Mitek Systems (NASDAQ:MITK) operates an identity validation platform. The company has been growing at a very good pace with mostly organic performance. I believe that Mitek is poised for long-term margin expansion along with a good amount of further growth in the growing identity verification market. The current valuation doesn’t seem to reflect Mitek’s future prospects as my DCF model estimates a very high upside for the stock. I believe that the stock is worthy of a buy rating at the current price.

The Company & Stock

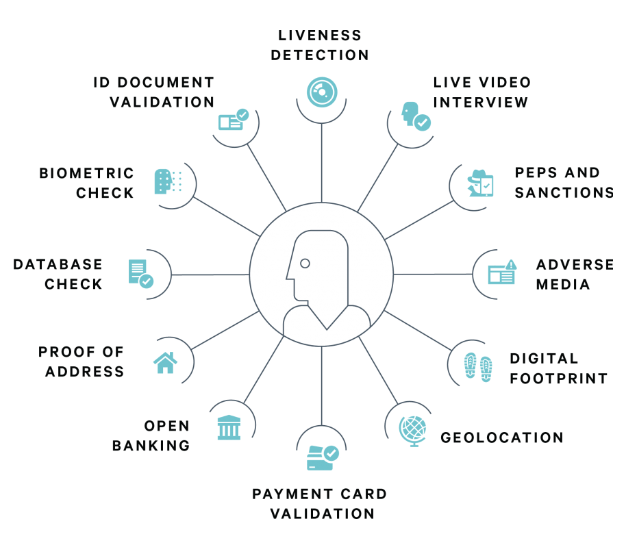

Mitek offers an identity validation solution through the company’s MiVIP platform. The company is operating on a growing industry – in Mitek’s June investor presentation, the company estimates the identity verification market will grow at a CAGR of 15.5% until 2029. Mitek’s platform takes into account multiple factors for a complete analysis of the customer’s verifiability. For example, the platform accounts for biometric checks, proof of address, geolocation, and digital footprint:

miteksystems.com

In addition, Mitek has other offerings – the company also provides biometric authentication software MiPass, that affirms a customer’s validity through biometric analysis, a mobile deposit platform used by over 6500 financial institutions that provides customers the ability to deposit checks on a mobile device, and a check fraud defender that scans for check fraud.

The company’s offering seems to be very good in quality. Mitek has a trailing NRR rate of 120% as communicated in the company’s Q3 earnings call. Mitek’s customers also include a good amount of large companies – the company has customers such as PayPal, Airbnb, Chase, Morgan Stanley, MasterCard, Ameritrade, and Accenture.

Mitek’s return on the stock market has been decent, but not fantastic. Mitek hasn’t paid a dividend as the company’s cash flows have been used in a couple of acquisitions. The company’s stock price has appreciated at a CAGR of 7.1% over the past ten years:

Ten-Year Stock Chart (Seeking Alpha)

Financials

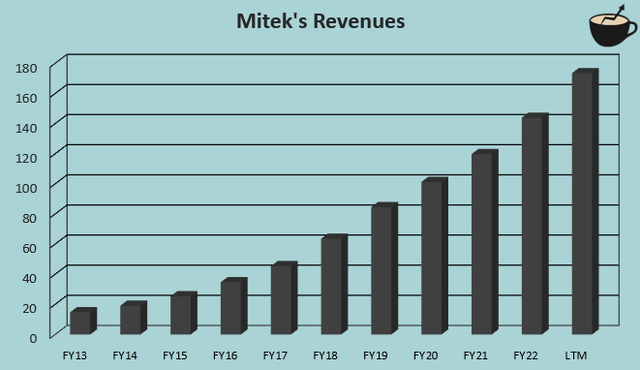

Mitek’s revenues have grown rapidly. From FY2013 to FY2022, the company’s compounded annual growth has been 28.8%:

Author’s Calculation Using Seeking Alpha Data

Mitek’s achieved growth has been achieved in a very stable manner. More than just constant annual growth, Mitek’s quarterly year-over-year growth has been positive in every quarter from Q2/FY2013.

The growth seems to have partly halted recently, as in Q3/FY2023 Mitek’s revenues only grew by 9.5%. The poor performance was driven by a lacking performance in the identity validation segment as the segment’s revenues only climbed by 6% year-over-year. Mitek’s CEO Max Carnecchia indirectly attributed the slower growth to a more difficult macroeconomic environment in Mitek’s Q3 earnings call. As an encouraging sign, Carnecchia did guide for growth in the mid-teens for the segment in Q4 – the hiccup is highly likely to only be temporary.

