Positive prospects for risk assessment giant Moody’s (NYSE:MCO), who is positioned to capitalize on risk assessment opportunities in KYC, and ESG. Prospects appear baked into their current valuation.

Company Overview

Moody’s is a risk assessment firm. The company has two reportable segments:

Moody’s Investors Service [MIS] which provides credit rating opinions and related information. Bulk of this segment’s revenues are generated from rating fees paid by debt issuers. This is Moody’s most profitable segment in terms of margins with segment operating margins of over 55% compared with roughly around 30% for their Moody’s Analytics segment.

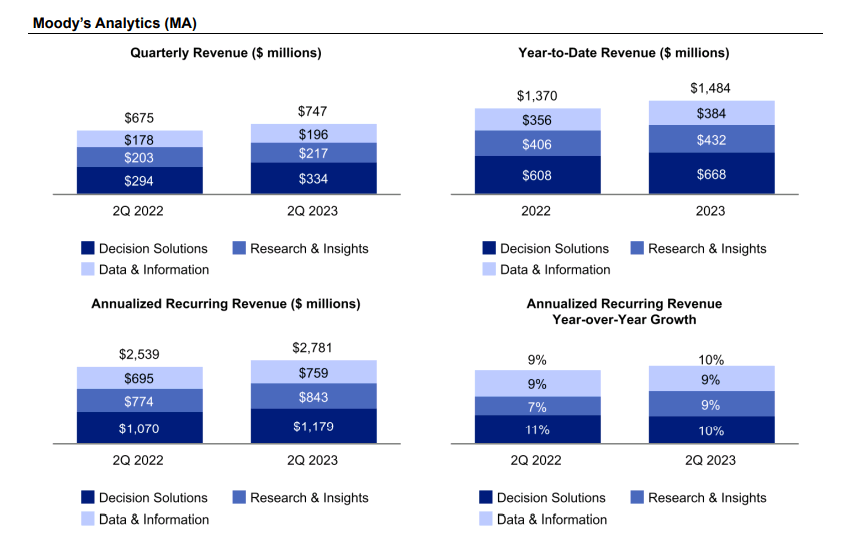

Moody’s Analytics [MA] which provides financial intelligence, research and analytical tools to support customers’ growth, efficiency and risk management objectives. There are three main lines of business within this segment namely Decision Solutions, Research & Insights, and Data & Information. This segment accounted for 53% of total revenues in 1H 2023.

1H 2023: revenues up slightly driven by MIS slowdown

For the first half of 2023, Moody’s reported a 2% YoY increase in revenues to $2.9 billion. MA revenues rose 8% to $1.484 billion supported by sustained demand for analytics. All lines of business within the segment grew during the half year, and annualized recurring revenue rose 10% in Q2 2023, continuing the 10% growth reported the previous quarter. Customer retention stood at 93% in Q2 2023.

Moody’s Corporation 10-Q, Q2 2023

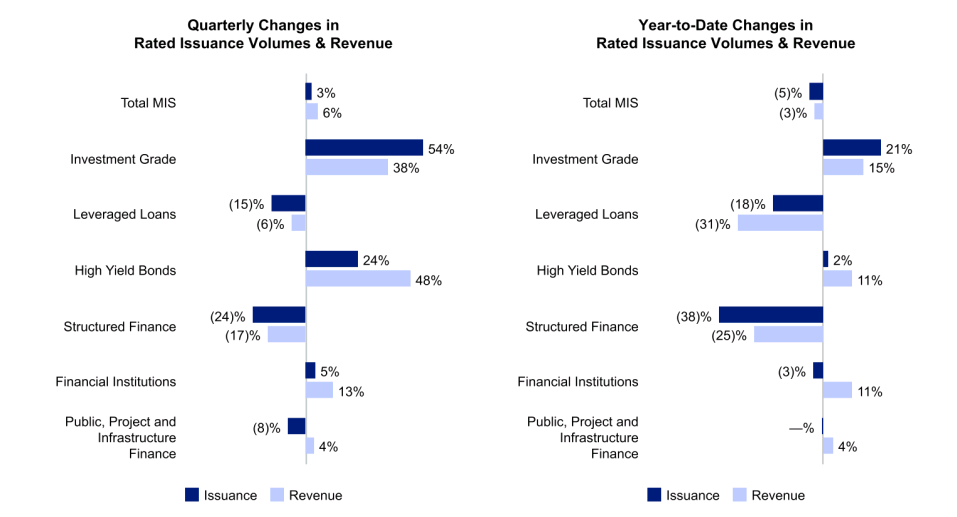

MIS revenues declined 3% YoY to $1.48 billion partly due to strong comps in Q1; total MIS rated issuance volumes improved to 3% in Q2 2023 outpacing revenue growth of 6%, improving from the 13% decline registered in Q1 2023. The improvement was driven by a steady improvement in the issuance environment led by a 54% increase in investment grade activity in Q2 2023.

