Investment Thesis

Although often overlooked in comparison to Tesla, Inc. (TSLA) and BYD Company Limited (OTCPK:BYDDF), Li Auto Inc. (NASDAQ:LI) has emerged as one of the leading competitors in the Chinese landscape of battery-electric vehicles (BEVs) and, most recently, all-electric vehicles (EVs). Li Auto’s strategy is quite different from its competitors, offering hybrid engines in China to reduce range anxiety along with the ability to travel long distances across China.

Unlike other competitors that have chosen to sell on volume and compete primarily on cost, such as BYD and Tesla, the company seems to have found a good fit in the premium EV market. In our last review of Li Auto, we actually assigned a buy rating near the bottom at $18, after which the company rose an astonishing 67.24%, as opposed to 29.21% for the S&P 500, even despite the terrible performance of Chinese equities. Yet we think the stock is still trading below its intrinsic value after the run-up, leaving room for growth as it is overlooked by the economic chaos in China and the focus which is mainly geared towards competitors, whose fundamentals are headed south.

Notable Outperformance

Since we first looked at Li Auto in 2022, we have been pleasantly surprised by the outperformance it has shown as an underdog in a serious competitive environment with Tesla, BYD, and a host of legacy automakers. Our two assumptions of US$19.12BN in revenues by 2024 and EBITDA margins of 4.9% have arguably been exceeded even before the year began.

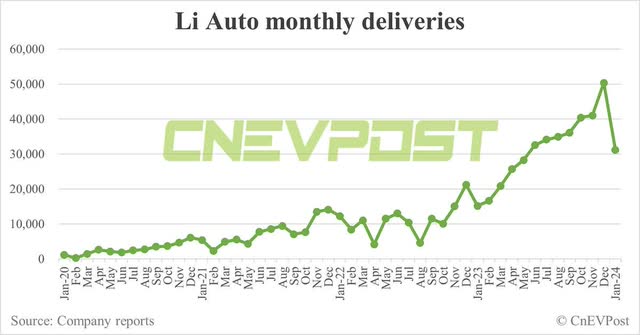

Revenues for the third quarter were US$4.75 billion or US$19 billion annualized, up 271.2% YoY and up 21.0% from the second quarter. Gross margins came in at a stable 22.0% and operating margins rose to an impressive 6.7%. Many of these improved figures were due to deliveries of models introduced after the Li One, namely the Li L7, Li L8, and Li L9. As a result, orders grew from about 10K per month in 2022 to a record high of 50K in December. The delivery numbers for January were a lot lower, but that is also to be expected due to seasonal factors such as the Chinese Lunar New Year and the year-end deliveries being pushed out in December.

CnEVPost

Li Auto also has its first all-electric multipurpose vehicle on the way, the “Li Mega,” which was recently delayed for a few months but is still set to launch very soon on March 1 with deliveries beginning in early March. Besides the production challenges Li Auto is facing, the management team still believes it will become the best-selling EV in the category above 500K Yuan ($70.36K).

With the EV’s official price expected to be under 600K Yuan ($84.43K), it is definitely in the higher price range for China. We also reckon they will face stiff competition from the recently launched XPeng X9. Both vehicles have a range of approx. 700 km and a 370 kW engine for the X9 AWD Performance model versus a 400 kW engine for the Li Mega. The X9, for example, is currently in the price range of $50K-$60K, meaning that the AWD Performance version is nearly 30% cheaper than the current $84.43K outlined price cap for the Li Mega, despite the fact that a lot of the specifications are pretty similar.

In addition to the Li Mega, the company also announced that its next BEV model, the Li L6, will be launched in the first half of this year, along with three other BEV models launching in the second half of the year. We see these factors as a short-term headwind, along with the current ramping of the Li Mega, which management expects will also be a short-term headwind to gross margins.

Operational Leverage

Another aspect that we apparently estimated correctly was Li Auto’s ability to exert operating leverage, as we believed that operating expenses would not scale linearly with revenues, but rather would decline relative to revenues as the product line became more saturated. We saw this same effect happen at Tesla, where operating expenses remained relatively flat while revenues continued to scale linearly.

