Overview

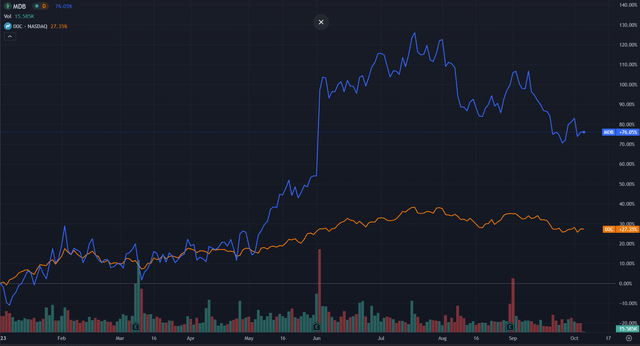

MongoDB (NASDAQ:MDB) stock has had an excellent run this year, outpacing the NASDAQ Composite’s price return nearly 3-to-1 and returning roughly 76% year-to-date. Notably, price action in this stock has been concentrated around its earnings reports, indicating buoyant investor sentiment that has been a direct result of its quarterly performance.

Seeking Alpha

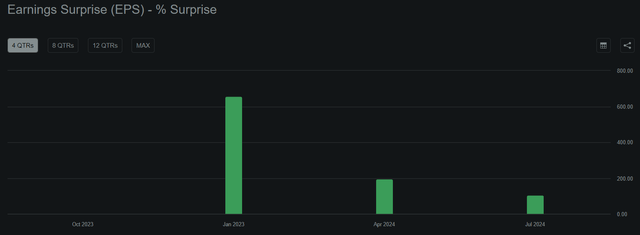

The earnings trendline here has indeed been favorable, with there now being 3 quarters in a row of exceptional outperformance vis-à-vis consensus earnings expectations. Coming off a smashing 657% beat for fiscal Q4, MongoDB has continued to crush consensus. Fiscal Q1 ’24 saw the company outperform on EPS by 195% and fiscal Q2 ’24 yielded a surprise to the upside of 106%.

Seeking Alpha

I previously took a bullish view on MongoDB’s earnings prospects heading into its Q1 ’24 quarterly release. My logic at the time was that general market uncertainty around cloud earnings had served to depress expectations for MongoDB in line with that of other major cloud computing providers. This turned out to be prescient and has now been priced into this stock as well as others in the cloud business.

Of course, time has now brought us into a different period. Throughout 2024 the cloud sector has recovered and appreciated markedly, and MongoDB in particular has continued its strong run on earnings growth. This implies that there is a new narrative as well as a novel set of price drivers for this stock. We should now be asking whether consensus has caught up and whether we should still expect MongoDB to outperform on earnings, as well as investigating the stock’s momentum and valuation profile more generally. This will give us a view into how its shares are set to perform across the next several quarters.

Quarterly Performance, Product Development, and Trendlines

While the most recent quarter’s results for MongoDB were released back in August, it’s worth reviewing where things stand and what there is to pay attention to from management’s perspective. Important to note is continued momentum for the company’s core Atlas product, an integrated set of cloud-native data processing services that now accounts for 63% of overall revenue. Revenue for the Atlas suite grew 38% y/y and overall revenues grew 40% y/y. Several new products were announced, including Atlas Stream Processing (for data streams) as well as Relational Migrator, a tool for porting SQL databases into MongoDB unified SQL/NoSQL system.

Several initiatives around artificial intelligence have also begun to bear fruit. The primary one worth noting is Atlas Vector Search, a semantic search product that allows business users to leverage natural language to search across large quantities of mutually distinct data sets. Management has also made clear that they believe their product is uniquely positioned to benefit from the nascent AI era. This is sensible due to certain technical requirements of artificially intelligent processing, something which management details. This centers around the database’s capacity for processing a wide range of heterogeneous data types concurrently, something enabled by the firm’s unique Document Model data schema. In-database parallel computations are also a feature of MongoDB, something which should map well to the parallel hardware utilized in artificial intelligence applications. Finally, flexible scaling allows for datasets to grow unbounded – another important aspect for making it useful in the context of AI applications.

Seeking Alpha

For MongoDB, product development and general financial metrics appear to continue to be excellent as of its most recent quarter. Continued upward momentum in the stock appears justified on this basis. In order to establish a trendline and a forward view, we can now broaden our financial lens to include other salient metrics as well as the last few quarters of results.

Year-over-year revenue growth actually picked up in the latest quarter, approaching 39.6% for the highest figure that we’ve seen since fiscal Q3 ’23 (ending Oct 2022). While this may not be the pinnacle as to MongoDB’s rate of yearly growth over the last 10 quarters, it is still good to see this level of momentum in the near term. There does not appear to be an imminent slowdown as to top-line growth here.