After Mitek became profitable on an EBIT basis in FY2015, the company has achieved an EBIT margin slightly above ten percent in most years. Currently, Mitek’s trailing EBIT margin stands at 11.9%, quite near the company’s average of 9.6% since it became profitable. I believe that Mitek has potential for a significantly larger EBIT margin, though – the company’s trailing gross margin is 86.7%, providing room for margin expansion as Mitek’s SaaS revenues scale up.

Valuation

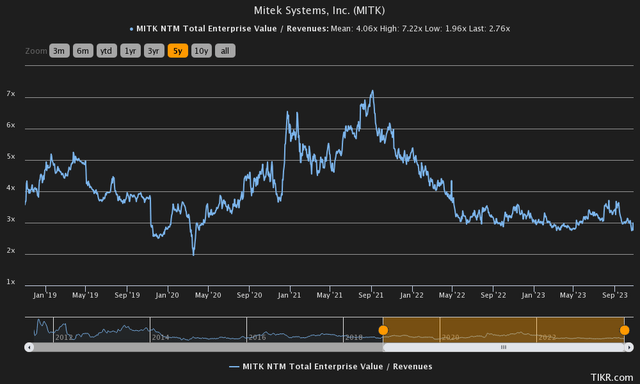

Mitek currently trades at a forward EV/S of 2.8, 32% below the company’s five-year average of 4.1:

Historical Forward EV/S (TIKR)

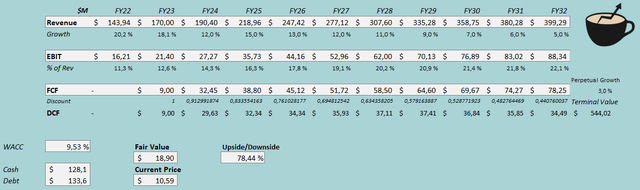

An EV/S ratio alone isn’t a very good indicator of a company’s valuation, as companies have different growth rates, cash flow margins, and risk profiles. To estimate a rough fair value for the stock, I constructed a discounted cash flow model as usual. In the model, I estimate Mitek to hit its current year revenue guidance with a growth of 18.1%. After the year, I estimate a growth of 12% for FY2024 – I believe that Mitek can achieve a higher growth in a normal market, but the market conditions for the identity verification segment could stay soft for a part of the year. After FY2024, I estimate the growth to accelerate into 15%, but to start slowing down in steps into a perpetual growth rate of 3%. The estimated growth represents a CAGR of 10.7% from FY2022 to FY2032.

I estimate Mitek to achieve significant operating leverage. I estimate an EBIT margin of 12.6% for FY2023, 1.3 percentage points above the achieved FY2022 level. After the year, I estimate similar margin expansion in the future; eventually, I estimate the EBIT margin to reach a level of 22.1%. I believe that the estimated margin is very possible because of Mitek’s incredibly high gross margin SaaS revenues. Mitek has a very good cash flow conversion as the company’s GAAP earnings include a large amount of amortization and depreciation, combined with a very low need for capital expenditures.

The mentioned estimates along with a weighed average cost of capital of 9.53% craft the following DCF model with a fair value estimate of $18.90, an incredible 78% above the price of $10.59 at the time of writing – if my estimates for growth and margin expansion hold water, the company is significantly undervalued:

DCF Model (Author’s Calculation)

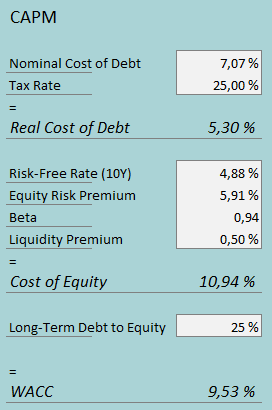

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In Q2, Mitek had $2.4 million in interest expenses. With the company’s interest-bearing debts, Mitek’s interest rate comes up to an annualized figure of 7.07%. Mitek uses a good amount of debt in the company’s financing; I estimate a long-term debt-to-equity ratio of 25% for Mitek.

On the cost of equity side, I use the United States’ 10-year bond yield of 4.88% as the risk-free rate. The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the US, made in July. Tikr estimates Mitek’s beta to be 0.94. Finally, I add a small liquidity premium of 0.5%, crafting a cost of equity of 10.94% and a WACC of 9.53%, used in the DCF model.

Takeaway

Mitek operates in a growing industry with an offering that seems to be competitive within the market. The company has achieved a high amount of growth in the medium- to long-term history. Although the company is facing a current hiccup in revenue growth that the company’s CEO indirectly attributes to the macroeconomic situation, I believe the long-term growth story still stands. In addition, the valuation seems to be highly attractive as my DCF model estimates an upside of 78%. If Mitek’s offering continues to stay as competitive, I believe that the investment could be very fruitful.

Read the full article here