Thesis

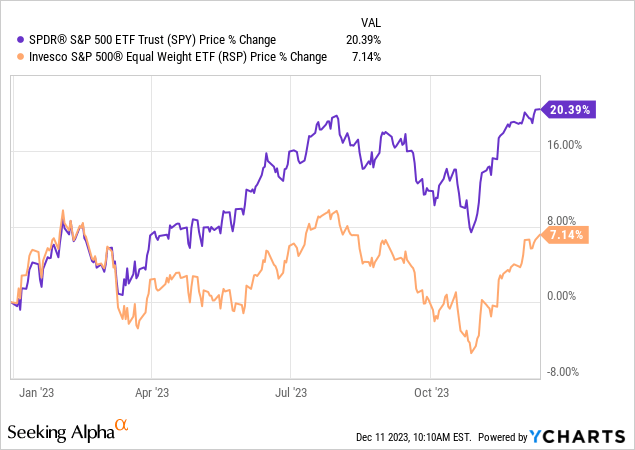

Despite very pessimistic expectations, equities have done well in 2023. The recession that everybody expected did not materialize, instead, we got an artificial intelligence (‘AI’) revolution. The AI craze pumped up mega-cap tech stocks, which have posted tremendous results this year when compared to the rest of the index:

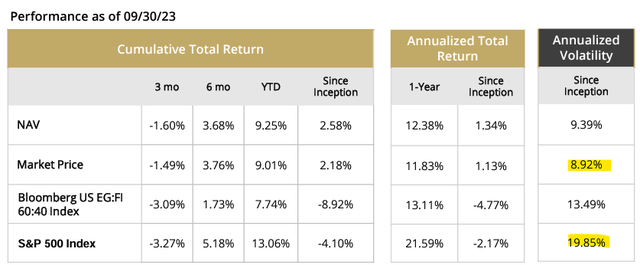

After being negative in October, the S&P 500 Equal Weight ETF (RSP) is now at a respectable +7.14% price return but lags the SPY given the equal weighting in its composition.

The Simplify Hedged Equity ETF (NYSEARCA:HEQT) is a fund we have covered before, writing a piece early in the year shortly after the fund was IPO-ed. In our initial coverage piece, we highlighted the innovative collar strategy that retail investors could now access, with more established vehicles such as the JPMorgan Hedged Equity Fund Inst (JHEQX) having been closed to retail investors for long stretches of time. The fund performed as expected, with a low volatility profile during risk-off events as compared to the S&P 500.

In revisiting the fund, we are going to frame it in today’s equity environment and asses if the ETF represents a better choice than an outright S&P 500 investment. With valuations stretched and an uncertain picture of what 2024 will bring, the retail investor is best served to be cautious in their equity purchases. In this article, we are going to go through the reasons why we believe HEQT is a smart way to buy equities here versus an outright SPY purchase, and walk through the mechanics of a down scenario in the index and its implications for HEQT.

What is a put-spread collar?

A put-spread collar is a complex options strategy that involves the buying of a protective put-spread on the downside concurrently with the selling of a call that caps the upside. In effect, the cash obtained from selling the call is utilized to buy the put spread (for zero cost put-spread collars). A simple collar involves the buying of a put and the selling of a call. HEQT does a more complex version via the purchase of a put spread (i.e. the fund sells a lower strike put as well). The additional complexity is layered in to keep costs as close to zero as possible. There is a trade-off between the strike price of the put and the cost associated with it.

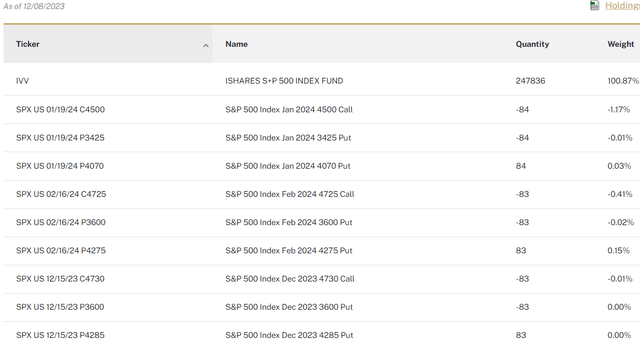

HEQT takes a laddered approach to its options:

Options (Fund Fact Sheet)

The above table represents the current holdings. A ‘laddered approach’ simply means there are put-spread collars for December 2023, January 2024 and February 2024. Therefore, the fund does not roll all of its options at one time. Let us have a closer look at the February structure so that we can translate for investors the implications of the strategy.