Seeking Alpha

Looking at the company’s cost structure as well as its bottom line, we can also see some recent momentum in this regard. Total operating expenses have been declining for 4 quarters in a row, notably hitting their lowest point in 10 quarters as of fiscal Q2 ’24. This also resulted in the company getting closer to operating breakeven on a GAAP basis, with a GAAP operating loss of 11.6% in the most recent period.

Seeking Alpha

GAAP net loss also shrank markedly in the latest quarter and is now closer to breakeven than it has been at any point previously.

Seeking Alpha

Moving on to cash flow, a different picture emerges. Cash from operations for MongoDB has not been particularly consistent, and its most recent quarter actually showed its largest loss in a year.

Seeking Alpha

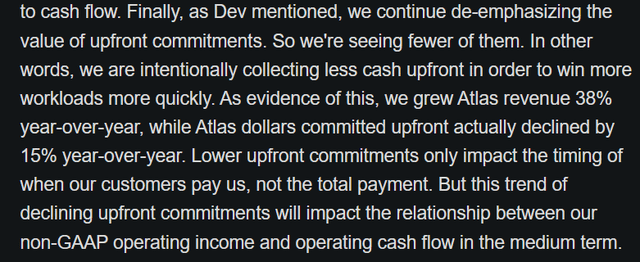

This likely stems from the company’s shifting posture as to its contracts. While they previously were looking to front-load commitments and incentivized their sales force to sign people up for one year, this is no longer the case. Given the significance of this change, it will be interesting to watch how this metric plays out. Ultimately I will be looking for this metric to restabilize and return to upward growth, likely in conjunction with GAAP profitability. On the other hand, however, it is an indicator of confidence – or perhaps prudence – for MongoDB’s management to be oriented towards more long-term contracts and maximizing total workloads (units of cloud utilizations) per customer.

Seeking Alpha

Overall things look sound as to MongoDB’s fundamental picture and overall trajectory. While the picture is not perfectly aligned, particularly around cash flows, I believe that momentum is certainly being maintained and even accelerated as of the company’s most recent quarter.

Valuation

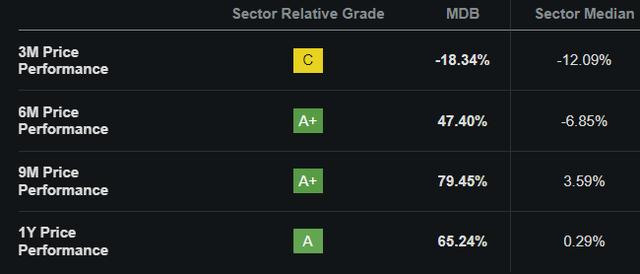

Given MongoDB’s significant appreciation over the past year, it is sensible to check in on its momentum and valuation metrics to see if things are still within a sensible range. Off the bat we can note that its shares have actually underperformed the IT sector at large over the last 3 months, something which is in stark contrast relative to the rest of the past year. This level of softening is worth paying attention to, as it indicates some bearish sentiment around the company’s future.

Seeking Alpha

As to valuation metrics, we can readily conclude that this is not a cheap stock. Since MongoDB is not yet profitable on a GAAP basis we must stick to non-GAAP metrics. Here we can see that this stock is quite expensive on a price/earnings basis relative to the IT sector at large, trading at nearly a 7x premium on a trailing basis and nearly a 6x premium on a forward basis. I don’t think we can infer too much from the valuation disparity across trailing/forward multiples in this particular instance.

Seeking Alpha

This is undoubtedly a ‘growth’ valuation and is quite likely contingent on the company’s capacity to maintain it. Growing well in excess of the sector’s median growth rate while not being profitable on a GAAP basis, this is a sensible conclusion to draw. The risk then becomes clear; MongoDB stock can sell off significantly if it has a quarter in which growth is materially slower than it has been in recent periods.

Seeking Alpha

Conclusion

Overall I remain bullish on MongoDB and think the stock should continue to do well in the year ahead. While admittedly expensive from a valuation perspective, I think that the company can continue to grow at the rates that it has been and maintain what I consider to be a ‘growth valuation’. This centers around its product base and notably relevant technology capabilities for artificially intelligent computing. The other aspect of this is the firm’s steady progress towards GAAP profitability, something which it looks to be roughly 2 quarters away from. This should further undergird its growth prospects and help it to maintain an elevated multiple. Considering the trajectory here, I am going to call it a buy.

Read the full article here