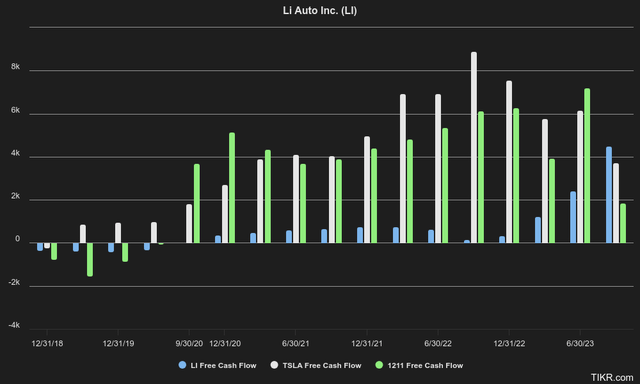

Li Auto’s bottom-line results actually surprised us quite a bit. To emphasize how big a difference it is from other major EV manufacturers: Li Auto currently pulls more free cash flow on a 12-month basis than Tesla and BYD. And the most amazing fact is that Tesla has a market cap of over $580 billion and BYD is standing at $71.54 billion, while Li Auto only has a market cap of $32.29 billion. In short, Li Auto’s free cash flow increased from less than $1BN to more than $4.49BN, while Tesla and BYD’s free cash flow actually decreased.

TIKR Terminal

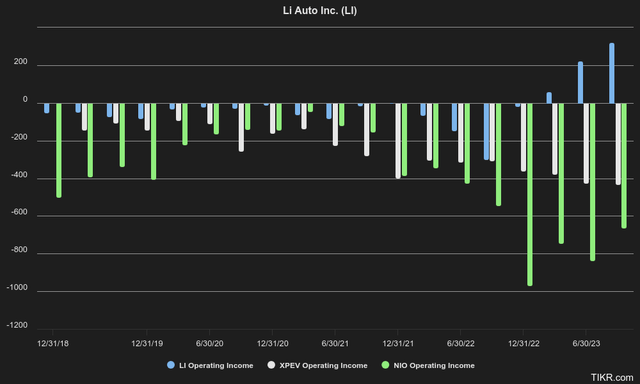

So not only does Li Auto prevail on some key fundamentals against major EV manufacturers, it is also one of the few truly profitable manufacturers when looking at direct competitors. Last time we looked at Li Auto, it looked like they were in the same boat as other premium EV manufacturers on a smaller scale, such as XPeng Inc. (XPEV) and NIO Inc. (NIO). They still had negative operating results in the same way as the other players, but that changed in 2022. And today, while both other players are still struggling from an operational perspective, Li Auto has become operationally profitable in the last few quarters.

TIKR Terminal

One might wonder why Li Auto is not even trading close to Tesla at a $580 billion valuation, despite the fact that the company has recently surpassed them in FCF generation. After all, Li Auto’s sales figures still indicate double-digit growth, and like Tesla in the United States, Li Auto is also heavily involved in developing autonomous driving technologies in China.

In addition, management has stated that a future goal is to keep gross margins above the current 20%, which is also on par with BYD and Tesla’s gross margins. For a healthy and growing company like this, it would be reasonable to grant an FCF multiple of 18x. In which case Li Auto would be worth much more than it is now, but we have not yet taken into account the current risks surrounding China.

The China Factor

China is currently facing a number of serious problems, which we will not go into in-depth since this is an article on Li Auto and not macroeconomics. But as we have pointed out in previous articles, the country is facing problems, from an inflated housing market to economic instability, debt problems, and possibly an upcoming demographic problem as well.

