A Hold Rating for Ivanhoe Mines

This analysis recommends maintaining the Hold rating on Ivanhoe Mines (OTCQX:IVPAF) (TSX:IVN:CA) shares already given in this previous analysis.

At the time of the previous analysis, the stock was believed to be well-positioned to benefit from copper’s bright future as a key element in clean energy transition projects through increasing adoption of electrification. Many analysts are trying to estimate how much the copper market could be affected by this new trend, which has gained a lot of momentum recently as information creates an urgent need to address carbon emissions or the cause of extreme effects of climate change. There is no consensus among analysts on the growth trends, which vary widely between reports, but one thing is certain: the market will experience a rapid recovery. Ultimately, copper is the preferred element in the manufacture of electrical connectors and systems due to its very good electrical and thermal conductivity. The production of copper will be boosted by government incentives to make this post-industrial society greener and greener.

Ivanhoe Mines fits into this very favorable context as follows: the company is working to increase copper production and further develop other productions, not only of copper but also of other key elements for the planet’s energy future, such as zinc.

There is no doubt that copper, with its robust price conditions seen over the medium and long term, creates a very favorable environment for Ivanhoe Mines to implement its growth plans. However, the Hold rating was assigned on the basis that the Federal Reserve’s restrictive interest rate policy continued to invalidate any project of recovery in the stock price of Ivanhoe Mines. Because high financing costs in the eyes of market participants are difficult to reconcile with the demand for copper; thus, the market reassesses the value of the US-listed shares of copper producers and developers downwards, and the resulting backlash cannot spare Ivanhoe Mines shares either.

Shares May Still Face Downward Pressure, Sliding Near-Term Recovery Opportunities

The higher cost of capital (fixed-rate mortgage interest rates at their highest level in 20 years) combined with elevated core inflation (currently at 4.1% versus the target of 2%) really can’t support consumption, and since copper is used to make many everyday products that people buy, there’s currently no need to stock that much copper at U.S. goods manufacturers, among other things grappling with a contraction in new orders.

This dynamic therefore creates downward pressure on Ivanhoe Mines’ share price as copper is the company’s primary source of income.

Investments in economic activities also continue to be seriously affected by costly credit, the loopholes of which have become even smaller after the crisis that affected US regional banks in the spring of 2023.

Investments in the exploration and development of copper deposits are not exempt from this problem. Although Ivanhoe Mines’ balance sheet has probably a lower need for debt to fund growth compared to many other operators (the projects are implemented through joint ventures with the participation of governments), the negative impact of tighter credit conditions is also being felt on Ivanhoe’s shares. If there is no rational response, this is inevitably the case as the market takes the baby out with the bathwater.

The Shares Could Be Cheaper than in the Previous Analysis, but the Stance Remains on “Hold”

And then, as the company continued to work on its mining and metallurgy projects, a -3.16% decline in copper futures sent Ivanhoe Mines shares below the levels prevailing at the time of the previous analysis amid high borrowing costs and elevated core inflation.

The Joint Venture company is making progress in expanding copper ore milling capacity at the Congolese Kamoa-Kakula plant (October 2024 target: from about 9-10 million to 14 million tonnes of copper ore per year) and with the project to establish another production but of zinc at another Congolese mining site in Kipushi by summer 2024. Given the increased growth prospects triggered by operational improvements, the stock must logically have become even cheaper.

However, this is not yet enough to revise the Hold rating on Ivanhoe Mines shares upwards, as the Fed’s “longer for higher” interest rate policy coupled with elevated core inflation will likely create further headwinds for Ivanhoe Mines shares. These two main macroeconomic issues are pushing the economy into a recession which many economists have already predicted so far this year.

The voice of Luke Tilley, Chief Economist at Wilmington Trust, recently joined the chorus of recessionary economists when he argued that the US economy is not improving but instead slowing at a rate that will soon be impossible to ignore.

