Gulfport Energy (NYSE:GPOR) is refinancing its May 2026 notes with new September 2029 notes that carry a 1.25% lower interest rate. This pushes Gulfport’s note maturity out by over three years and also end up saving it roughly $6 million per year in interest costs.

Near-term natural gas prices are fairly weak, but with the help of hedges, Gulfport is projected to generate $173 million in 2H 2024 free cash flow and $350 million to $400 million in 2025 free cash flow at current strip.

Operational efficiencies and the impact of continued share repurchases, increases my estimate of its value by $5 per share compared to a few months ago. I now estimate its value at $159 to $176 per share, and consider it a buy at its current sub-$140 share price.

Debt Refinancing

Gulfport is issuing $650 million in new 6.75% unsecured notes due September 2029 and using most of those proceeds to repurchase its 8.0% unsecured notes due May 2026. Gulfport has $550 million in outstanding 8.0% notes.

It appears that Gulfport’s tender offer for the 2026 notes may currently involve a price of slightly over 102% of par. Gulfport’s tender offer (at 100% participation) would thus cost around $562 million in total, not including accrued and unpaid interest of approximately $12 million. Gulfport expects to redeem any untendered notes in May 2025 at 100% of par.

After commissions and other expenses, this may leave around $65 million for reducing Gulfport’s credit facility debt.

These transactions help reduce Gulfport’s interest costs by approximately $6 million per year.

Q2 2024 Results

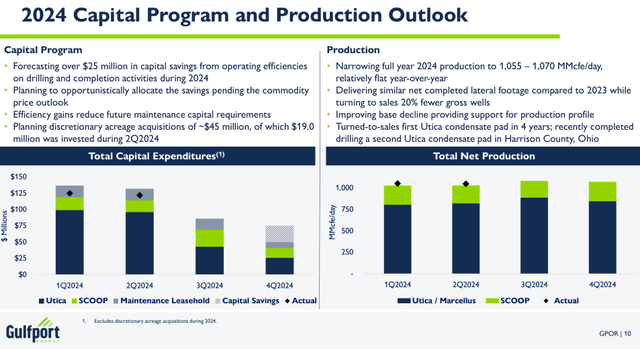

Gulfport’s Q2 2024 production ended up at 1.05 Bcfe per day, roughly the same as its Q1 2024 production of 1.054 Bcfe per day and marginally above its expected production for the quarter. It also achieved this with $122.2 million in incurred capex, which was lower than budgeted.

Gulfport’s Capex And Production (gulfportenergy.com (Q2 2024 Presentation))

Gulfport realized $0.26 less than NYMEX for its natural gas before hedges in Q2 2024. Gulfport’s natural gas hedges added $1.03 per Mcf in value, so it actually realized $0.77 above NYMEX for its natural gas after hedges.

Despite the low benchmark natural gas prices (with the average daily NYMEX settled price under $2 during the quarter), Gulfport still generated $20 million in adjusted free cash flow. This was largely due to its hedges.

Gulfport also mentioned that it expects $25+ million in full-year capex savings from operational efficiencies in its development work.

2H 2024 Outlook

Gulfport narrowed its full-year guidance range to a new range of 1.055 Bcfe to 1.07 Bcfe per day. The mid-point of its guidance range was unchanged.

Gulfport expects increased production in 2H 2024 and thus may average around 1.073 Bcfe during the second half of the year. This would get it to the mid-point of its full-year production guidance.

Gulfport also noted that its production is expected to have an increasing percentage of liquids as it does more development of its liquids-rich assets.

Gulfport’s natural gas percentage was 92% to 93% in 1H 2024, and I am modeling that at 91% for 2H 2024. By 2026, Gulfport currently expects its natural gas percentage to come down to the high-80s, although it believes that mid-80s is probably the minimum due to its large dry gas base.

At the current 2H 2024 strip of $72 to $73 WTI oil and $2.30 NYMEX gas, I expect Gulfport to generate around $473 million in oil and gas revenues before hedges. Gulfport’s 2H 2024 hedges have approximately $153 million in positive value at those prices.

| Type | Units | $/Unit | $ Million |

| Natural Gas [MCF] | 179,663,120 | $2.00 | $359 |

| NGLs (Barrels) | 2,211,480 | $28.50 | $63 |

| Oil (Barrels) | 750,000 | $67.50 | $51 |

| Hedge Value | $153 | ||

| Total Revenue | $626 |

Gulfport is now projected to generate $173 million in 2H 2024 free cash flow. This also assumes reinvests the $25 million in capex savings into late 2024 development.

| Expenses | $ Million |

| Transportation, Gathering, Processing and Compression | $182 |

| LOE | $36 |

| Taxes Other Than Income | $18 |

| G&A | $24 |

| Cash Interest and Preferred Dividends | $18 |

| Capex (Including Discretionary Acreage Acquisitions) | $175 |

| Total Expenses |

$453 |

Gulfport intends to put most of its free cash flow towards share repurchases. This could allow it to reduce its share count to approximately 20 million by the end of 2024, including the impact of preferred share conversion.

Estimated Valuation

At the current strip for 2025 (including $3.15 NYMEX), I believe that Gulfport can generate $350 million to $400 million in free cash flow after hedges. This is a scenario that involves modest production growth and does not include spending on discretionary acreage acquisitions.

At $75 WTI oil and $3.75 NYMEX gas (my long-term commodity prices), it appears that Gulfport could generate $500 million to $550 million in free cash flow, or roughly $25 to $27.50 per share based on 20 million outstanding shares.

At a 15% free cash flow yield and adjusted downward for lower 2025 commodity prices, this would make Gulfport worth around $159 to $176 per share.

Conclusion

Gulfport should be able to generate around $550 million in free cash flow over the next year and a half, despite weak near-term natural gas prices. This is with the benefit of hedges, although it may be able to generate close to $550 million in free cash flow per year at $3.75 NYMEX gas instead.

Gulfport’s debt refinancing takes care of its note maturities until 2029, and it is planning on putting most of its free cash flow towards share repurchases. This could reduce its share count (including the conversion of preferred shares) to around 20 million by the end of 2024.

Gulfport’s operational efficiency improvements and share repurchases boost my estimate of its value to $159 to $176 per share.

Read the full article here