Investment Thesis

Receiving a regular dividend income coupled with the prospect of capital appreciation is one of the principal benefits for those who invest in high dividend yield companies.

However, identifying high dividend yield companies that offer sustainable dividends can be a challenging task. Companies that pay sustainable dividends don’t only provide you with the chance to get immediate dividend payments, but also with a source of income that continuously increases. Identifying companies that pay sustainable dividends is particularly important when it comes to retirement planning.

Furthermore, choosing companies with sustainable dividends reduces the likelihood of experiencing a dividend cut, which could significantly impact the stock price of the chosen company negatively. Consequently, this can adversely impact the Total Return of your investment portfolio, particularly if the respective stock accounts for a relatively large percentage compared to the overall portfolio.

In this article, I have filtered out two high dividend yield companies which I currently consider to be appealing for dividend income investors. This is given their current Valuation, robust financial health, ability to generate income, and their track record of dividend growth.

However, it is worth noting that I perceive one of these selections as having a higher risk of dividend reduction, which is why I suggest underweighting this company in your investment portfolio.

The companies needed to fulfil the following requirements to be included in a pre-selection:

- Dividend Yield [FWD] > 3%

- P/E [FWD] Ratio < 30

- Return on Equity > 10%

I selected the following two companies for March 2024:

- CVS Health Corporation (NYSE:CVS)

- The Bank of Nova Scotia (NYSE:BNS)

CVS Health Corporation

CVS Health Corporation is a provider of health solutions with a current Market Capitalization of $93.55B.

With a Dividend Yield [FWD] of 3.59% and a 10 Year Dividend Growth Rate [CAGR] of 10.07%, CVS Health Corporation provides investors with an appealing mix of dividend income and dividend growth. These metrics indicate that the company should be an attractive candidate for investors planning to benefit from steadily increasing dividend enhancements while investing over the long term.

Among CVS Health Corporation’s competitive advantages are its extensive network within the Health Care Industry, strong brand recognition, diversified business model (which contributes to mitigate risks), and its economies of scale (which help to reduce costs).

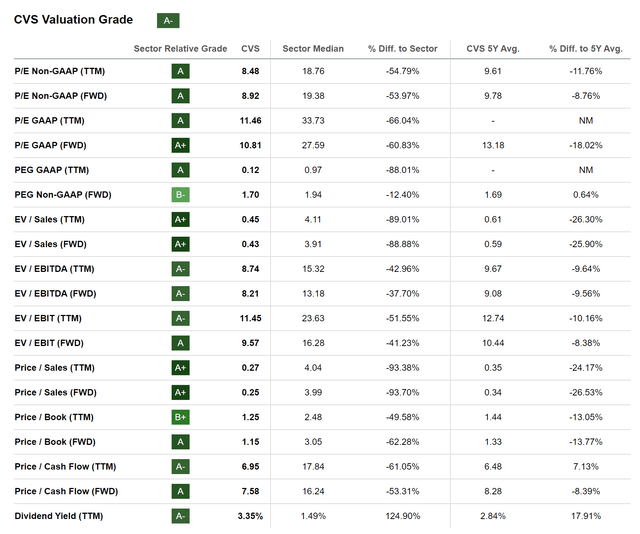

CVS Health Corporation in Terms of Valuation

I consider CVS Health Corporation to currently be undervalued. First, the company’s current P/E [FWD] Ratio of 10.81 not only stands 18.01% below its 5-year average but also 60.83% below the Sector Median, clearly indicating that the company is presently undervalued.

Second, its Price/Sales [FWD] Ratio of 10.25 not only stands 26.53% below the company’s 5-year average but also 93.70% below the Sector Median.

Third, CVS Health Corporation’s Dividend Yield [TTM] of 3.35% stands 17.91% above its 5-year average, and also 124.90% above the Sector Median, further strengthening my belief that the company is undervalued.

This undervaluation is further reflected in the Seeking Alpha Valuation Grade for the company, which you can find below.

