Introduction

Despite a background steeped in Japanese tradition, Mizuho Financial Group (NYSE:MFG) is undergoing a radical makeover. The idea is to reform the old corporate identity, a task many Japanese corporations face, ultimately to build up profitability and shareholder value.

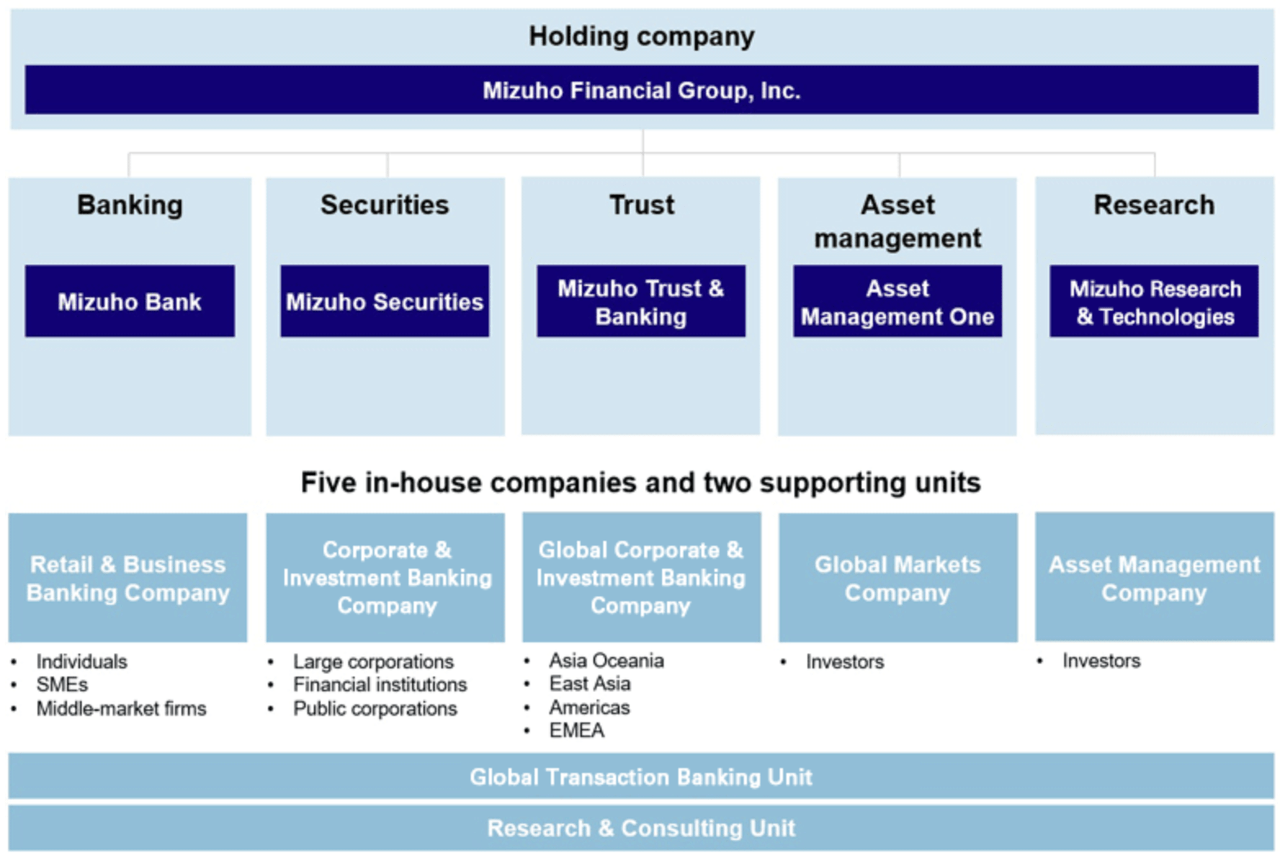

Group structure (Mizuho)

These efforts are already paying off. Over the past year, the stock returned 54% including dividends, outperforming the US banking industry which was in the red with -5%. Japan as a whole has seen outsized interest from investors as of late, after many years of lackluster showing.

Mizuho by now has fully recovered from the wreckage of the financial crisis and even made headway in lifting meager returns characteristic of Japanese banks. Its price-to-book has definitely reacted to these developments, but has little room left to full value.

