Iris Energy Update:

Iris Energy (NASDAQ:IREN) reported FY 2023 results for the period ending June 30 last night. There was a lot of new information to digest that was available at the time of my last writing, “Iris Energy: Nvidia Chip Purchase Signifies Entry into AI/High Performance Computing Space”. All of earning information plus the conference call reinforced my conviction that $8, the low end of sell-side estimates, is an attractive and possibly conservative target. Profitability for the year ending in June was not tremendously material, as the thesis is based on what the business does going forward. That said, profitability since the last balance sheet update in June is excellent.

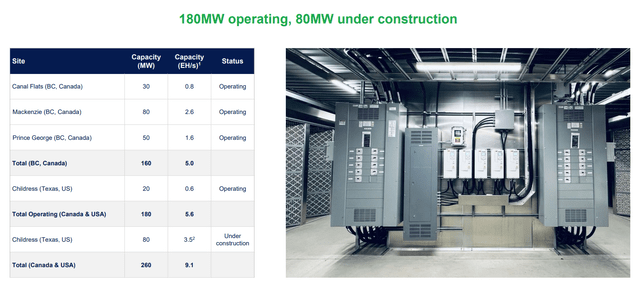

The company ended June with ~$69 million of cash, versus the June update that stated there was $64 million in the bank as of the end of May. Part of the cash likely stems from an at the money program, and part is from bitcoin mining. While the bitcoin mining segment overall was less profitable in ’23 versus ’22 owing to lower bitcoin prices and energy costs per bitcoin (BTC-USD) mined that increased 35% year over year, the company outlined its advantaged energy position as the Childress, Texas facility becomes a bigger portion of exa hash base.

Iris Energy Hash Rate by Facility (FY 2023 Presentation)

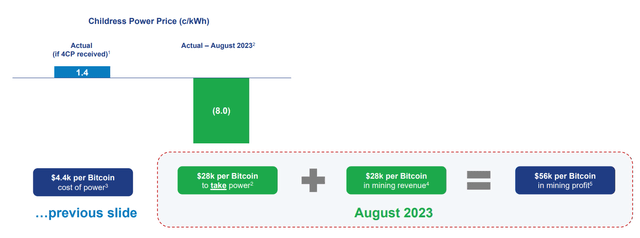

Thanks to its access to cheap power and spikes in Texas power prices, which allows the company to participate in emergency energy response (throttling down energy usage at peak periods and sending into the grid), the company’s energy costs at Childress are $.020/kWh. That’s about half the company’s costs in Canada, which are considered relatively low.

There are further potential savings as the company should soon be able to participate in the 4CP (Four Coincident Peak) programs in Texas (more about that program here). Full 4CP participation would lower the company’s cost to $.014/kWh.

The company was able to monetize this cheap power in August, which allowed it to double its profitability for the month.

Iris Energy Childress Power Costs (FY 2023 Presentation)

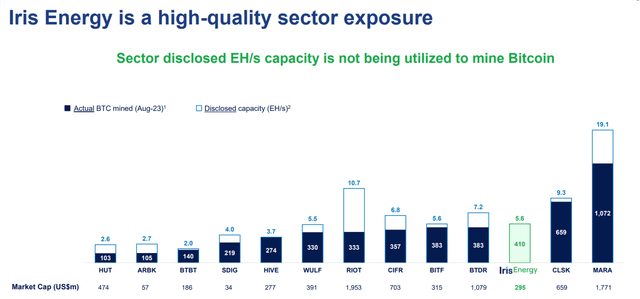

The company continues to fund its buildout at Childress. Remember, it expects to be a 9.1 exa hash by early 2024 and believes it has an eventual capacity of 30 eh/s. Just getting to 9.1 puts these guys in the big leagues, as represented by the bar chart below.

Mining Industry Hash Rash and Market Caps (FY 2023 Presentation)

The AI/HPC Initiative:

Much of the conference call, particularly the question and answer session, was dedicated to the AI/HPC initiative. Remember, the company announced in August that it purchased 248 Nvidia chips for $10 million that it expects to install at Childress. The chips should be delivered in the coming months, and the company said it is in negotiation for customers needing HPC computing capacity.

Referring back to my notes from the Piper Sandler conference last week, most data center companies cannot just install AI/HPC capacity in existing facilities. They need more power and other infrastructure not available in older facilities without significant upgrades. Childress is a new facility that the company has designed with AI/HPC in mind, and as stated above, it has about the cheapest power available.

Valuation:

Even not counting the excess energy profits from August, I believe that the company is operating at a run rate of over $50 million of EBITDA. With a market cap of $345 million (stock at $5.15), $70 million of cash, and no debt, that leaves the company trading at 5.5x just its bitcoin mining EBITDA with no consideration for the energy optionality, the bitcoin capacity expansion, or the Ai/HPC initiative. As you can see in the bar chart above, that valuation leaves it at a huge market cap discount to other miners, judging by bitcoin mining capacity alone. All of the company’s other merits are freebies. I continue to think the stock has an upside to at least the high single digits, if not low double digits.

Risks:

The primary risk is the price of bitcoin. I think the energy optionality and the AI/HPC initiative can minimize that risk, but if Bitcoin comes off, this stock will come off with it…at least until the AI/HPC initiative becomes larger.

Conclusion:

As I’ve said before, I believe most businesses in the bitcoin universe are garbage, with bad business models, and worse management teams and balance sheets. IREN is one company I can get extremely comfortable with. It is the one company I want to own in the space. Those who share my skepticism on Coinbase (COIN) and MicroStrategy (MSTR) can hedge their short bets on those with a long in IREN. I also think it’s a good long on its own merit for those who can handle the volatility and bitcoin pricing risk.

Read the full article here