FRP Holdings, Inc. (NASDAQ:FRPH) recently noted quarterly double-digit net sales growth, and indicated, with a lot of cash, a significant number of future projects that may enhance future net sales. Also, with lending ventures promising double-digit internal rates of return, exposure to the growth of public infrastructure investments, and growing investments in data centers, FRPH appears in a very good position right now. I did see some risks from failed valuation of future development projects or certain geographic concentrations, however, FRPH does appear quite undervalued.

FRP’s Business Model, And Recent Double-Digit Quarterly Net Sales Growth y/y

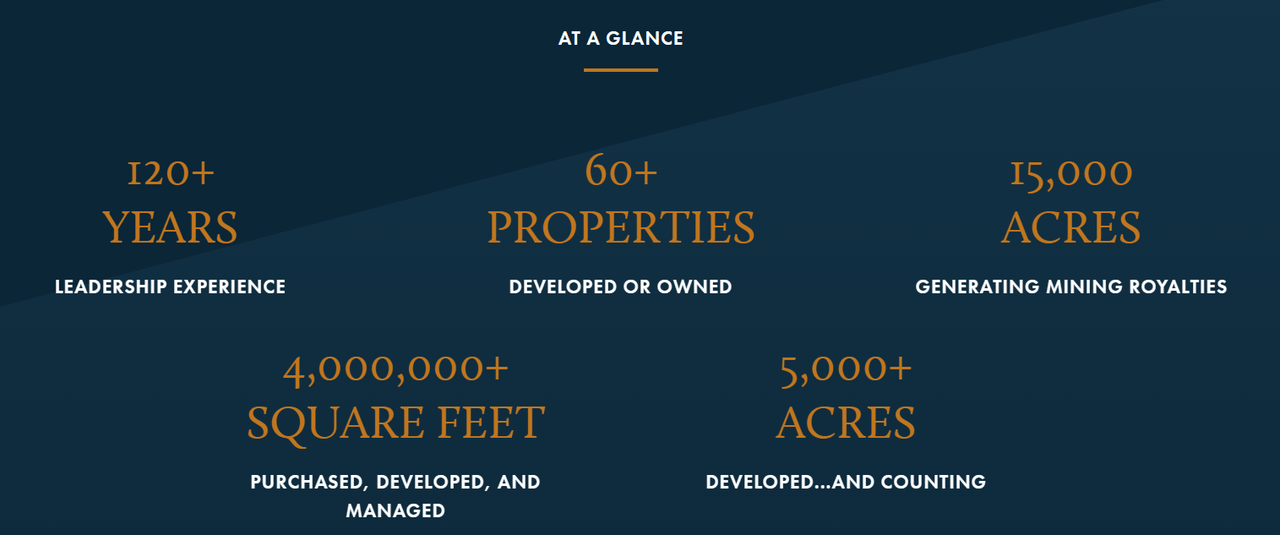

FRP is a company that focuses on activity within the real estate market. The operations are summarized in the rental and management of commercial activities of the company’s properties, rental and management of land with mining potential under the company’s ownership, the acquisition and development of different types of family homes as well as office buildings and projects of construction in general, and the activity on joint agreements for the acquisition, management, and administration of third-party establishments.

Source: Company’s Website

In recent years, the activity of some of the segments has shown historical profit records, which consolidates the company’s current strategy and its development into the future. Specifically, the activity on the acquisition and development of land for mining projects translated into the first acquisition in 10 years, purchasing all of Bland Property in Florida.

The activities are distributed in four segments of operations, and each segment corresponds to the treatment and form of development of the land. Among them we find the asset management segment, which mainly aims at the development of commercial projects through the rental of land for the construction of buildings, the mining rental segment, wherein FRP rents the land for the development of mining projects and receives income in relation to the activity of the tenants. Besides, there is the development segment, which is responsible for locating land on different development markets and carrying out the necessary analysis for its subsequent sale or rental to specific clients. Finally, we find the segment of joint agreements, in which the company seeks the stabilization of its activity in the development of real estate projects with other companies, mainly in the construction of buildings in residential areas.