Taking into account the volatility characteristic of the copper price, which does not develop steadily, but through cyclical fluctuations, the principle of inertia will mean that Ivanhoe Mines’ shares can still rise somewhat despite the negative winds described. However, it must be added that concerns about the aftermath of the economic recession will tend to stifle the ability of copper prices to recover in a convincing manner, so the appointment of a new strong up-cycle for Ivanhoe Mines shares will probably be postponed and therefore there is no reason to raise the Hold rating today.

The Hold rating on Ivanhoe Mines shares has been reaffirmed to avoid losing ground on the rosy copper outlook as the company continues to lay the foundation for business growth following progress in the third quarter of 2023.

About the Congolese Kamoa-Kakula Copper Complex in the Third Quarter of 2023: its Current Size, and Comparisons with Peers

For a geolocation of Ivanhoe Mine’s mining operations and the risk of operating in Congo, see previous analysis.

The Q3 2023 report shows that Kamoa-Kakula believes the near-term future of the company in terms of costs and production is as follows:

For all of 2023, the Kamoa-Kakula complex forecasts cash costs to remain flat at CA$1.40 to CA$1.50 per pound (or $1.01 to $1.09 as of this writing), while production of the red metal is expected to fluctuate between the lower bound of 390,000 tons and the upper bound of 430,000 tons.

The cost numbers are actually very competitive compared to two of Ivanhoe Mine’s closest peers and the company is working on mineral and metallurgical projects to better align production with the competition in the near future:

In terms of cash costs, Phoenix, AZ-based Southern Copper Corporation’s (SCCO) business was at $2.02 per pound in 2022, while Vancouver, B.C.-based Brazilian copper producer Ero Copper Corp. (ERO:CA) incurred $1.82 per pound due to its operations in Q3-2023.

Currently, the Kamoa-Kakula complex is still well below Southern Copper’s 2022 copper production of 894,700 tonnes, but beats Lundin Mining Corporation (LUN:CA) (OTCPK:LUNMF) as the Toronto-based producer of copper mines 283,300 tonnes of attributable metal on an annual basis from the 3rd quarter of 2023. Instead, Ero Copper is lagging far behind and expects 44,000 to 47,000 tons of copper for the full year 2023.

However, as far as the third quarter of 2023 is concerned, production from the Kamoa-Kakula mine in Congo is performing very well as it reached a production record of 103,947 tonnes of copper in concentrate, up 0.2% quarter-on-quarter and up 6.3% year-on-year.

The amount of payable copper tons of Kamoa-Kakula sold in the market was 96,509 tons in the third quarter of 2023, a slight decrease of 4.9% compared to the previous quarter, but an increase of 2.9% year-on-year.

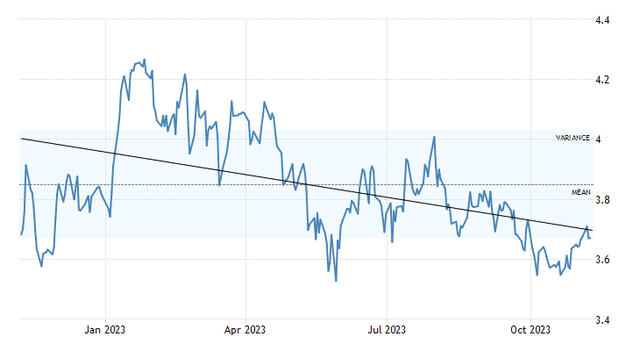

The higher sales volumes were achieved during a period when the copper price provided a significantly more favorable environment compared to the prior year (averaging $3.79/lb for Q3 2023 compared to an average of $3.51/lb for Q3 2022), resulting in higher sales and profit.

Kamoa-Kakula’s third-quarter 2023 GAAP EPS was C$0.08 (or $0.06), on a nearly 51% year-over-year increase in revenue to C$694.84 million (or $514.60 million). The 68.6% year-over-year increase in EBITDA to C$423.21 million (or $313.43 million) in the third quarter of 2023 resulted in an EBITDA margin of 61% versus an EBITDA margin of 55% in the third quarter of 2022.