Financial update

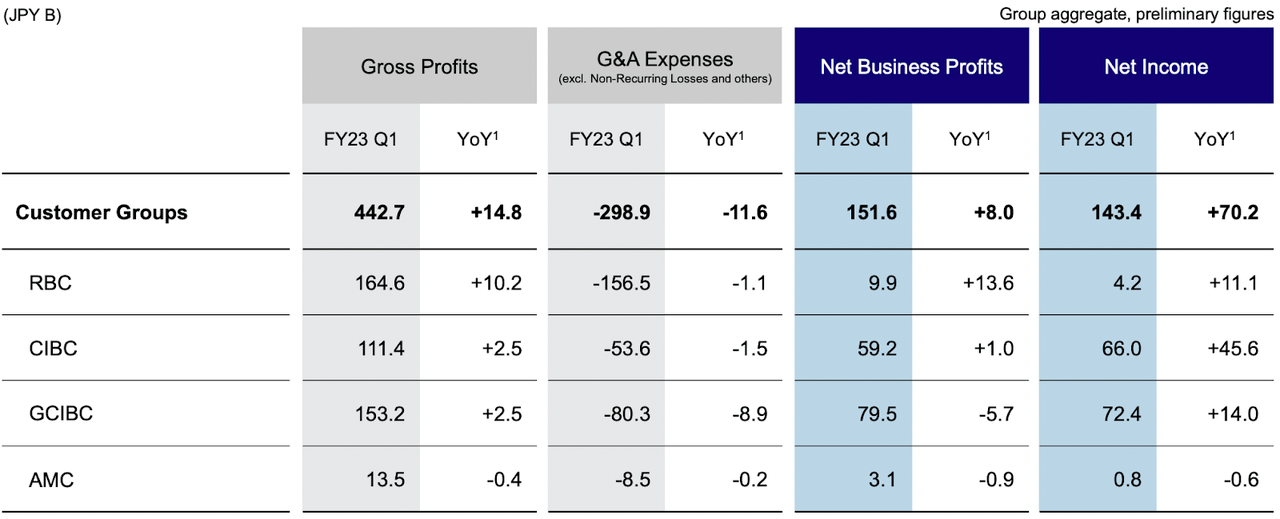

After a steady FY22, Q1 of FY23 continued the streak of positive results with a 6.5% growth in consolidated gross profits and a growth of 4.8% in consolidated net profits, mainly owing to performance in Retail & Business Banking.

Results by in-house company (Mizuho)

Net interest income at ¥217b made up 35.5% of consolidated gross profits; non-interest income for in-house companies totalled ¥244b.

Attributable profit went up 54% year-on-year, largely due to a recovery in credit costs, as in gains from unwinding of loan loss provisions. This has taken Mizuho to 40% of its annual target for attributable profit that is ¥610b.

At the same time, G&A expenses coming from “growth areas” increased slightly, which follows the latest medium-term management plan defined as “a period for shifting to business expansion stage”.

Financial health

The group’s capital position has been stable with CET1 ratio within the targeted range, at 10.1% as of June 2023. Leverage ratio, currently at 4.4%, stays above the regulatory requirement for systemically important financial institutions.

The loan book is diversified with more than 40% originating outside Japan. Non-performing loans stand at a low 1.1%. Loan-to-deposits, a traditional measure of liquidity, is an adequate 55% for the consolidated balance sheet.

Economic prognosis

For the longest time, Japanese banks struggled with ultra-low interest rates that failed to spur the sluggish economy. Though megabanks such as Mizuho (alongside Mitsubishi UFJ and Sumitomo Mitsui) have been spared from the worst of the damage thanks to their far reaching exposure to external markets.

