We’re upgrading Alphabet Inc. (NASDAQ:GOOG) (NASDAQ:GOOGL) aka Google to a buy ahead of earnings, scheduled for October 24th. We now see a clearer growth path for Google ads revenue as digital ad spending picks up in 2024. The company’s ad revenue accounts for ~78% of total sales, we’re more constructive now, as we expect a rebound from the low single-digit growth in ad revenue will reaccelerate Alphabet’s top-line growth.

Our previous bearish sentiment on the stock was based on our belief that ad spend would remain muted in 2H23 due to the higher interest rate environment forcing ad firms to optimize spend; we’ve seen the slower ad spend impact Alphabet’s top-line growth with revenue growing 7%, 2.6% and 1% over 2Q23, 1Q23 and 4Q22, respectively. We now see top-line growth pushing into the double-digit range in 2024. Ad firms pulled back significantly on spending this year due to the uncertain macro environment; global ad spending is estimated to grow 4.4% this year, lowered from previous forecasts of 5.9% Y/Y growth.

In contrast, ad spend is expected to rebound by 8.2% Y/Y in 2024, pushing the total ad spend over $1T for the first time, according to WARC’s global ad spend outlook for 2023/24. While we understand investor concerns of macro headwinds hindering the rebound next year, we think the U.S. Presidential election and Olympics, both set for 2024, will help offset macro uncertainty, as these events have been historic catalysts for an uptick in ad spend. We expect Google to be at the heart of the rebound and see financial outperformance towards 2H24.

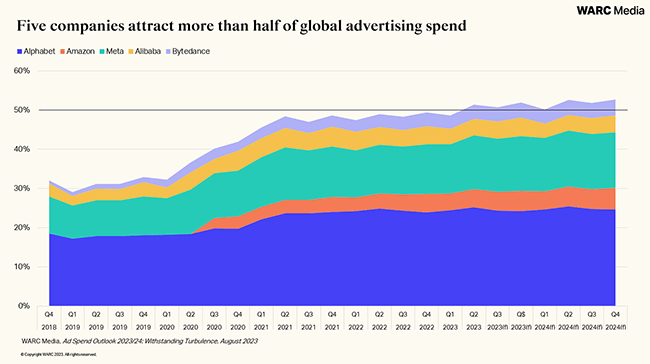

The following outlines the global ad spend forecast by market share.

WARC Media

We expect macro headwinds to ease in 2024 and expect Alphabet’s search engine dominance will continue to stretch out its visibility as a lucrative ad platform, especially after Microsoft’s (MSFT) failed efforts to position A.I.-empowered Bing to take a larger chunk of the market earlier this year. In 2024, Google is estimated to command roughly 83.1% of the global search market, with Microsoft’s share at 6% and China’s Baidu (BIDU) potentially seeing a share drop to 6.5%. Additionally, we’re not too concerned about the U.S. Department of Justice suing Alphabet for monopolizing search and search advertising; the civil antitrust lawsuit constitutes the most high-profile technology lawsuit in decades, but don’t expect it’ll hinder top-line growth in the near-to-mid term.

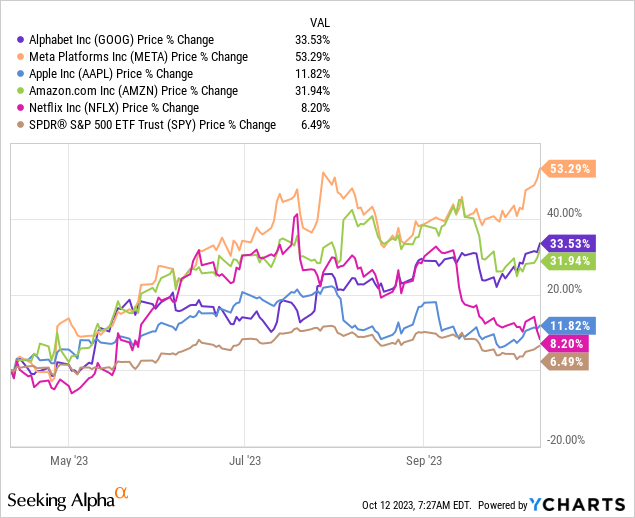

The stock has outperformed the FAANG peer group and S&P 500 (SP500) over the past six months, with the exception of Meta Platforms (META), which remains our favorite pick among the group into 2024. Alphabet is up 36% over the past 6M, outperforming the S&P 500 by 28%. We see Alphabet outperforming the peer group more significantly in 2024 and recommend investors buy into the growth. The following chart outlines Alphabet’s stock performance against Meta, Apple (AAPL), Amazon (AMZN), Netflix (NFLX), and the S&P 500 over the past six months.

