Investment Thesis

Garrett Motion (NASDAQ:GTX) has successfully completed its Chapter 11 restructuring, enabling it to emerge from bankruptcy; as a result of this and other recent developments, I am bullish on this stock. With the company coming up with new financing and capital structure, I expect its financial leverage, financial discipline, and efficiency to improve, which I believe will help propel the company to tremendous growth going forward.

Further, given the company’s strong Q2 ’23 performance, I am confident that it is now on a good trajectory which I believe will be fuelled by its competitive positioning and growth potential. Its investment in research and innovation will, in my opinion, help the company in its long-term success. Based on these variables, I believe GTX stock is a good investment opportunity for growth-oriented investors. I recommend it to potential investors seeking to diversify to growth stocks, especially in the auto industry.

Current Affairs: Nothing But A Promising Future

Based on GTX’s recent developments, I believe the firm is taking shape and may be on the verge of a great recovery from its bankruptcy struggles. In terms of current developments, I will concentrate on the Chapter 11 restructuring, MRQ performance, and my thoughts on these developments.

1. Chapter 11 Restructuring

First, GTX completed Chapter 11 restructuring with new capital and a strong balance sheet on April 30, 2023. The firm emerged from bankruptcy with a new finance and capital structure that banished Garrett’s previous asbestos indemnity and any related liabilities to Honeywell incurred in its 2018 spin-off, as well as the resolution of all litigation between Garrett and Honeywell. Furthermore, the company announced in June the conversion of its Series A Preferred Stock into a single class of Common Stock, which I believe is consistent with its capital restructuring.

In my view, these aspects positively impacted the company in terms of reducing its effective leverage and increasing its operational, financial, and strategic flexibility. Here is how I think this was possible;

- Garrett was able to lower its funded debt from $2.1 billion to $1.25 billion equivalent term loan and $300 million revolving credit line through Chapter 11. This means GTX has lower interest expenses and debt obligations, which increases company cash flow and liquidity. The removal of the 30-year indemnity lowered Garrett’s effective leverage while increasing its operational, financial, and strategic flexibility. In return for the termination of the indemnity, Garrett made an initial cash payment to Honeywell of $375 million and granted Series B Preferred Stock to Honeywell, which entitles Honeywell to certain cash payments from 2022 through 2030. The Series B Preferred shares can be repaid at any time at a present value (about $584 million as of the date of emergence at the agreed-upon discount rate of 7.25%), resulting in much-needed flexibility.

About the conversion of Series A preferred stock, below is my take on how it will impact the company;

- Financial flexibility: The conversion will increase the company’s financial flexibility by freeing cash flow that was previously required to pay dividends on series A preferred stock. The corporation anticipates saving around $80 million each year in dividend payments. This cash flow can be used to pay down debt, repurchase common stock, or seek strategic opportunities, which I believe will be a long-term growth catalyst.

- Leverage: In the short term, the conversion raised the company’s leverage ratio since it reduced its equity basis and raised its debt-to-equity ratio. The business incurred $700 million in new debt in conjunction with the repurchase of approximately $570 million in shares of series A preferred stock held by certain Center Bridge Partners, L.P. and Oaktree Capital Management, L.P. funds. However, I expect this will be offset by cash flow savings from dividend payment reductions and returns realized from the new capital allocation discipline, resulting in a significantly lower leverage ratio.

- Capital structure: The conversion improved the company’s financial structure by eliminating the series A preferred shares and creating a single class of common stock. This boosted the company’s market capitalization, improved its liquidity, and potentially qualify it for index inclusion. The conversion will also lower the company’s capital cost because the 11% dividend on the series A preferred shares will no longer be paid.

Completing the Chapter 11 restructuring comes with a lot of financial flexibility, low leverage, and what I believe will be an improved financial discipline. This flexibility and solid financial footing will enable the company to grow in the long run because it will be in better position to exploit the opportunities in the market and execute its long-term growth ambitions. Further, with what I anticipate to be an improved cash flow, I expect the company to return capital to shareholders through share repurchases. In my view, these aspects will propel the company to a solid upward trajectory in the future.

2. Solid Q2 ‘23

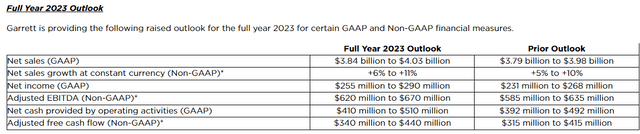

GTX reported good financial results for the second quarter of 2023, raised its outlook for the whole year, and announced plans to pay off some of its. Net sales totaled $1,011 million, an increase of 18% in GAAP terms and 19% in constant currency terms, exceeding global vehicle production by nearly 12.5 percentage points. The company made $71 million in net income and $170 million in adjusted EBITDA, with a 16.8% adjusted EBITDA margin. Also, $164 million in net cash flow from operations and $140 million in adjusted free cash flow were reported in the quarter. GTX planned to pay off $200 million in debt early in the third quarter of 2023. In terms of guidance, it also raised its outlook for net sales, adjusted EBITDA, and adjusted free cash flow in 2023 as follows.