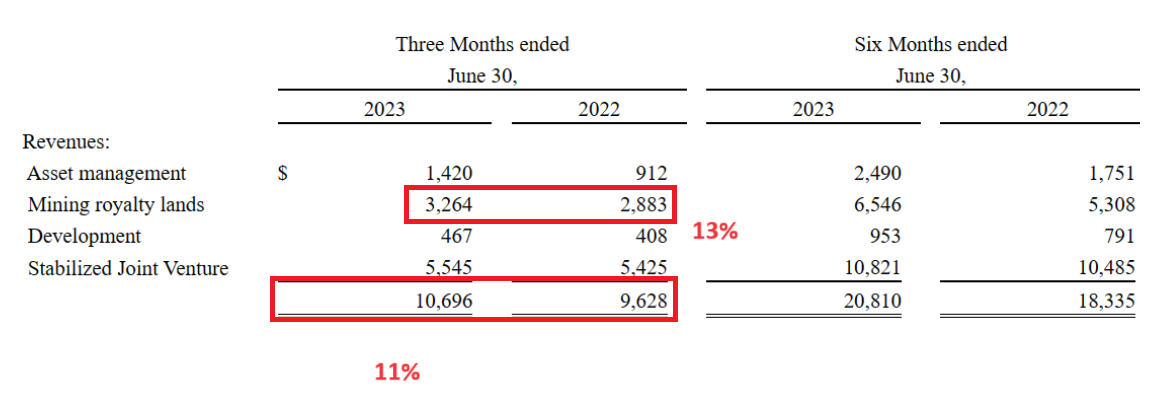

I believe that the recent numbers delivered for the quarter ending June 30, 2023 are quite impressive. The company delivered double-digit net sales growth y/y, and the minimum royalty lands business segment reported 13% sales growth y/y. In my view, these figures reflect a sufficient reason to have a close look at the current valuation of FRP.

