to -9.0 in October from -13.5, versus a 16-month high of 12.0 in August which was the only positive reading over the last year. Today’s Philly Fed bounce accompanies an Empire State drop to leave a mix that is consistent with a modest up-tilt in the full set of headline and component sentiment readings since a March trough, following a steady descent into Q1 of 2023 from robust peaks in November of 2021.

Philly Fed (www.phillyfed.org)

U.S. Manufacturing remains in recession, and Housing is not far behind.

Housing

The NAHB housing market index tumbled another 4 ticks to 40 in October, the weakest since January, after falling 6 points to 44 in September. The climb in mortgage rates continues to take a toll on builder confidence. The current single-family sales index also fell 4 ticks to 46 after dropping 7 points to 50.

Housing starts climbed 7.0% to 1.35 million in September, a little firmer than projected, after plunging 12.5% to a 1.26 million pace in August. September’s clip was the weakest since June 2020. Building permits declined 4.4% to 1.47 million after jumping 6.8% to 1.54 million in the prior month.

Existing home sales fell 2.0% to 3.96 million in September after sliding 0.7% to a 4.04 million pace in August. This is the slowest pace since October 2010. The median sales price slid to $394,300 after dipping to $404,100. It is the lowest since April.

Sales look poised for a 21% Q4 contraction rate, after contraction rates of 19.7% in Q3 and a 6.9% rate in Q2. Sales remain depressed by limited supply, as owners are unwilling to relinquish properties in the current environment of elevated mortgage rates and home prices.

The Fed

Chair Powell spoke to the Economic Club of New York on Thursday, and the mix of his remarks made for a volatile trading session. The indication that the FOMC could be sidelined by the rise in longer-term interest rates that are doing some of the Fed’s heavy lifting was taken by the markets as a dovish stance and yields and the US Dollar tumbled, while Wall Street rallied.

However, the markets shuddered at Powel’s view that the economy’s resilience could be because rates have not been high enough for long enough, suggesting a restrictive stance for a lot longer until the economy slows sufficiently to bring inflation to 2%.

That is a message I sent a couple of months ago when we started to see the forecasts for a solid GDP forecast for Q3.– Fed policy isn’t restrictive enough.

Once again there is NOTHING to see here – It’s HIGHER for longer and investors better start believing that the longer part is going to be VERY long. Yet I hear analysts continue to forecast rate cuts next year. The dilemma the equity market is facing is twofold. Higher for Longer is scary and IF rates are indeed cut – then that means the economy is falling off a cliff. That is also frightening for equities.

The U.S. Political Scene

House Speaker Vote. It now appears there is no obvious path to 217 votes for Jordan, leaving some Republicans to wonder if they could elect current temporary Speaker Pro Tempore McHenry (R-NC). It’s unclear if he can garner 217 votes either.

The continuing resolution keeping the government open expires on 11/17, and besides the geo-political turmoil around the world that needs to be addressed, the longer the House goes without reaching an agreement on who to elect as speaker, the more likely it is that we reach that mid-November deadline without a budget agreement.

Then there is the administration’s emergency request to approve billions more in aid for Ukraine and Israel. With the slim Republican majority, they would need 98% of their contingent to back ONE candidate, and as we have seen that is an impossible task. An easy solution would be for the President to solve the issue by persuading a literal “handful” of Democrats to get behind a candidate (ALL have unanimously voted against any Republican nominee) and remove this obstacle.

As far as the shutdown, as stated in earlier updates, it’s a non-event for the markets. If the aid packages are deemed that important then the roadblock can be easily eliminated to approve the spending. With complete dysfunction in Washington, we’re all suffering the consequences of politicians.

The Geopolitical Scene

After three years of overlapping crises, it is natural to wonder whether the surprise attack on Israel and its subsequent declaration of war poses another threat to the global economy and supply chains around the world. While these concerns are valid, I do not think the tensions in the Middle East will lead to any major disruptions. Unlike Russia and Ukraine, Israel is not a huge oil or commodities supplier to the world.

