At a Glance

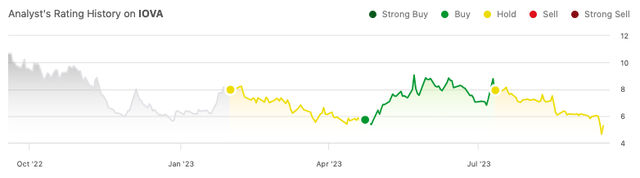

Navigating through regulatory delays and internal investment shifts, Iovance Biotherapeutics (NASDAQ:IOVA) continues to position itself as a frontrunner in T-cell therapies for solid tumors. Since my last “Hold” recommendation, the FDA’s extension of lifileucel’s Priority Review to February 2024 signaled not a roadblock but a procedural hiccup. This delay, paradoxically, may provide time for further fine-tuning of its market strategy, already underscored by significant Authorized Treatment Centers (ATC) investments and payer engagements. Insider confidence is palpable, with a recent $25M share acquisition by an Iovance director, boosting stock value. With a cash runway now extended to approximately 13.1 months after a capital infusion, I am upgrading my stance to “Buy.”

Seeking Alpha

Q2 Earnings Report

To begin my analysis, looking at Iovance’s most recent earnings report, the most striking metrics are the increase in Research and Development (R&D) expenses to $86.3M for Q2 2023, up $12.9M from $73.4M in Q2 2022. This uptick can be largely attributed to the growth of internal R&D teams and elevated costs associated with the Phase 3 TILVANCE trial. Concurrently, Selling, General and Administrative (SG&A) expenses have dipped to $21.9M, a decrease of $4.4M YoY, largely due to capitalization of expenses post-Proleukin acquisition. Revenue remains almost negligible at $0.2M, owing to product sales following the Proleukin acquisition. The net loss has widened to $106.5M from $99.3M YoY. These metrics indicate that Iovance is strategically investing more into its pipeline while managing SG&A expenses, a sign of disciplined financial and operational maturity as it advances its clinical programs.

Cash Runway & Liquidity

Turning to Iovance’s balance sheet, as of June 30, 2023, the company holds Cash and Cash Equivalents of $230.0M and Short-term Investments of $20.9M, totaling $250.9M in highly liquid assets. Factoring in the recent capital infusion of $172.5M from a share offering in July, the updated liquidity position escalates to $423.4M. Over the last six months, Iovance reported a Net Cash Used in Operating Activities of $193.8M, translating to a monthly cash burn rate of roughly $32.3M. With the additional capital, the cash runway extends to approximately 13.1 months. It’s worth noting that these calculations are predicated on historical figures and may not be indicative of future performance.

In light of the recent capital raise, the company appears to be in a strengthened liquidity position. Iovance’s current liabilities total $88.6M, and it holds a nominal long-term note payable of $1.0M. Non-current operating lease liabilities are at $68.8M. The positive influx of $259.2M from financing activities over the last six months, inclusive of the recent $172.5M, provides a cushion that not only extends the cash runway but also may instill investor confidence despite the ongoing negative cash flow from operations.

Capital Structure, Growth, & Momentum

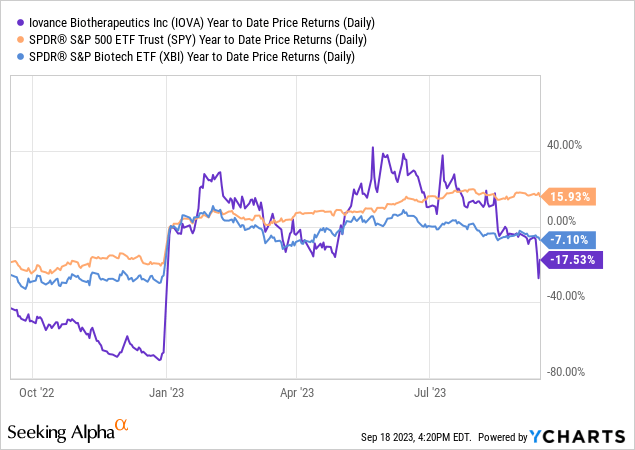

According to Seeking Alpha data, Iovance shows a moderate level of debt against a market capitalization of $1.31B, mitigated by a healthy cash reserve. In terms of growth, the company is in a clinical phase but expects a revenue surge from $12.79M in 2023 to $539.79M by 2025, echoing its high-potential pipeline focused on T-cell therapies for solid tumors. The stock underperformed over the past year with a -55.60% return, significantly lagging behind the S&P 500.