Source: 2023 Investor Day Presentation

Balance Sheet

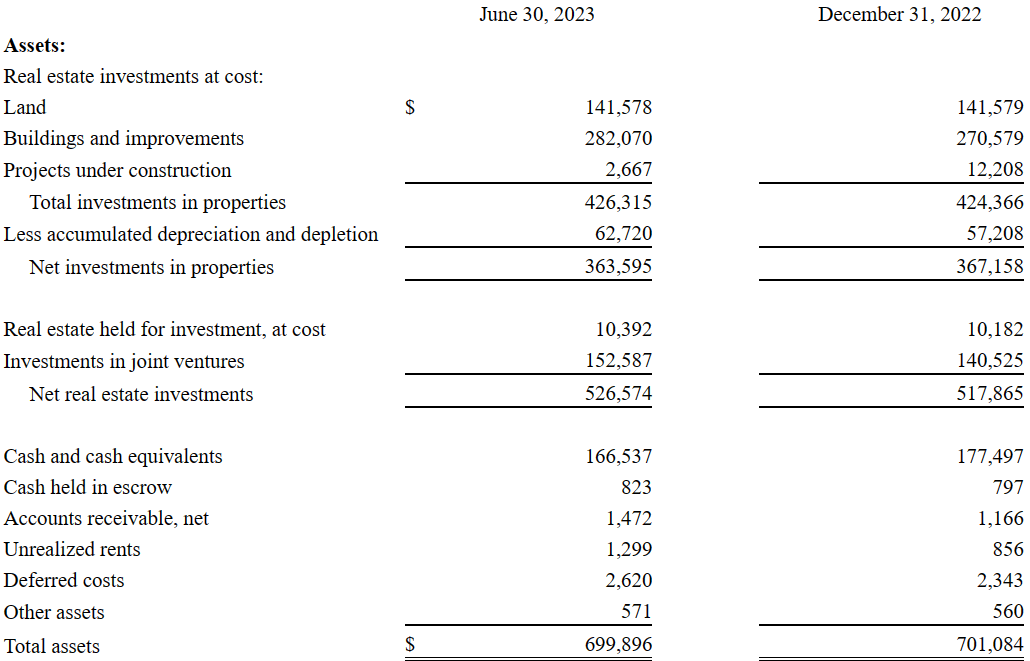

As of June 30, 2023, the company reported land worth $141 million, buildings and improvements close to $282 million, total investments in properties of about $426 million, and net investments in properties worth $363 million. Finally, with cash and cash equivalents of about $166 million, total assets stood at $699 million. I believe that considering the total amount of cash and the asset/liability ratio of more than 2x, FRP appears to have a solid balance sheet and a decent amount of liquidity to execute further product development.

Source: 10-Q

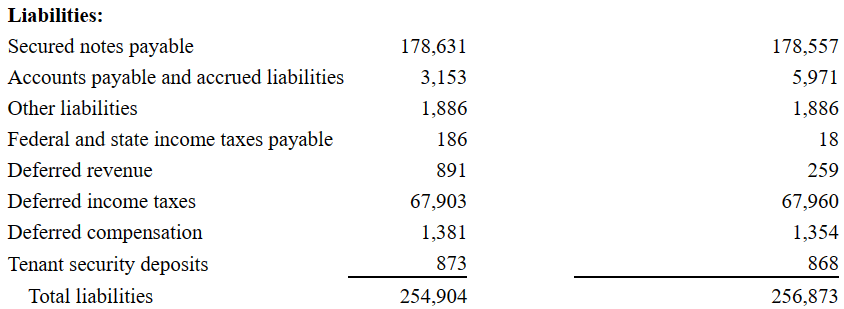

I believe that the list of liabilities does not seem worrying, not only because the total amount of debt is small, but also because the total amount of liabilities is not significant. More in particular, the company reported secured notes payable worth $178 million, accounts payable and accrued liabilities of about $3 million, deferred compensation of about $1 million, and total liabilities of close to $254 million.

Source: 10-Q

I studied a bit of the debt outstanding and the interest rates paid by FRP. They include a maximum of 1.50% over Daily 1-Month LIBOR, which would represent a total of close to 7%. I used these figures in my DCF model.

The interest rate under the Credit Agreement will be a maximum of 1.50% over Daily 1-Month LIBOR, which may be reduced quarterly to 1.25% or 1.0% over Daily 1-Month LIBOR if the Company meets a specified ratio of consolidated total debt to consolidated total capital. A commitment fee of 0.25% per annum is payable quarterly on the unused portion of the commitment but the amount may be reduced to 0.20% or 0.15% if the Company meets a specified ratio of consolidated total debt to consolidated total capital. The credit agreement contains certain conditions and financial covenants, including a minimum tangible net worth and dividend restriction. Source: 10-Q.

