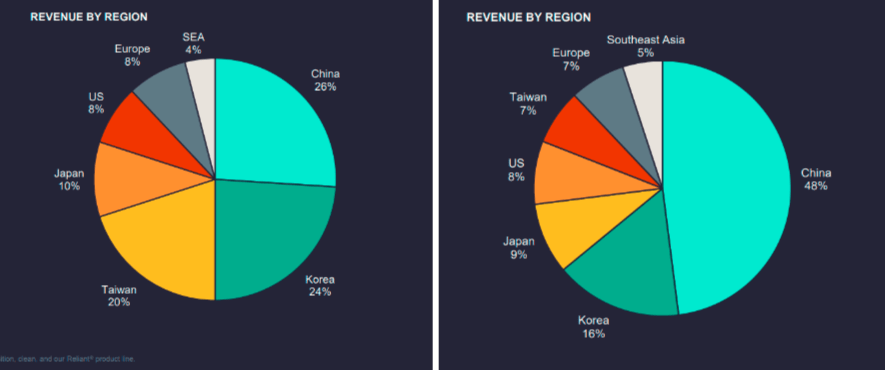

We remain hold-rated on Lam Research (NASDAQ:LRCX). Consistent with our expectations last quarter, LRCX, alongside the broader semi-cap, is experiencing increased Chinese demand due to panic buying from Chinese customers out of fears of the Biden administration expanding its export ban on semiconductors. The Chinese concern is well placed, in our opinion; Washington announced new rules to the ban this week limiting the sale of A.I.-related chips to China, including Nvidia’s (NVDA) A800 and H800. This September quarter, shipments to Chinese customers grew 100% QoQ, accounting for 48% of total sales, up from 26% last quarter. The following graph outlines revenue by region for the September quarter and June quarter.

LRCX earning results

While the higher Chinese demand offsets the weaker end demand from customers from all other geographies, we think this demand is not a sustainable growth driver. We now think it’ll be until 2H24 for the memory and foundry capex spending to rebound, and we don’t expect LRCX to experience financial outperformance ahead of the capex rebound. The stock is down 5% since our downgrade to hold, relatively in line with the S&P 500. We don’t see the stock working in the near term and see a higher risk profile from Chinese sale exposure and the muted near-term spending environment.

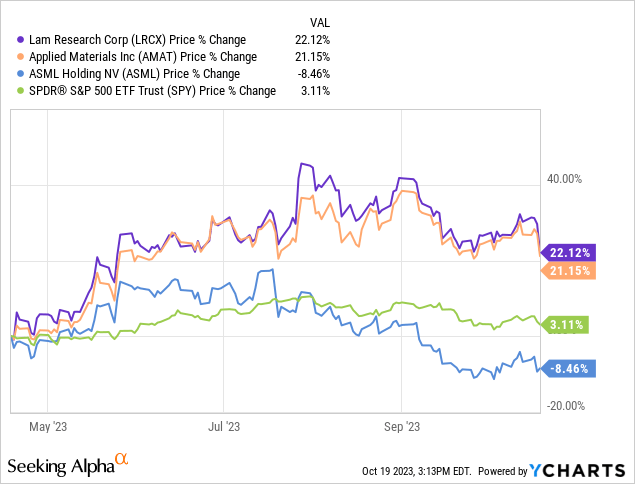

The following graph outlines LRCX’s stock performance against the S&P 500 and semi-cap ASML (ASML) and Applied Materials (AMAT).

YCharts

Valuation

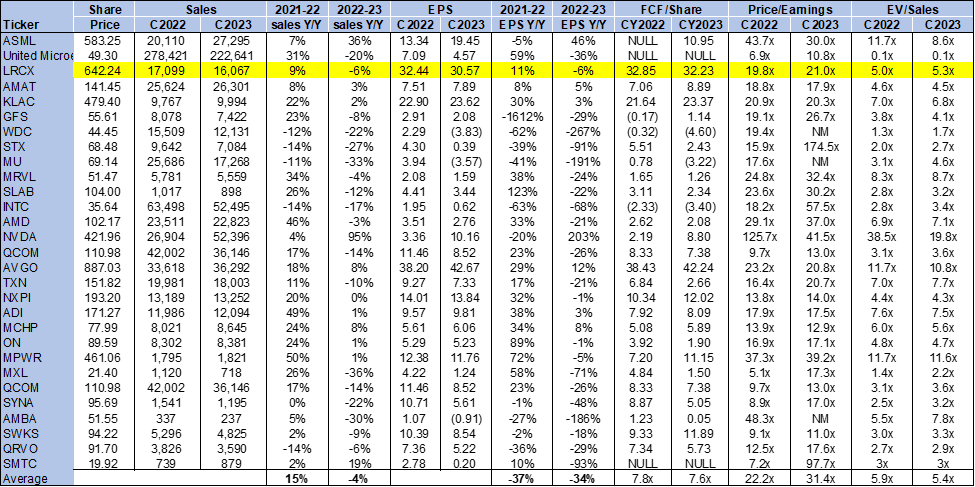

The stock is fairly valued, in our opinion, but we don’t recommend investors buy the stock at current levels as we don’t see it working in the near term. On a P/E basis, the stock is trading at 21.0x C2023 EPS $30.57 compared to the peer group average of 31.4x. The stock is trading at 5.3x EV/C2023 Sales versus the peer group average of 5.4x. The following chart outlines LRCX’s valuation against the peer group.

TSP

Word on Wall Street

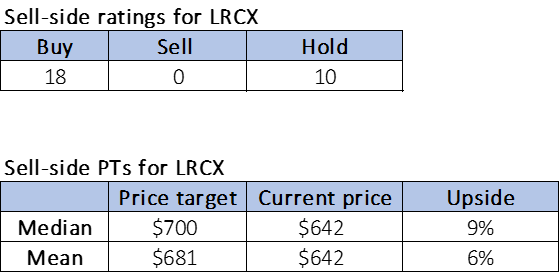

Wall Street is bullish on the stock. Of the 28 analysts covering the stock, 18 are buy-rated on the stock, and the remaining are hold-rated. We attribute Wall Street’s sentiment to LRCX’s longer-term position as etch and deposition complexity increases to match more advanced tech. We’re bullish on LRCX in the longer term as we expect the company to be well-positioned to benefit from the transition to next-gen 3D NAND and future-gen DRAM. The median sell-side price target is $700, while the mean is $681, with a potential upside of 6-9%.

The following charts outline sell-side ratings and price targets for LRCX.

TSP

What to do with the stock

We maintain our hold rating on LRCX. We continue to be cautious about the semi-cap space in the near term. We think the company is at higher risk due to exposure from Chinese sales as the Biden administration’s ban expands. We don’t see a near-term catalyst to drive end demand recovery, and the memory spend continues to be muted in the near term. We now expect memory and foundry capex rebound to occur in mid-2024, not ahead. We recommend investors stay on the sidelines.

Our investing group, Tech Contrarians, discussed this idea in more depth alongside the broader industry and macro trends. We cover the tech industry from the industry-first approach, sifting through market noise to capture outperformers.

Feel free to test the service on a free two-week trial today.

Read the full article here