Because of this, it is unlikely that the Israeli-Hamas war will disrupt supply chains or drag down economic confidence in the same way the Russia-Ukraine war or the pandemic did over the last few years. A major impact on supply chains could occur if there was an escalation in the war throughout the region.

Fortunately, I think we have to view that as a LOW probability of occurrence. The only way the oil supply could be disrupted is if Iran were to enter the war. Iran has long been a financial backer of terrorist groups like Hamas, as well as Hezbollah in Lebanon, but that is very different from engaging in a direct military confrontation with Israel. As the leadership in Tehran knows very well, Israel is a nuclear-armed country and has the strongest air force in the Middle East. It would be downright suicidal for Iran to get involved. However, for a variety of other reasons, I do believe that the added uncertainty will hold oil prices near the $85-$90/barrel range.

Not to minimize the impact and devastation of the events that are taking place in the Israeli conflict, but the war has not altered my asset class views or outlook for the US economy or earnings growth. First, from an economic perspective, Israel is a small country, with a GDP of $521 billion-making it the 29th largest country in the world, representing only 0.5% of world GDP. To put this into perspective, when measured by GDP, Israel would rank as the 13th largest state in the US (roughly the size of Virginia) and when compared to companies in the S&P 500, Israel is roughly the same size as the 15th largest company (Eli Lilly).

Additionally, Israel is not a significant trade partner of the US, making up only 0.7% of both US imports and exports (the 25th and 29th largest trade partner respectively). And because of this, Israel is not big enough to derail the US economy from its current path. From an earnings perspective, given that I don’t expect a significant economic impact from the war, combined with the fact that the S&P 500 receives only 0.2% and 2.8% of revenues from Israel and the Middle East region respectively, the conflict will not have a meaningful impact on earnings.

Finally, it is worth noting that previous events in the region have not had a significant market impact. Unfortunately, conflict in this region is nothing new. Bespoke Investment Group notes that in the previous 11 major conflicts, the S&P 500 was up ~15% on average in the 12 months following the onset of the conflict and was positive 75% of the time.

While this terrorist act may not change my economic views, it does highlight what is yet another global policy error that can have major MACRO consequences in the future.

Iran

Iran did some saber-rattling this week by calling for an oil embargo on Israel. The fact that Iran is in a position to make any ‘calls’ in this war is preposterous. The lack of global leadership in dealing with Iran is why there is a second global war being waged today. Shockingly the US continues to be the leading player in shirking responsibility by sending billions to what the U.S State Department has acknowledged as a state sponsor of terror.

If this terrorist attack isn’t a wake-up call to impose economic sanctions that will isolate and destroy the Iranian economy once and for all then we can expect more of the same in the future. The FACTS, not opinion, rhetoric, or “spin”, but FACTS, tell us the existing sanctions on Iran are NOT being enforced. Iranian oil exports have tripled in the last 2+ years. Instead of crippling their economy, the country’s coffers have been enriched in the last 2 years.

If common sense doesn’t prevail, this war is just the beginning of global turmoil. The U.S. received yet another reminder that ‘policy’ errors have consequences when a Navy warship intercepted Iranian missiles, headed for Israel. After missing the opportunity to buy oil at a cheaper price, the U.S. finally decided to begin replenishing the oil removed from the SPR (Strategic Petroleum Reserve). Energy Secretary Granholm has stated it may take up to two years to bring the reserve back up to prior levels. Combine this with U.S. Domestic issues that I’ll present next, and it’s easy to see why the price of crude oil will stay elevated and perhaps ratchet higher.

There is NO reason to abandon the energy trade.

Food For Thought

EXXON outfoxed the “Agenda”.

Exxon Mobil CEO Darren Woods announced that he struck a $59.5 billion deal to buy oil and gas explorer Pioneer Natural Resources.

This deal can be read as a bet on U.S. shale fracking and a side-step against the US anti-fossil fuels policies. The acquisition comes at a time when the present hostile regulatory environment makes it more difficult to explore and develop new resources.