Source: Global-rates

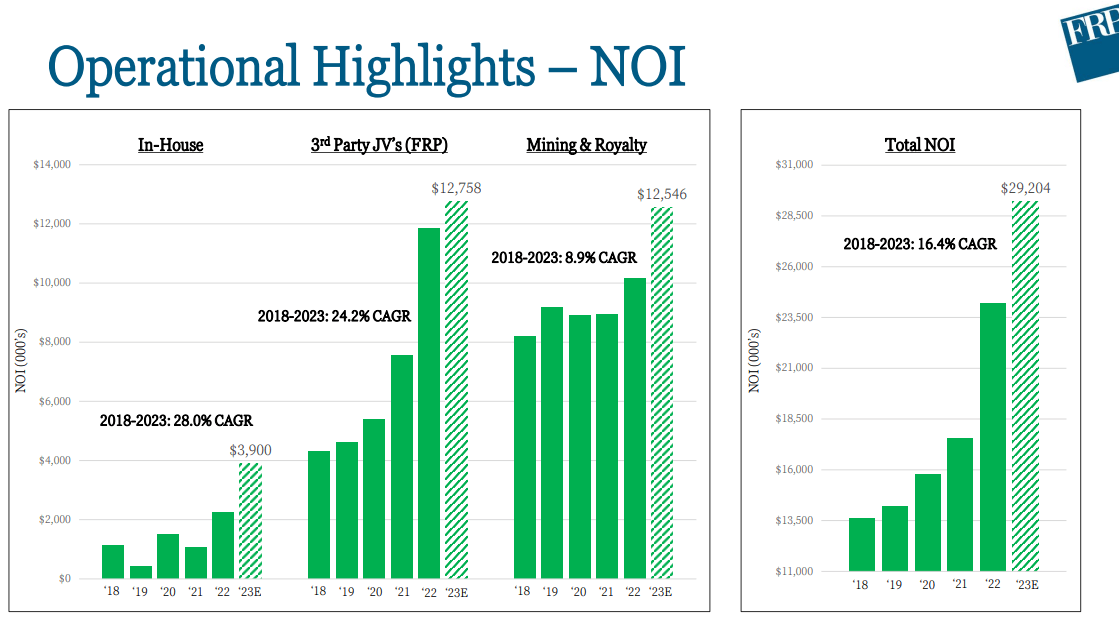

Recent Improvements In Net Operating Income Appear To indicate Valuable Know-how, Which May Continue To Play Major Role In Future Income Statements

I believe that further successful allocation of capital to properties and land for future investment in real estate projects that have long-term value appreciation will most likely bring FCF growth and net income growth. With many years in the same industry, I believe that the know-how accumulated and certain economies of scale will most likely help improve the FCF margins and NOI. In this regard, it is worth noting the most recent figures reported in a recent presentation, in which we could see significant NOI growth.