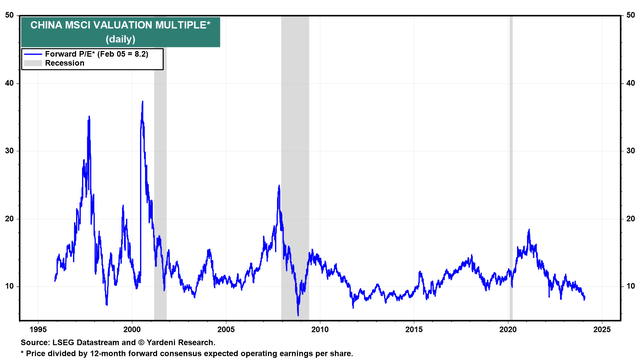

Like many other emerging markets, this is one reason why Chinese stocks have always traded at a discount to the United States. But contrary to others, we don’t think that makes them uninvestable. The Chinese stock market is also very different from that in the United States, where the market is pretty much institutionalized with big banks and asset managers like BlackRock and Vanguard and a large majority of people automatically setting aside money through 401Ks and Roth IRAs to invest in equities. In China, the landscape is very different. Not many citizens own stocks and prefer real estate, which also partially explains the bloated real estate market.

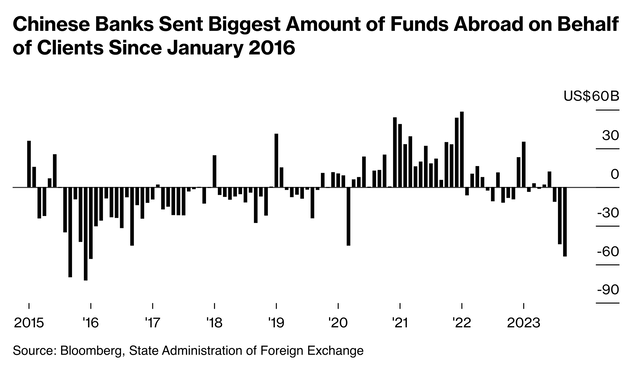

Something else that not many analysts talk about is the fact that there is a shadow factor of capital flight in China that the government is trying to minimize. Given all the problems with economic instability, especially now with real estate, it is perhaps no surprise that domestic citizens are mostly reluctant to have all of their capital tied up in Chinese banks and prefer to have it abroad, in countries like the U.S. or in real estate. China is somewhat less favorable in terms of economic freedom and politics compared to the US.

That doesn’t make things any easier, as domestic investors also don’t seem particularly willing or able to pull the stock market out of its all-time lows. Fortunately, earlier this week it looks like the Chinese government was willing to step in and stabilize the market.

Bloomberg

This came in the form of reports that China’s sovereign wealth fund came out with news telling investors that they would increase their stake in ETFs. Which is somewhat baffling because many Chinese ADRs like Alibaba Group Holding Limited (BABA) and JD.com, Inc. (JD) are sitting on big piles of liquid assets and presumably could have provided some stabilization by returning capital to investors, buying back more shares or paying decent dividends. Which they didn’t do, as they waited for government intervention. But then the issue goes back to capital flight, with the Chinese Communist Party perhaps preferring to keep capital in domestic firms rather than returning it to investors, to limit capital flight from China.

In conclusion, if we consider this “China factor” because of the above risks and use a lower multiple at which Chinese stocks have historically been valued, we believe there is still value to be found in Li Auto. For example, if Li Auto were trading at 10x free cash flow, that would be more than reasonable given the company’s competitive position and growth. At this 10x P/FCF ratio with $4.49BN of FCF, we expect Li Auto to have fair value at a market capitalization of $44.9BN or $42.37 per share.

Yardeni Research

The Bottom Line

Some believe that China is a value trap and uninvestable, or that it is headed for economic destruction. We, on the other hand, believe there is value to be found in certain names, including Li Auto. Taking into account the economic situation, we still see an upside of $42 per share, even at a valuation of a lower multiple.

The government also stepped in with their sovereign wealth fund and showed their commitment to other programs to protect domestic and foreign investors by trying to put a floor in Chinese stocks at extremely historically cheap valuations. Regarding all the BEV/EV manufacturers, we see Li Auto being overlooked by investors as we believe it’s flying under the radar, while much attention is focused on larger players such as Tesla and BYD or even competitors such as NIO and XPeng.

Therefore, we maintain our Buy rating, with our view that Li Auto is still trading below intrinsic value, which we see closer to $42 per share.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here