Note:

I have covered Imperial Petroleum (NASDAQ:IMPP, NASDAQ:IMPPP) previously, so investors should view this as an update to my earlier articles on the company.

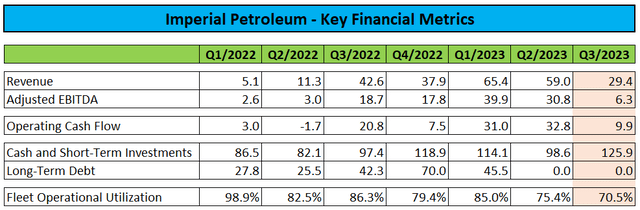

Last week, Imperial Petroleum reported very weak third quarter results as fleet utilization suffered from an elevated number of dry-dockings as well as seasonally weaker demand.

In addition, revenues and cash generation were impacted by the sale of the Aframax tanker Stealth Berana (now renamed Afrapearl II) to recent spin-off C3is Inc. or “C3is” (CISS) in July.

Press Releases / Regulatory Filings

Nevertheless, the company still managed to generate almost $10 million in cash flow from operations which in combination with the initial down payment received from C3is for the Stealth Berana and net proceeds from the August equity and warrant offering resulted in cash and short-term investments to increase by $27.3 million sequentially to $125.9 million.

The company continues to have no debt.

However, Imperial Petroleum’s cash position is expected to take a $70+ million hit in Q1/2024 with the delivery of two tankers acquired substantially above market value in the company’s worst related-party dealing to date.

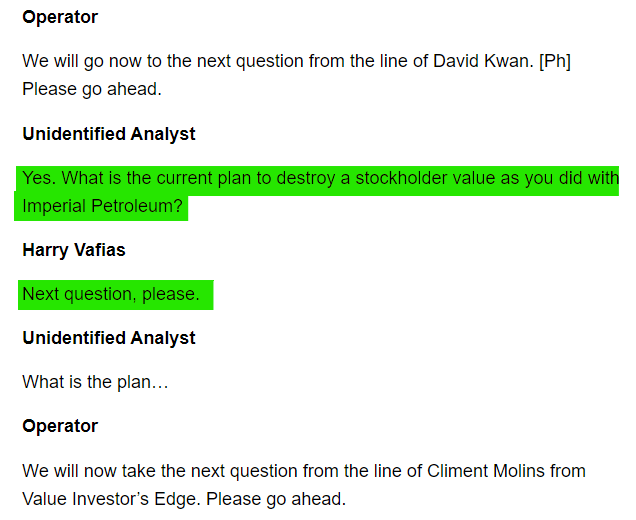

In recent months, the company and particularly CEO and controlling shareholder Harry Vafias have come under increased pressure from market participants to abstain from further dilutive offerings.

The abysmal performance of Imperial Petroleum’s common shares even resulted in an angered investor crashing the former parent StealthGas’ (GASS) most recent conference call:

Seeking Alpha Transcript

Apparently, Imperial Petroleum has started to reverse course in recent weeks as the company announced a $10 million share repurchase program in early September and subsequently bought back almost 5% of its outstanding shares at an average price of approximately $1.67.

In addition, the company has repurchased approximately 2.58 million of out-of-the-money Class C and Class D Warrants for $0.62 million.

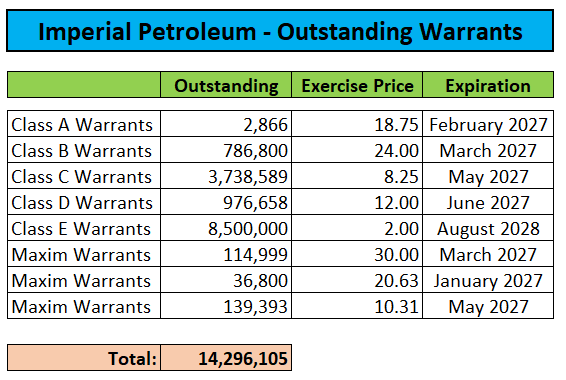

However, there’s still a substantial number of potentially dilutive warrants outstanding:

Regulatory Filings

Please note that Mr. Vafias holds 13,875 of the company’s Series C Convertible Preferred Shares with an aggregate liquidation preference of $13.875 million.

With common shares currently trading near the conversion floor price of $1.50 and mounting pressure by market participants, Mr. Vafias might be inclined to convert his preferred stock holdings into an approximately 25% common equity stake.

Regulatory Filings

While heavily dilutive, the move would result in Mr. Vafias becoming more aligned with common equity holders thus reducing the probability of further dilutive equity offerings substantially.

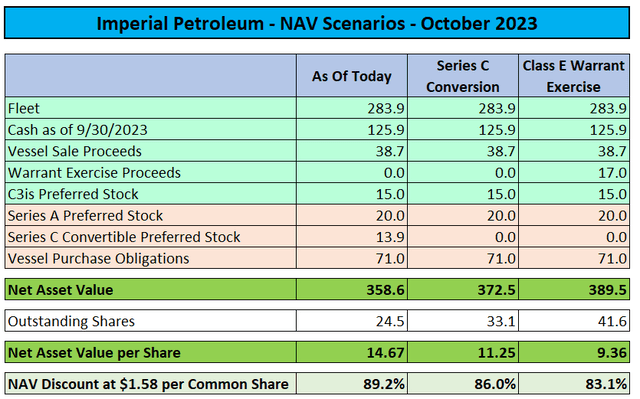

Valuation-wise, even when assuming the above-discussed Series C Preferred Stock conversion and exercise of all of the company’s outstanding Class E Warrants at a price of $2.00 per share, Imperial Petroleum’s common shares are still trading at an approximately 83% discount to estimated NAV:

Press Releases / Regulatory Filings / MarineTraffic.com

Based on my assumption for Imperial Petroleum to continue share buybacks and Mr. Vafias potentially converting his preferred shareholdings, I am upgrading the common shares from “Sell” to “Speculative Buy“.

But given the company’s tainted past and poor corporate governance, only the most speculative investors/traders should consider taking a position in Imperial Petroleum.

In addition, investors should note the overhang from the Class E Warrants which would come into play should the share price eclipse $2.

Bottom Line

Similar to peer Performance Shipping (PSHG), Imperial Petroleum appears to have reversed course as of late. Rather than diluting common shareholders even further, the company has started to buy back common shares and warrants under its recently announced $10 million repurchase program, likely due to mounting pressure from market participants.

With additional share and warrant buybacks as well as a potential preferred stock conversion by CEO Harry Vafias providing for strong near-term catalysts, I am upgrading the common shares from “Sell” to “Speculative Buy“.

However, given Imperial Petroleum’s tainted history and ongoing, poor corporate governance, only the most speculative investors/traders should consider taking a position in the company’s common shares.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here