Source: 2023 Investor Day Presentation

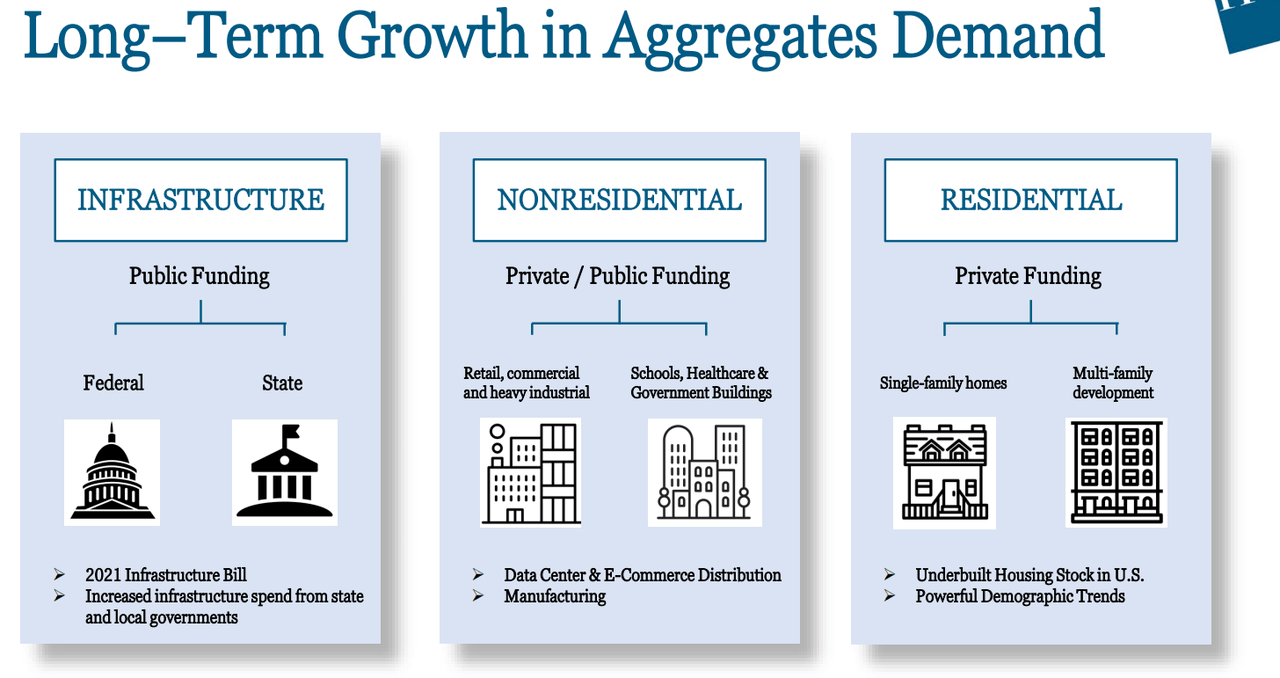

Recent Public Funding, Private Funding, Investments In Data Centers, Manufacturing, And E-Commerce Distribution Will Most Likely Have A Beneficial Effect on Net Sales Growth

I also believe that a significant number of FCF catalysts are coming from recent regulations like the 2021 infrastructure bill, increases in global investments in data centers, e-commerce distribution, and manufacturing. In my view, the new money coming to the industry will most likely accelerate future net sales growth. In this regard, management provided the following slide about increases in demand for the products of the company.