This deal accomplishes quite a lot for Exxon (XOM) as the company becomes the biggest player in the rich Permian Basin that spans Texas and New Mexico. In addition, the rising rate environment is making it more expensive to drill, and that should encourage more M &A activity.

Being a low-cost producer with an enviable list of land assets, Pioneer Natural Resources is a “prize”. Exxon will now have the luxury of bypassing the arduous and at times impossible task of acquiring new leases and permits. That means the newly combined entity will drill longer, more productive horizontal wells without wasting more time and money. Exxon has already stated that it can drill longer “laterals” Which means fewer wells which reduces the environmental impact.

A the end of the day Exxon expects to double its current Permian production and nearly quadruple it by 2027 to two million barrels of oil equivalent a day, which is more than half of its current worldwide production. In a stroke of genius, Exxon is making a huge bet on U.S. shale, while defraying costs, and in effect has outgamed the system that is at war with fossil fuels. In essence, this buyout of Pioneer makes Exxon less vulnerable to government policies aimed at reducing long-term supply and demand.

U.S. oil output has been increasing mainly because producers are running down their inventory of drilled but uncompleted wells. However, that is about to end, as the number of those wells has dropped to 830 from 3,330 in the Permian in the last 2 years. The Administration continues to slow-walk new drilling permits and leases, which increases the incentive for producers to grow by acquisition.

The Interior Department last month released its statutorily mandated five-year offshore leasing plan, more than a year late. It included a mere three auctions through 2029-the least necessary to comply with the IRA. Since 1992 no five-year plan has offered fewer than 11 lease sales. That action sends large oil companies to move their operations to different parts of the world.

The world will need fossil fuels for many decades, and at some point, the energy transition fraught with all of its issues will be identified as a supplement rather than a replacement. The costs associated with the transition run into the trillions and the money that has already been buried in this project has not produced anywhere near the solution that is required to run a productive economy.

Finally, U.S. workers and the U.S. economy would be better off if production happened at home rather than overseas. The U.S. energy policy that I have warned about for the past two years is starting to show that ‘policies’ have consequences.

Investment Backdrop

The indices are all at a point where they could still go either way. Given all of the “outside” influences, the best scenario might be more sideways action. Plenty of starts and stops, with uncertainty sure seems like it will be part of the scene for a while. Perhaps for the entire 4th quarter. That tells me to stay diversified and look for “special situations”.

The Daily Chart of the S&P 500 (SPY)

It’s easy to see why I use technical analysis as part of my strategy. The S&P 500 rallied to a resistance trend line and was turned away. The battle will now be waged at what is considered to be an important support area for the index.

S&P 500 (www.tc2000.com)

The ball is in the BULL’s court and it will soon be time for them to step up and defend their position. A ‘break’ of support opens up a completely different set of circumstances on the technical front.

Final Thoughts

Once sentiment sours, NOTHING is going to change that downward price action. Plenty is going on now that keeps the algorithms in control and why the volatility is ramped up. Headlines out of Israel, Drone attacks in Iraq, Navy warship intercepts Iranian missiles (U.S. policy errors have consequences), D.C. dysfunction, and higher Treasury yields are all impacting short-term sentiment.

I’ve come to find that in most cases market “reactions” were consistent with what the “charts” are implying. Simply because they are giving us the pulse of all of the emotions that are present. Any investor that isn’t using the “technical aspects” of the investment landscape as part of their strategy is coming to the gunfight with a knife. You are destined to fail.

I don’t care about the reasons for the volatility and how the market is acting. I let price action and sentiment be my arbiters rather than headlines. To that end, I can uncover strong stocks, and these “stronger” (winning) stocks have remained VERY resilient in this poor backdrop. These along with others are the names to be involved in now. There is a BULL market in this mix BUT it is VERY selective.

THANKS to all of the readers that contribute to this forum to make these articles a better experience for everyone.

Best of Luck to Everyone!

Read the full article here