Iovance: Delayed, Not Derailed, by FDA

Iovance appears to be in a robust position both commercially and from a regulatory standpoint concerning lifileucel, its pioneering TIL therapy for advanced melanoma and additional solid tumors. Despite the FDA’s extension of the PDUFA date, the absence of major review issues coupled with successful pre-approval inspections suggest the delay is due to resource constraints rather than scientific setbacks. The therapy continues to enjoy Priority Review status, and a Phase 3 confirmatory trial (TILVANCE-301) remains on track, fortifying its regulatory standing.

Simultaneously, Iovance’s recent earnings call showcased a strong commercial launch strategy. The company aims to onboard 40 ATCs within the first 90 days post-approval. These ATCs are not mere placeholders; they are making significant investments in operationalizing TIL service lines and express high enthusiasm for lifileucel. On the market access side, engagement with key national and regional payers is ongoing, and pre-existing reimbursement avenues for Medicare patients further de-risk the commercial strategy. Positive feedback from ATCs on Iovance’s care enrollment system adds another layer of assurance for a seamless launch.

In summary, the administrative delay in FDA approval presents an opportunity rather than a setback for Iovance. The additional time can be used to refine its already well-planned market access and payer engagement strategies, while the compelling clinical data and unique therapeutic profile of lifileucel minimize any long-term financial or competitive risks. Given these factors, Iovance stands well-prepared to rapidly serve the advanced melanoma patient community immediately following FDA approval.

My Analysis & Recommendation

In conclusion, Iovance Biotherapeutics appears primed for a turning point in its trajectory. The regulatory outlook for its flagship product, lifileucel, remains promising despite the FDA’s extension of the Priority Review date. The delay seems procedural, not scientific, alleviating concerns over potential roadblocks in the product’s clinical efficacy. Adding credence to this perspective is the substantial insider buying, signaling confidence in the firm’s prospects.

Investors should pay attention to several key aspects in the coming weeks and months. First, keep a close eye on updates concerning the expedited review; any favorable decision from the FDA would serve as a powerful catalyst for stock valuation. Second, the company’s beefed-up liquidity position to $423.4M enhances its risk profile, especially when balanced against its monthly burn rate, ensuring it has enough runway to negotiate further operational or regulatory hurdles.

However, while the future of lifileucel looks optimistic, challenges will undoubtedly surface upon approval. The immediate concern would be clinician adoption. As we are dealing with a novel form of autologous T-cell therapy, a significant ramp-up in clinician education and healthcare system logistics will be crucial for widescale adoption. The 40 ATCs are a good start, but they would need to operationalize swiftly to leverage first-mover advantage. Additionally, long-term outcomes and post-market surveillance data will be critical in assessing the real-world efficacy and safety of lifileucel, which could sway clinician and payer sentiment over time.

In light of the current facts and forthcoming catalysts, I am upgrading my investment recommendation for Iovance from “Hold” to “Buy.” The company’s regulatory prospects, insider confidence, and reinforced financial standing make for a compelling investment case. Still, investors should exercise due diligence given the inherent uncertainties tied to the commercial success of a novel therapy like lifileucel.

Balancing the high-risk, high-reward profile of Iovance, a strategically timed entry at this juncture could offer significant upside potential. Keep an astute focus on regulatory updates and monitor the execution of their commercial launch strategy post-approval to gauge long-term viability.

Risks to Thesis

While I’ve recommended a “Buy” for Iovance, several risks warrant closer scrutiny:

-

Intellectual Property: Given the competitive landscape of T-cell therapies, a failure to protect IP could significantly dilute Iovance’s market position.

-

Reimbursement Risks: My optimism on payer engagements may underestimate challenges, especially in private insurance markets where cost-containment pressures are high.

-

Competitive Readouts: Upcoming data from competitors in the TIL or CAR-T space could shift attention and resources away from lifileucel.

-

Regulatory Uncertainty: Although the FDA extension is deemed procedural, future roadblocks can’t be ruled out, affecting timelines and cash burn.

-

Market Adoption: The success of the 40 ATCs could be slower than anticipated, affecting revenue streams and market positioning.

-

Clinical Data: Longer-term data revealing adverse events could dent clinician and payer sentiment.

-

Internal Financial Metrics: The uptick in R&D spend coupled with high cash burn could stress finances if milestones aren’t met, requiring additional dilutive capital.

Read the full article here