Source: 2023 Investor Day Presentation

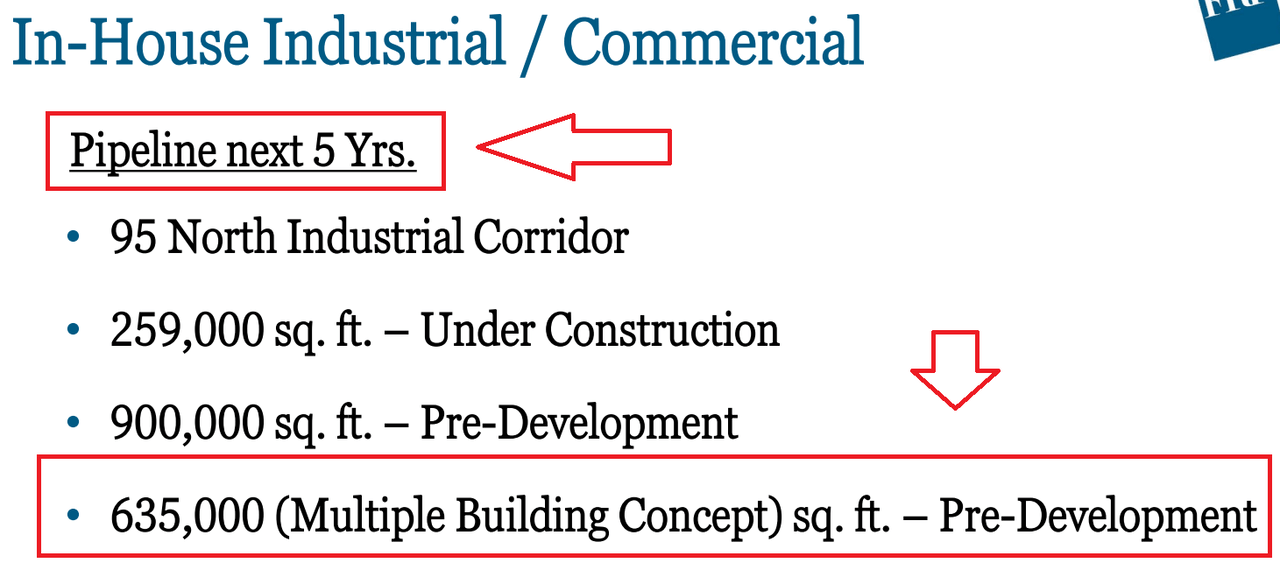

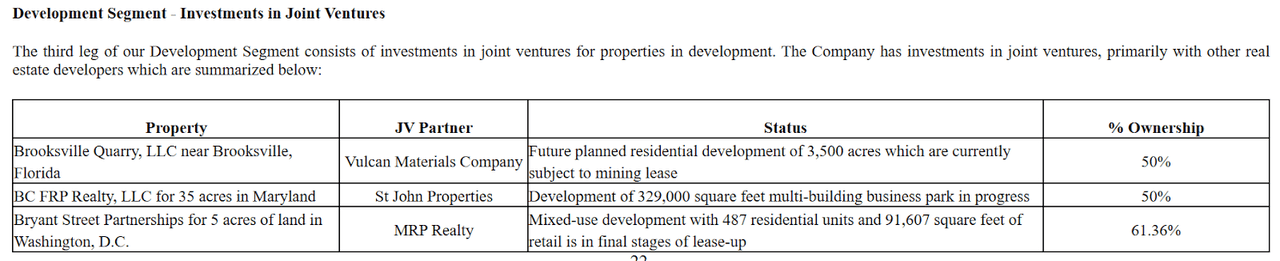

The Company Reports A Significant Number Of Industrial, Commercial, And Third Party Joint Ventures

I believe that incoming increases in capacity could bring further increases in revenue expectations. In this regard, it is worth noting that the company reported an impressive pipeline with 259k sq. ft. under construction, 900k sq. ft. in pre-development, and 635k sq. ft. under pre-development.