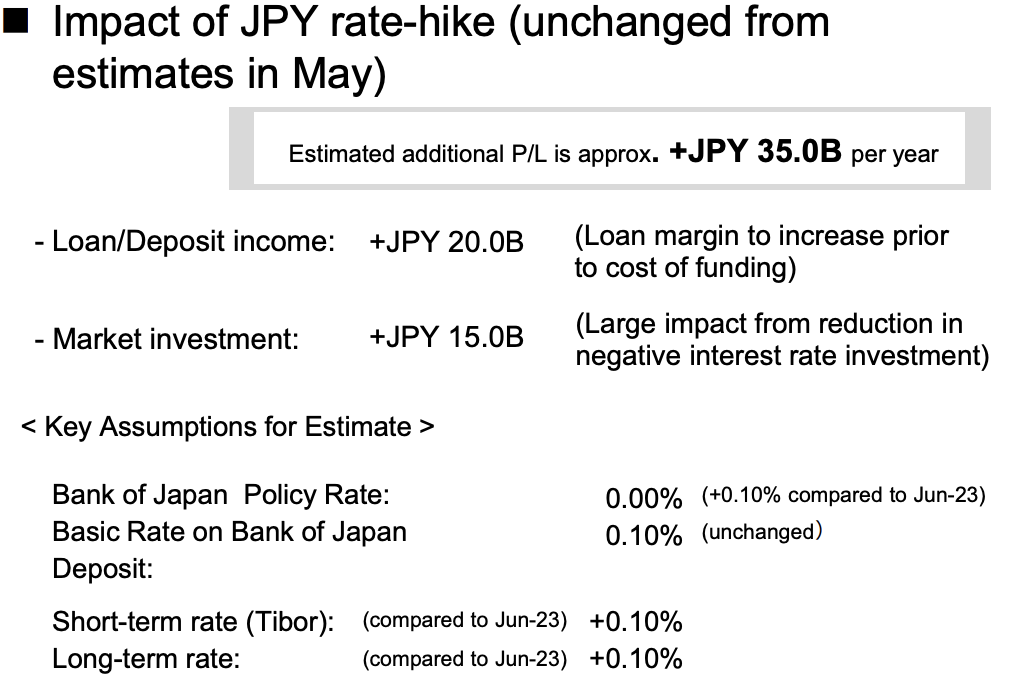

The end to monetary stimulus measures may be in sight. In July, the Bank of Japan raised the cap on long-term government bond yields from 0.5% to 1%, which implies the higher market rate of interest. Some economic changes may be forcing the central bank’s hand. Consumption is rising, and inflation persists above the targeted 2%; wage growth is picking up pace.

Meanwhile, the weak yen has been benefiting many Japanese exporters and holders of foreign assets. It has simultaneously hurt the valuation of domestic companies — possibly Mizuho’s too (as argued by Seeking Alpha’s Valkyrie Trading Society). Even so, the banking lobby is anxious about the prospect of a sudden reversal in the direction of interest rates and currency.

Mizuho

Valuation

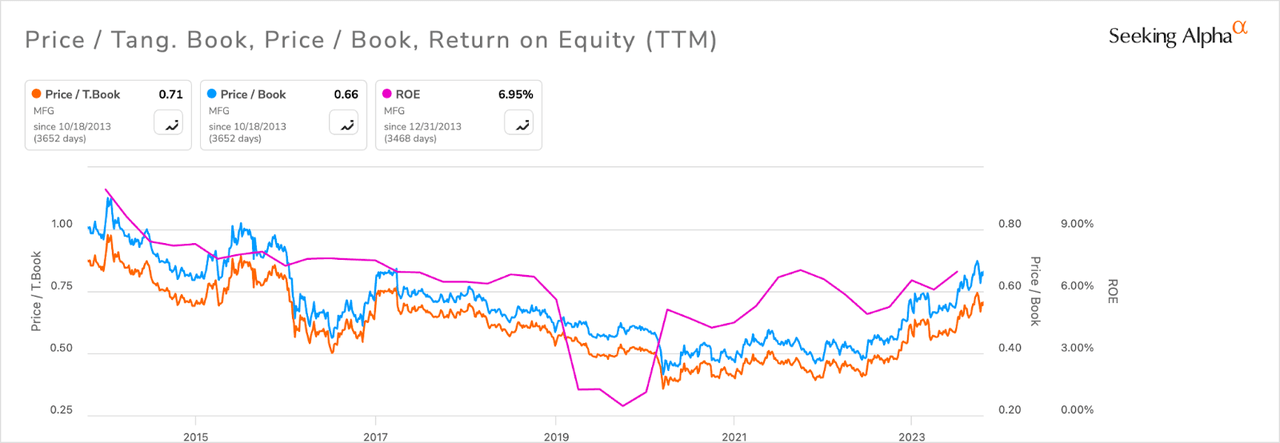

Based on price-to-book ratio, MFG remains comparatively affordable at 0.66x (0.71x tangible book), below the Financials sector median. However, relative to the historical valuation, it is near the five-year high that was reached at 0.70x P/B (0.75x tangible book) about a month ago.

Seeking Alpha

Notice that through the years ROE moved in rough tandem with book value multiples; the upward momentum has become especially pronounced since mid-2022. This is a mark of a sound financial firm.

Mizuho supplements price returns with regular growing dividends currently yielding 3.8%.

Summary

Mizuho’s importance for Japan and its globally active corporations cannot be overestimated. In fact, promoting Japan and its businesses abroad is the group’s core mission.

But like other Japanese banks, Mizuho endured long periods of poor profitability, a result of the country’s drawn-out struggle with deflation. Its ROE, although improving and close to targeted 8%, is still low versus the sector’s 11.22%; ROA is a paltry 0.2% compared to the median 1.15%.

The stock’s trading below book value relative to US peers hence makes sense. The good news is that Mizuho has been proactive. It is trying to downsize to reduce costs, mainly in retail banking, while investing in profitable businesses like Global Markets and institutional banking.

More importantly, it has set a solid foundation for a more diverse revenue stream both in Japan and internationally. Mizuho positions itself as a universal bank cross-selling products to customers and sees a strong competitive advantage in its ability to rotate personnel across business lines.

But a vast integrated structure such as Mizuho’s obviously makes for a more complex business. In foreign markets, for one, Japanese megabanks have struggled with matching their lending volumes to deposits. This leaves them exposed to funding risks which are now much more expensive to manage.

That aside, buy Mizuho stock for its potential for long-term profit growth and dedication to returning value to shareholders.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here