Source: Seeking Alpha

CVS Health Corporation’s Attractive Dividend

Different metrics underscore the attractiveness of CVS Health Corporation’s Dividend: the company’s Dividend Yield [FWD] of presently 3.59% not only stands above its average from the past 5 years (2.90%) but also significantly above the Sector Median (1.62%).

In addition to that, it can be highlighted that the company’s Free Cash Flow Yield [TTM] of 10.91% reflects its attractive risk-reward profile, indicating that its stock price is not a result of high growth expectations. This strengthens my belief that you can presently invest in CVS Health Corporation with a margin of safety.

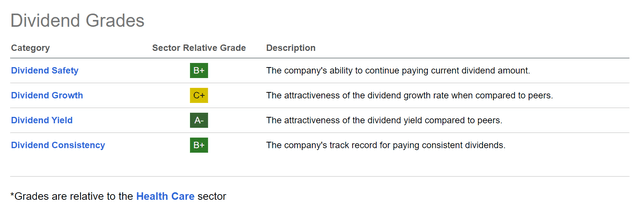

CVS Health Corporation According to The Seeking Alpha Dividend Grades

The attractiveness of the company’s Dividend is further underscored when having a look at the results of the Seeking Alpha Dividend Grades: CVS Health Corporation receives an A- rating for Dividend Yield and a B+ for Dividend Safety and Dividend Consistency. For Dividend Growth, the company receives a C+.

Source: Seeking Alpha

The Bank of Nova Scotia

The Bank of Nova Scotia is headquartered in Toronto and was founded in 1832. The Canadian bank operates through the following segments:

- Canadian Banking

- International Banking

- Global Wealth Management

- Global Banking and Markets segments

The Bank of Nova Scotia in Terms of Valuation

I consider The Bank of Nova Scotia to currently be undervalued. This is the case since the bank’s P/E [FWD] Ratio of 10.33 lies slightly below the Sector Median of 10.47. In addition to that, it can be highlighted that its Price/Book [FWD] Ratio of 1.13 stands 11.04% below its 5-year average (1.27), further indicating that the Canadian bank is undervalued at the time of writing.

When compared to U.S. banks such as JPMorgan (NYSE:JPM) and Bank of America (NYSE:BAC), The Bank of Nova Scotia exhibits a slightly lower Valuation: while the Canadian bank showcases a P/E [FWD] Ratio of 10.33, JPMorgan’s stands at 11.76 and Bank of America’s at 11.21.

It is further worth highlighting that The Bank of Nova Scotia pays a significantly higher Dividend Yield (6.39% compared to Bank of America’s 2.71% and JPMorgan’s 2.23%) than its U.S. competitors.

The Bank of Nova Scotia in Terms of Profitability

The Bank of Nova Scotia’s Net Income Margin of 26.75% (which stands 14.11% above the Sector Median) and its Return on Equity of 10.34% reflect the bank’s strong Profitability and financial health. Its financial health is further underscored by an Aa2 credit rating from Moody’s.

The Attractiveness of The Bank of Nova Scotia’s Dividend

I am convinced that the Canadian bank is particularly appealing for dividend income investors, given an attractive Dividend Yield [FWD] of 6.39% in combination with a 5 Year Dividend Growth Rate [CAGR] of 4.28%.

The attractiveness of The Bank of Nova Scotia’s Dividend Yield in combination with its dividend growth potential, strengthens my confidence that the Canadian bank is a potential candidate for incorporation into The Dividend Income Accelerator Portfolio.

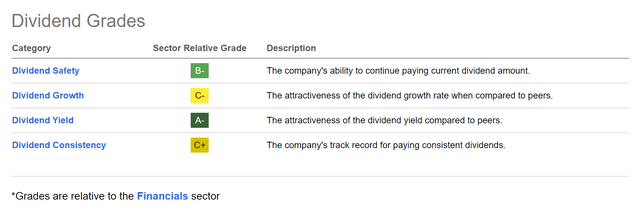

The Bank of Nova Scotia According to The Seeking Alpha Dividend Grades

The Seeking Alpha Dividend Grades further underscore my theory that the Bank of Nova Scotia is an appealing choice for dividend income investors. It receives an A- for Dividend Yield, a B- for Dividend Safety, a C+ for Dividend Consistency, and a C- for Dividend Growth.