Source: 2023 Investor Day Presentation

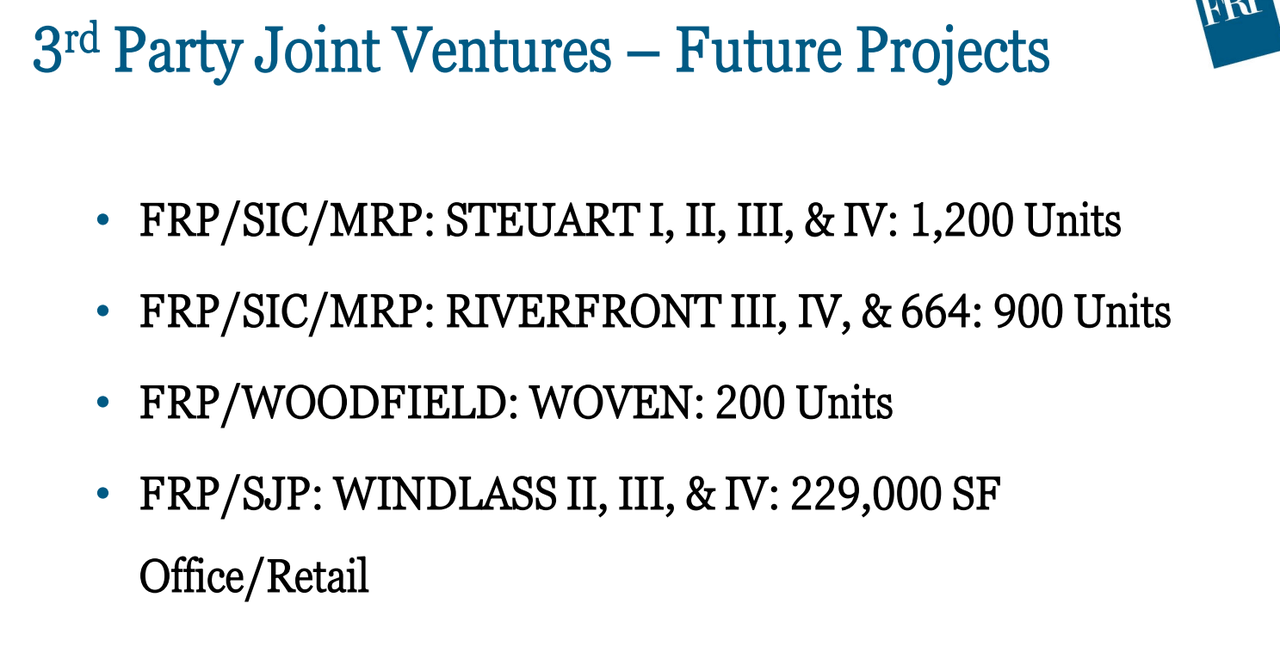

In addition, FRP reported a significant number of new units coming from execution in future projects executed with third parties. In my view, these projects will most likely bring revenue growth in the coming years.

Source: 2023 Investor Day Presentation

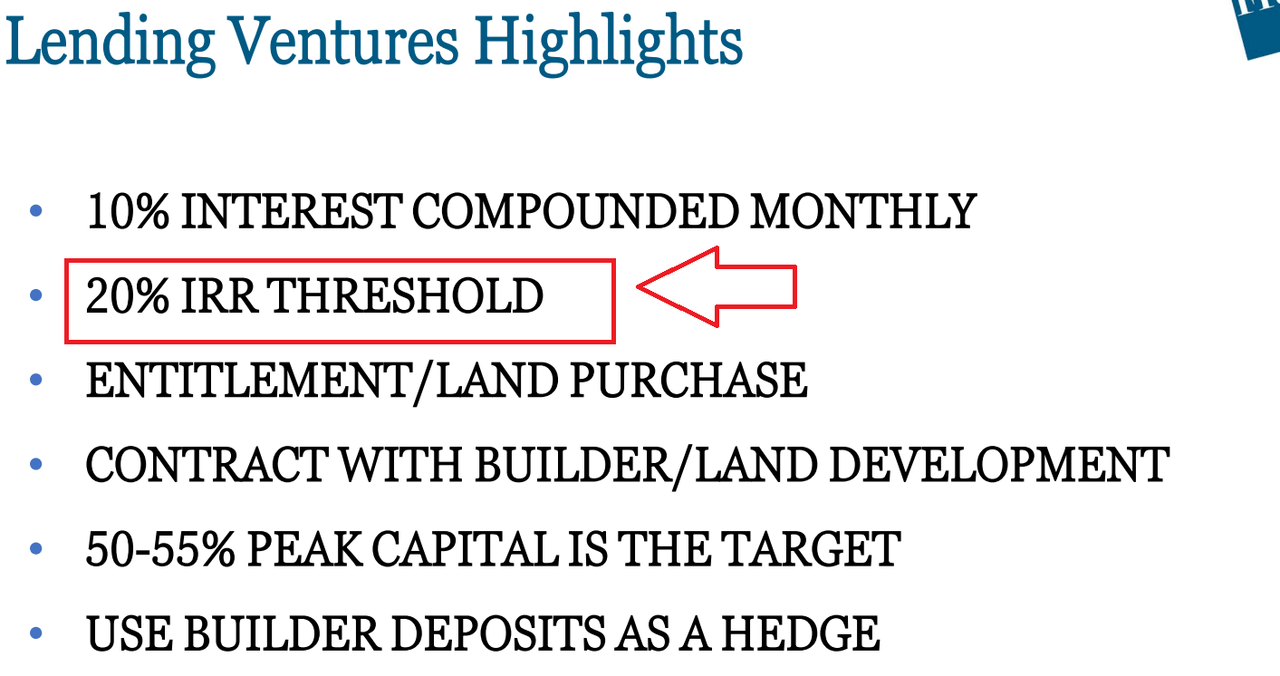

Lending Ventures Highlights Include Double-Digit Internal Rate Of Return

I think that investors would most likely be interested in the financial figures promised in a recent presentation. The lending ventures are expected to bring an internal rate of return threshold close to 20% and 10% interest compounded monthly. With these figures and sufficient communication about the returns obtained in the ventures, I believe that stock demand will most likely improve.