Garrett Website

In my opinion, this company’s resilient and adaptable response to market shocks, operational efficiency, and cost discipline are all evident in its good financial performance. Additionally, I think it demonstrates a strong ability to generate cash flow, deleverage, and a competitive position in the market. Given this outstanding result, the enhanced financial outlook, and the implemented financial reorganization, I am confident about the company’s future financial performance.

Competitive Position: Long-term Growth Lever

Upon analyzing GTX, I see that it is well-positioned in the market and that this will be a driving force behind its long-term growth. As one of the leading providers of turbochargers, electric-boosting technologies, and software solutions, the firm enjoys a strong competitive position in the worldwide automobile market.

It serves more than 40 global automakers and more than 250 vehicle models across passenger cars, commercial vehicles, off-highway vehicles, motorcycles, and motorsports. The company has a loyal customer base, with an annual client retention rate of over 90%. The company also has a global footprint, with 13 manufacturing facilities and six engineering centers across 11 countries.

Its competitive position is based on its technological leadership and innovation capabilities, which enable it to offer high-performance, fuel-efficient, and emission-reducing solutions to its customers. The company invests about 6% of its revenue in research and development and holds approximately 1,700 patents. To address the changing needs of its clients, the company continuously introduces new products and solutions. For example, the corporation unveiled E-Turbo, a game-changing electric-boosting technology that combines a traditional turbocharger with an electric motor and power electronics to give greater performance, efficiency, and emissions for hybrid and electric vehicles. Predictive Control Software, Cybersecurity Software, and Connected Vehicle Solutions are some of the software solutions offered by the company that improve the operation, connectivity, and security of automobiles in a bid to meet diverse customer needs.

In my opinion, this competitive position, either in terms of product and regional diversity or innovation, will be a major growth lever because the diversity will boost the company’s resilience during tough economic downturns by leveraging booming market segments. Further, the innovative culture will enable the company to remain relevant in the dynamic consumer environment, something I believe will be critical to its long-term success.

Growth Potential: The Power Of The Growing Market

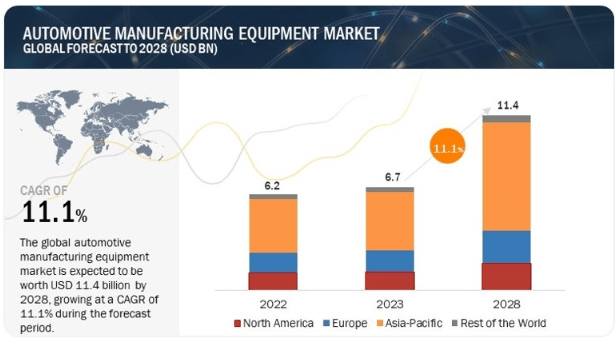

GTX has a high growth potential in the automotive industry, as it is well-positioned to benefit from the trends of electrification, connectivity, and sustainability that are driving the transformation of mobility. Below are the projected growth rates in the market.

AMEM

By 2028, the market for automobile manufacturing equipment is projected to be valued at $11.4 billion, expanding at a compound annual growth rate of 11.1%. Given its strategic position, I believe GTX is well-positioned to capitalize on this market, allowing the company to achieve even greater success. Furthermore, I believe that the business’s strategic acquisitions, such as the acquisition of Truvalue Labs, may assist the company in tapping into new markets and segments in the expanding market.

In summary, the significant market expected growth presents a very high growth potential for GTX. Given its improved structure due to the Chapter 11 restructuring and its competitive standing in the market, I think the firm is in a good position to exploit the growing market. This viewpoint indicates that the company’s future is promising.

Risks

While investing in GTX may be an excellent decision, it comes with its risks, just like any other investment. Here are some of the potential risks;

Ability to execute growth successfully: The company may encounter difficulties or delays in achieving its strategic objectives or incur higher costs or lower returns than expected due to various risks such as integration challenges, regulatory hurdles, intellectual property disputes, competitive responses, or unforeseen liabilities.

Cyber security: If the firm has any cyber incidents that affect its systems or those of its customers, suppliers, partners, or third parties, it may incur reputational harm, operational interruptions, data or intellectual property loss, or liability claims.

My Verdict

Based on the information provided in this analysis, I find GTX is a total new reset brought about by the Chapter 11 restructuring. In my opinion, the company is now in a much better financial structure and financial footing. When blended with its competitive positioning and growth potential, I believe it will register tremendous growth in the future. Further, based on relative valuation metrics, GTX is trading below industry medians, attracting an overall valuation grade of A- by seeking alpha. This, in my view, shows that the company is trading at a discount, so I recommend the stock to growth-oriented investors at a discount.

Read the full article here