Ivanhoe’s Partnership in the Congolese Complex: Current Copper Prices Call into Question the Financial Position, but Investors Should Not Worry

The retail investor must know that the Kamoa-Kakula copper mining complex in Congo is not 100% owned by Ivanhoe Mine but belongs to the Kamoa-Kakula Holding Joint Venture. Therefore, Ivanhoe Mine, which holds 39.6% of the JV company, shares the company’s profits with its partners Zijin Mining Group Company Limited (OTCPK:ZIJMF) (OTCPK:ZIJMY), Crystal River Global Limited and the Government of the Democratic Republic of Congo, who are holding the remainders 39.6%, 0.8%, and 20%, respectively.

Ivanhoe Mines’ adjusted EBITDA for the third quarter of 2023 was CA$ 152 million ($112.57 million), compared to CA$ 85 million ($62.08 million) for the third quarter of 2022. On an adjusted basis and in U.S. currency terms, the EBITDA margin rate increased 860 basis points year-over-year to 55.2% in the third quarter of 2023.

Ivanhoe Mines underpins its participation in the joint venture with a balance sheet situation that at the end of the third quarter of 2023 objectively did not appear capable of ensuring financial solidity, should it become necessary to intervene in consultation with its partners to stimulate the growth projects currently underway.

It had cash and short-term securities of $303.3 million, against total debt of $644.5 million.

Additionally, the investment in copper and other base metals in Congo through the joint venture generated essentially an operating loss of $84.7 million versus an interest expense of $35.2 million on a trailing twelve-month basis through the third quarter of 2023. Furthermore, copper prices do not seem to be able to provide any meaningful help in reversing the trend between costs and returns.

In fact, for about three months, copper prices have been well below the average of the previous twelve months, during which it has not been possible to achieve the profitability required to cover the financial costs, and on top of this with the risk that the price of the red metal will continue to decline amid the challenging global macroeconomic and geopolitical situation.

Source: Trading Economics

However, Ivanhoe Mines believes that cash flow from the Kamoa-Kakula Phase 1 and Phase 2 expansion projects, as well as local financing opportunities, are sufficient to meet the capital cost requirements for the Phase 3 expansion, despite current copper prices.

On Track to Become a Major Copper Producer and Realize the Benefits of Copper as a Key Component of the Energy Transition

The Kamoa-Kakula Phase 1 and Phase 2 expansion projects were successfully completed in February 2023, with the debottlenecking program increasing the capacity of the concentrators to 9.2 million tonnes of copper ore per annum.

Phase 3 of the expansion project to process more than 14 million tonnes of copper ore, including a copper anode production capacity of 500,000 tonnes of copper per year, is expected to begin functioning within 12 months.

Then there is Phase 4, which involves the installation of another concentrator with a capacity of 5 million tons of copper ore per year and, according to the project, must bring the total capacity of the Kamoa-Kakula complex to well over 19 million tons per year, the second largest copper complex in the world according to the company’s plan. At that point, copper production in Congo should exceed 600,000 tons per year.

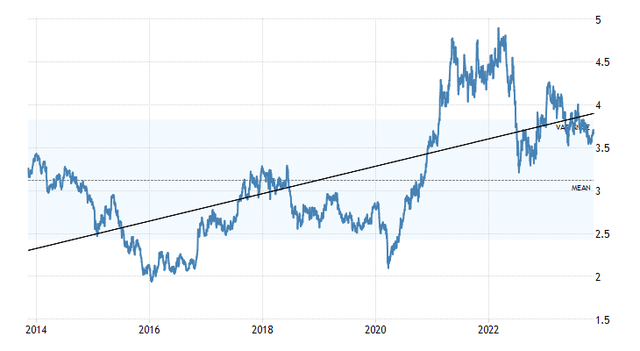

Copper prices proved crucial in boosting growth projects in Congo: The rush to build enough copper inventories amid fears that a strong recovery from COVID-19 restrictions would lead to dangerous shortages sent the metal’s price soaring to historic highs for an extended period of time.