We can see the fund long the S&P 500 via IVV. For February, the fund purchased puts with a 4,275 strike and sold calls with a 4,725 strike. Furthermore, it sold puts with a lower strike of 3,600. This structure translates into the fund having a capped upside at that level, but a protected downside below 4,275 until 3,600 (22% drawdown). The collar structure ensures the fund is ‘collared’ in a certain band, thus not being able to participate in the full move up, but also having a significant buffer in case of a market sell-off.

How did the HEQT collar structure perform historically?

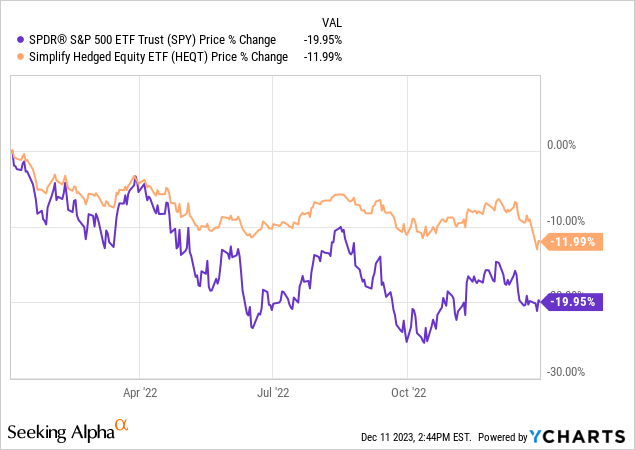

Let us have a look at how the put-spread collar translates into volatility and actual performance:

We charted above the 2022 performance for the SPY and for HEQT. HEQT ended up having half the loss exhibited by the index in 2022, with a 50% drawdown when compared to the index. While the SPY moved down to -22% in October, HEQT never exceeded a -12% loss.

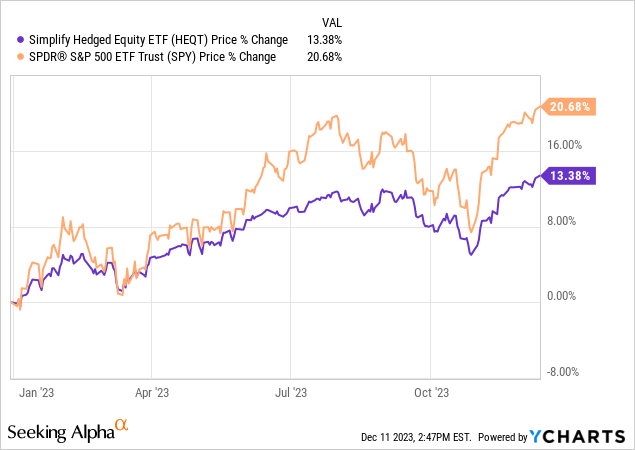

Conversely, in 2023, HEQT participated in more than 60% of the upside:

What is interesting to note is also that during the recent market swoon in October, the two funds’ returns came close to converging. HEQT’s performance is going to be dependent on volatility levels and volatility skew, and will not always reflect the exact correlations seen in 2022 or 2023. However, think of HEQT as a dampened take on the market, where regular drawdowns (i.e. -20%) translate into a very rough 0.5 factor for HEQT, while slow upside moves are participated in to a large extent. The worst-case scenario for HEQT is a very violent and sudden rise in the index, as we can clearly see via its November differential to the SPY.