Source: Seeking Alpha

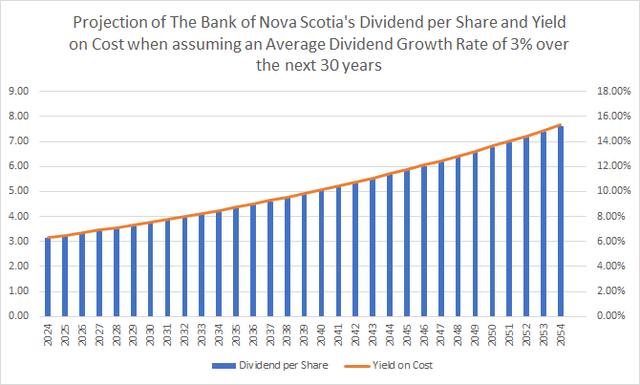

Projection of The Bank of Nova Scotia’s Dividend and Yield on Cost

The graphic below illustrates a projection of The Bank of Nova Scotia’s Dividend and Yield on Cost when assuming an Average Dividend Growth Rate of 3% for the following 30 years, further underlying the Canadian bank’s attractiveness for dividend income investors.

Source: The Author

Risk Factors

Given the risks associated with CVS Health Corporation and The Bank of Nova Scotia, it can be noted that I consider the risk level for investors of the Canadian bank to be marginally higher.

This higher risk level is reflected in the company’s elevated 24M Beta Factor of 1.00 when compared to CVS Health Corporation’s 24M Beta Factor of 0.48.

CVS Health Corporation’s relatively low 24M Beta Factor indicates that you can significantly reduce the volatility of your investment portfolio when including it in your portfolio. With a 24M Beta Factor of 1.00, The Bank of Nova Scotia mirrors the broader stock market’s Beta Factor, indicating identical volatility levels.

In addition to that, it can be highlighted that The Bank of Nova Scotia exhibits a significantly higher Payout Ratio of 66.59%, compared to CVS Health Corporation’s Payout Ratio of 27.69%. This showcases that the likelihood of a dividend cut is significantly higher for investors in The Bank of Nova Scotia.

This theory is further evidenced by The Bank of Nova Scotia’s negative EPS Growth Rate Diluted [FWD] of -5.93% in comparison to CVS Health Corporation’s positive EPS Growth Rate Diluted [FWD] of 2.02%. These metrics further evidence a higher likelihood of a dividend cut for The Bank of Nova Scotia when compared to CVS Health Corporation.

Due to the elevated probability of a dividend reduction, I suggest underweighting The Bank of Nova Scotia in a well-balanced dividend portfolio with a reduced risk level, providing the company with no more than 2.5% relative to your overall portfolio. This approach reduces the risk level of your portfolio and enhances your chances to obtain positive investment results when investing over the long term.

Conclusion

I am convinced that both CVS Health Corporation and The Bank of Nova Scotia can be excellent incorporations into your investment portfolio, contributing significantly to the generation of extra income through dividend payments.

Both CVS Health Corporation and The Bank of Nova Scotia pay an attractive Dividend Yield [FWD] of 3.59% and 6.39% respectively, have shown dividend growth in recent years (5 Year Dividend Growth Rates [CAGR] of 4.40% and 4.28% respectively), exhibit attractive Valuations (their current P/E [FWD] Ratios stand below the Sector Median), and both are financially healthy (Baa2 and Aa2 credit ratings from Moody’s).

Including both CVS Health Corporation and The Bank of Nova Scotia in an extensively diversified dividend portfolio which unifies high dividend yield and dividend growth companies brings plenty of benefits for investors.

You can use this extra income through dividends to further enhance your investment portfolio by reinvesting or to manage your day-to-day expenses.

Wouldn’t it be nice to explore the possibility of using the dividend payments of CVS Health Corporation and The Bank of Nova Scotia to finance your next family getaway?

Author’s Note: I would appreciate hearing your opinion on this article! If you could only choose two high dividend yield companies for this month of March, which would you select?

Read the full article here