Moody’s Corporation 10-Q, Q2 2023

Operating profit however declined to $1.104 billion in 1H 2023 from $1.164 billion in 1H 2022, leading to a decline in operating margin to 37.2% in 1H 2023 from 40% in 1H 2022. The drop was due to investments in generative AI. Free cash flows improved to $1.085 billion for 1H 2023, a 72% YoY jump from $628 million the same period last year. The increase was due to an improvement in working capital.

Near term, improving credit activity led management to upgrade MIS revenue guidance for the full year to high single digit growth (from low to mid-single digit growth previously). MA guidance remained unchanged with revenue projected to grow 10% for the full year. MA margins are expected to improve over the coming quarters on the back of their restructuring program and cost saving initiatives. Full year 2023 revenues are projected to increase in the high single digits (improving from last year’s 12% YoY revenue decline) while operating margins are projected at 37% (improving from 34.4% last year). Free cash flows are projected at $1.6 billion to $1.8 billion (up from last year $1.19 billion which was impacted by a tax-related working capital headwind).

Well positioned to capitalize on long-term risk assessment opportunities around ESG, KYC, emerging markets

Looking further ahead, prospects are generally positive for the company. Credit activity should recover along with a recovery in economic growth and a potential interest rate cut next year. Management noted in their Q2 2023 earnings call that the spike in investment grade issuance could “open the door for issuance further down the rating scale”.

Additionally, the company continues to expand their market share and capabilities in adjacent domains like ESG and KYC through acquisitions. Recent notable acquisitions include Bogard and RDC (which expanded their KYC coverage), RMS (which expanded their climate risk capabilities), and Catylist (which expanded their commercial real estate data sets and analytics capabilities). Management sees KYC and ESG as two growth opportunities given increasingly stringent regulations. Moody’s acquisitions strategy focuses on expanding their risk assessment capabilities in these areas, which not only supports inorganic revenue growth but also opens organic revenue growth avenues through cross-selling opportunities to existing clients. The acquisitions also expand Moody’s proprietary data sets which combined enable Moody’s to offer unique insights to clients, better serving client objectives related to risk assessment across various domains (like helping clients with commercial real estate interests, including commercial real estate insurers, better assess ESG risks stemming from climate change).

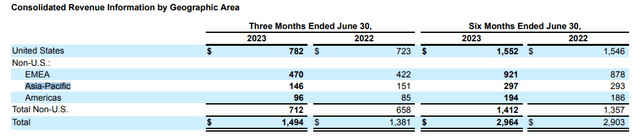

Meanwhile Moody’s acquisitions of SCRiesgo and MARC expands the company’s presence in Latin America and ASEAN respectively, positioning them to capitalize on credit growth opportunities in emerging markets which according to management accounts for as much as 50% of GDP but just 10% of cross-border issuance. Non-U.S. markets account for a smaller share of Moody’s revenues than the U.S. which generates 53% of revenues alone.

Moody’s Corporation, Q2 2023 10-Q

Stricter regulations are driving risk assessment demands and Moody’s, one of the “Big Three” credit rating agencies (the other two being S&P Global (SPGI) and Fitch) is well positioned to capitalize. The trio have long dominated the market with a collective market share of around 95% with Moody’s and S&P Global being the bigger among the three (Fitch has a market share of around 16%). Moody’s long standing reputation in the risk assessment space, operational history, and an expanding database of proprietary datasets present considerable barriers to entry for new entrants.

Conclusion

Moody’s has a moderate buy analyst consensus rating.

Seeking Alpha

With a forward P/E of 33.8, Moody’s earnings multiple is considerably higher than the sector median of 9 and higher than their five year average of 28.58. Their prospects appear baked in at this point.

|

Moody’s |

S&P Global |

|

|

Forward P/E |

33.8 |

31 |

|

TTM FCF yield % |

2.65% |

2.5% |

|

Return on assets % |

8.35% |

4.25% |

Read the full article here