YCharts

Google Cloud pushing new heights

Google Cloud pushed into new heights last quarter, climbing 28% Y/Y, while Microsoft’s Azure saw a sequential slowdown to 26% growth. We see momentum only expanding from here for the Google Cloud segment. We’ve been cautious about cloud growth in 2023 due to macro headwinds weighing on consumption growth as customers optimize spending in 2H23. Google Cloud achieved a higher growth rate in 2022 than AWS and Microsoft, according to Gartner data, and we expect to see a reacceleration in growth to higher double digits in 2024.

Valuation

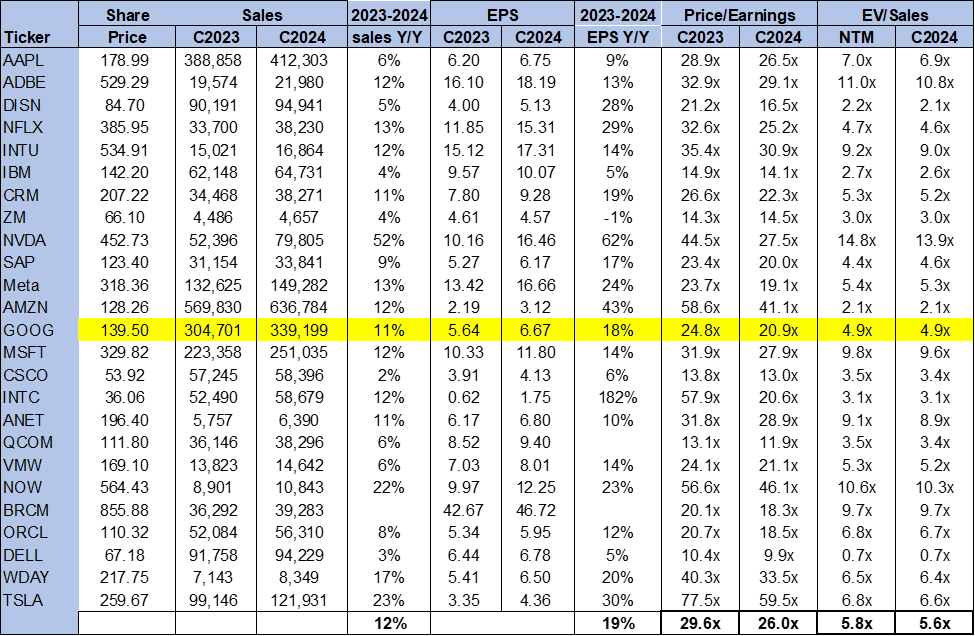

Alphabet stock is relatively cheap, in spite of its dominant position in the search engine market and expanding share as a cloud computing provider. On a P/E basis, the stock is trading at 20.9x C2024 EPS $6.67 compared to the peer group average of 26.0x. The stock is trading at 4.9x EV/C2024 Sales versus the peer group average of 5.6x. We see attractive entry points into the stock at current levels and recommend investors take advantage of the stock price volatility triggered by the DOJ’s lawsuit and add opportunistically on pullbacks.

The following chart outlines GOOGL’s valuation against the peer group.

TSP

Word on Wall Street

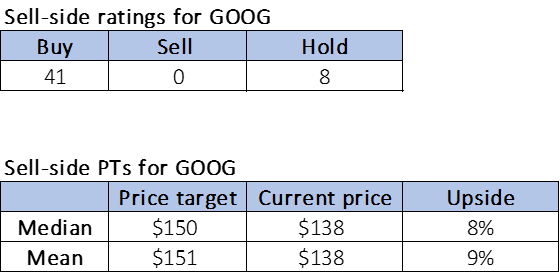

Wall Street shares our bullish sentiment; of the 49 analysts covering the stock, 41 are buy-rated, and the remaining are hold-rated. The stock is priced at $138 per share. The median sell-side price target is $150, while the mean is $151, with a potential 8-9% upside. The following charts outline the stock’s sell-side price targets and ratings.

TSP

What to do with the stock

We’re upgrading Alphabet stock to a buy ahead of earnings; we expect the stock to outperform the peer group in 2024. Our upgrade is driven by our belief that top line growth will reaccelerate as digital ad spending picks back up in 2024 and Google Cloud continues to exhibit resilient, profitable growth into next year. The stock is trading below the peer group in terms of valuation, and we think it’s undervalued at current levels. We see attractive entry points and recommend investors look to add or initiate a position in Google stock during the back end of the year.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here