Source: Trading Economics

The Kamoa-Kakula complex benefited enormously from the incredible rise in copper prices. It enabled employees to complete Phase 1 of the expansion project in July 2021, and the resulting cash flow from the expanded operations funded the completion of Phase 2 in April 2022, while copper prices remained at unprecedented levels.

The price of copper rebounded strongly again in early 2023 and despite the dramatic but temporary rise in energy prices in early summer 2022, there was momentum to move forward with Phase 3, which is now 60% complete.

The third concentrator plant is scheduled to be operational by the end of 2024. Due to the continued slowdown in core inflation combined with the rate cut as the Fed is expected to reverse its interest rate policy sometime next year, expectations for future copper demand will be much more optimistic, creating an ideal environment for strong copper prices.

In short, the Kamoa-Kakula complex appears to be well on its way to becoming one of the largest copper producers in the world.

Other Mineral Joint Venture Projects of Ivanhoe Mines in Congo and South Africa

The company is also involved in the Kipushi Mineral Project in Congo, where it is building a mine (50% complete in Q2 2023 and 62% complete in Q3 2023) that will produce primarily zinc and some copper using underground mining techniques.

The project is being implemented in a joint venture with the government of the Democratic Republic of the Congo through its state-owned company Gécamines SA.

Ivanhoe Mines owns 68%, Gécamines 32%.

Kipushi is expected to begin initial metal production from Congolese high-grade metal deposits for zinc production in the second quarter of 2024, and much of the necessary infrastructure is already in place.

The Kipushi Mineral Project in Congo is a primary zinc-producing mine with a mine life of 13.7 years and is expected to produce a total of 6.013 million tonnes of zinc or 437,000 tonnes of zinc per year over its life.

Ivanhoe Mines’ mining activities are also in South Africa, in an area approximately eight kilometers from Mokopane and approximately 280 kilometers northeast of Johannesburg, at the northern end of the South African bushland complex. The project is called Platreef, which Ivanhoe Mines would like to develop into a production and distribution of palladium, rhodium, and platinum as well as nickel, copper, and gold.

Construction of the Platreef Phase 1 mine is well underway. The first production is scheduled for the third quarter of 2024. The goal is to create 29 years of underground production of rhodium, palladium, platinum, and gold for a total of 15.149 million ounces or 522,000 ounces per year.

The project is a joint venture with the Black Economic Empowerment of South Africa, which owns 26%, and the Japanese trading and import/export company, ITOCHU Corporation (OTCPK:ITOCF), which owns 10%.

Ivanhoe Mines owns the remaining 64%.

The Stock Valuation: Shares Should Not Rebound for the Time Being

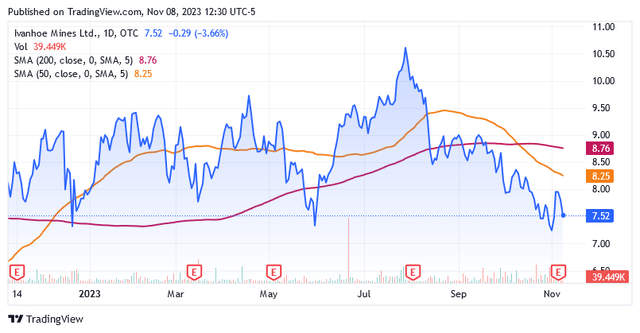

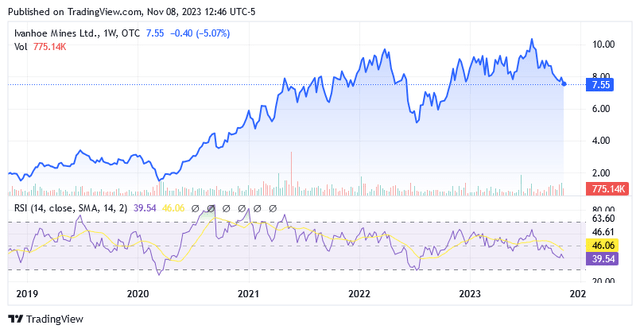

Shares of IVPAF were trading at $7.52 apiece as of this writing, giving it a market cap of $9.51 billion. Shares are trading below the 200-day simple moving average of $8.76 and below the 50-day simple moving average of $8.25.