From an analytics standpoint, HEQT has half the volatility of the index:

Volatility (Fund Fact Sheet)

Volatility is not directional but represents the degree of variation in the price of the security. All else equal, a retail investor should desire a low level of volatility.

Why is HEQT better than outright SPY right now?

We are closing in on the all-time highs for the SPY, yet many questions linger regarding the true lagged impact of higher rates on the economy. The index has been driven higher this year by a handful of stocks rather than broad participation, which has brought the ‘magnificent 7’ to represent a record proportion of the index. Many questions remain unanswered, but we are hard-pressed to see today’s environment as the start of a new healthy bull market without a correction first.

Buying equities outright at this juncture subjects a holder to the full volatility and swings inherent in the index. Given the lingering concerns around a true new bull market, a retail investor is better served by purchasing equities via HEQT given the substantial downside protection during a correction. If a new bull is truly confirmed, said retail investor can just switch from HEQT to SPY, while a potential correction will have a much lower impact on HEQT, thus providing investors with the ability to safely add to equities even when the market tanks. One has to be careful in buying a top, and this is what we are potentially witnessing here in the SPY.

What are the forward-looking expectations for the fund?

HEQT is going to mirror the SPY performance, but with a dampened volatility profile, as outlined above. At the current skew levels, the fund will participate in 60% of the upside while dampening 50% of the downside. As highlighted above, uncertainty persists in the market, with mixed views on the forward for the index from the large sell-side investment banks. We are of the opinion we are going to see another -10% correction in the index in March/April after a strong start of the year, as per the seasonality factors. Portfolio construction in an uncertain environment favors lower volatility structures.

Competitors and risks

HEQT was set up to compete with the JPMorgan Hedged Equity Fund Inst (JHEQX), which was closed to new investors until very recently:

Emboldened by this disruptive boom in market hedging, Simplify Asset Management is pitching an easy-to-access ETF that deploys a similar strategy to the JPMorgan whale, while being less exposed to the vagaries of the crowded marketplace for derivatives.

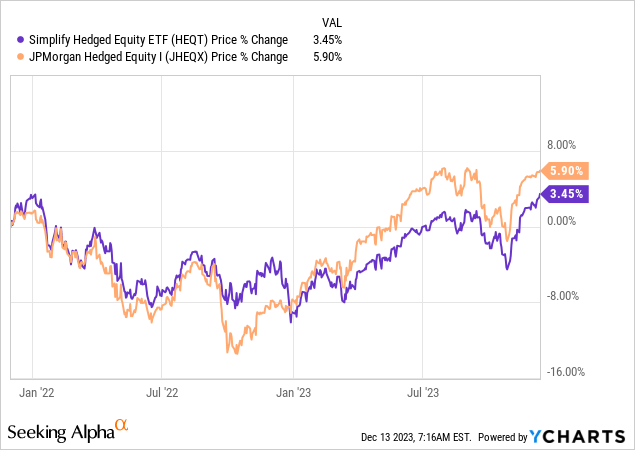

JHEQX is a market behemoth with a $16 billion portfolio, and initially was addressed to institutional clients only. The two vehicles have a very similar performance since the HEQT inception:

The risks for a HEQT investment lie with outsized moves in the index. As described above, the fund uses a put-spread structure, meaning that outsized down moves are not covered. Any move below 3,600 in the S&P 500 index will represent a 1:1 loss for the fund until the next roll date for the collars.

Conclusion

HEQT is an exchange-traded fund. The vehicle takes a position in the S&P 500 and then hedges out volatility via a put-spread collar structure. This complex overlay results in a drawdown that is roughly 50% of the one exhibited by the index, and an upside participation in excess of 60%. The exact figures will depend on net volatility levels and skew as options are rolled. The fund therefore represents a less volatile way to invest in the S&P 500, and in times of uncertainty regarding the net direction of equities, HEQT prevails as a safer alternative to an outright SPY purchase. We are of the opinion that we will see another correction before a true bull market takes hold, therefore retail investors needing to add S&P 500 exposure to their portfolios are better served by doing so via HEQT rather than an outright index purchase.

Read the full article here