Shares are unlikely to recover at this point rather could still decline somewhat due to continued negative pressure from higher borrowing costs and higher core inflation as these factors are seen to hurt copper demand.

Source: Seeking Alpha

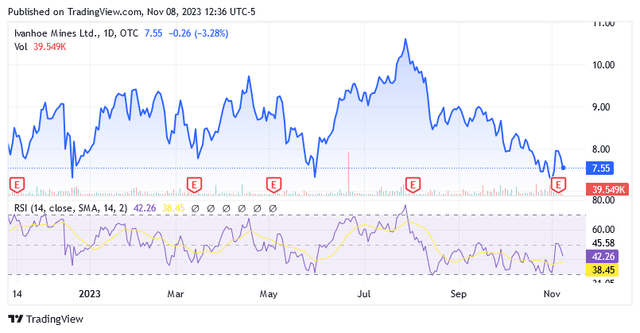

A 14-day relative strength indicator of 42.26x, still far from oversold levels, suggests there is still some room for shares to fall from current levels if they want to.

But as the unfriendly Fed interest rate policy of “higher and longer” has largely been priced into the share price, to cause a significant weakening in stock prices, another rate hike would be necessary.

Source: Seeking Alpha

But it is unlikely that the Fed will raise interest rates any further as the peak appears to have already been reached. The headwinds for Ivanhoe could really worsen in case of a downturn in the US economy, but the investor must not be intimidated and hold on stubbornly.

Why Investors Should Hold on Tenaciously in Case of a Recession

Shares have risen sharply since 2021, thanks to the boost Ivanhoe’s mineral and metallurgical expansion projects received from historically high copper prices between 2021 and 2022, amid strong recovery from COVID-19 and positive momentum from the resilience and recovery government programs.

Source: Seeking Alpha

It is clear that the market is now convinced that Ivanhoe Mines is well on its way to becoming a relevant producer of copper and establishing one of the largest copper production facilities in the Congo, whose extensive mineral resources attract the attention of large multinational companies, which in turn makes it easier to obtain the necessary financing. This now appears to be more of a stock to keep in the portfolio to continue to benefit from copper’s growth opportunities as part of the energy transition.

In such circumstances, sharp price declines, if they occur due to the economic recession, should not be viewed as a problem but rather welcomed as an opportunity to increase exposure to copper through Ivanhoe Mines.

The same considerations are applied to the stock traded on the Toronto Stock Exchange.

Shares of Ivanhoe Mines Ltd. under the TSX:IVN:CA symbol are trading at CA$10.40 apiece as of this writing, below the 200- and 50-day simple moving averages of CA$11.81, and CA$11.27, respectively. Shares are also trading below the middle point of CA$ 9.575 in the 52-week range of CA$ 9.88 to CA$ 14.01. The stock has a market cap of CA$ 6.70 billion.

The stock under the symbol TSX:IVN:CA has a 14-day Relative Strength Indicator of 42.75.

Conclusion

Ivanhoe Mines is a Canadian company that aims to significantly increase copper production and be better equipped to meet the demand of the global market, which is expected to grow as copper is fundamental in energy transition projects.

The company operates in the Democratic Republic of Congo, a country very rich in key elements for the energy transition program and therefore attracting the interest of large capitalists and financial institutions.

Ivanhoe, whose growth plans saw a turning point thanks to the historic peak reached by copper with the strong recovery from the pandemic, is now well-positioned to benefit amazingly from the evolving environment.

While Ivanhoe is about to build one of the world’s largest copper production and processing facilities in Congo, the company is also involved in a zinc production project that will start in Congo in about a year and precious metals development activities in South Africa, through joint ventures with local authorities and the government. Of course, these partnerships increase the chance of successful completion of the projects.

Shares could trade a bit lower in the coming weeks due to negative pressure from higher borrowing costs and increased core inflation hurting demand for copper. However, investors should stick to a “Hold” rating for the time being. There may be price opportunities in 2024 that can be used to expand the position.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here