Source: 2023 Investor Day Presentation

Financial Valuation

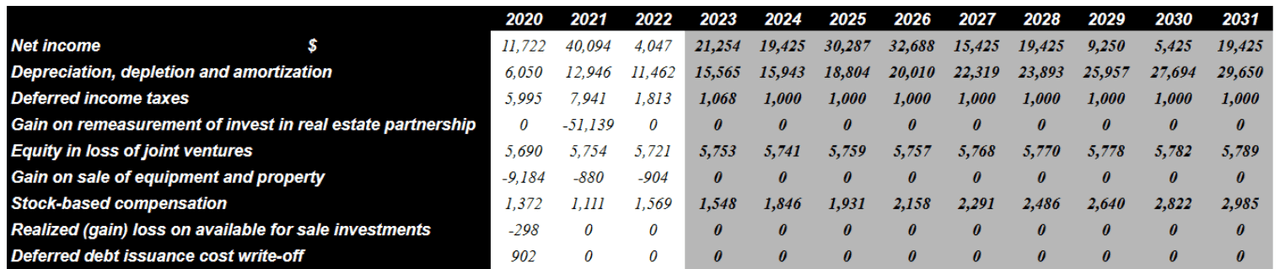

My financial model includes a 2031 net income close to $19 million, 2031 depreciation, depletion, and amortization worth $29 million, and deferred income taxes of about $1 million. I did not include gains on remeasurement of investment in real estate partnerships or gains on sale of equipment and properties because I believe that they are extraordinary events.

Source: My Financial Valuation

Besides, with stock-based compensation close to $2 million, changes in accounts receivable close to -$3 million, deferred costs and other assets of about -$12 million, and changes in accounts payable and accrued liabilities worth -$9 million, I obtained 2031 CFO of about $54 million. Finally, also taking into account 2031 capital expenditures of -$4 million, 2031 FCF would be close to $51 million.

Source: My Financial Valuation

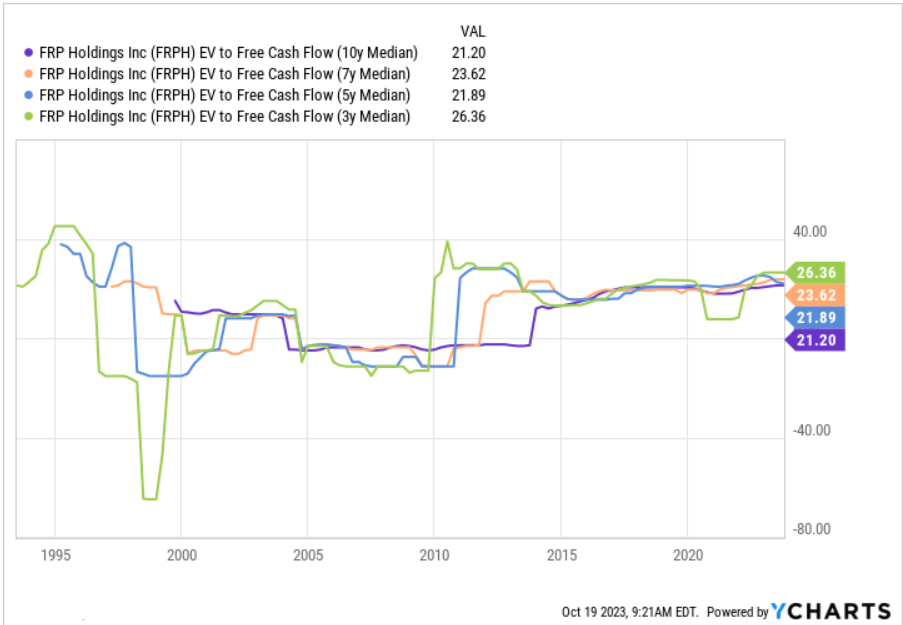

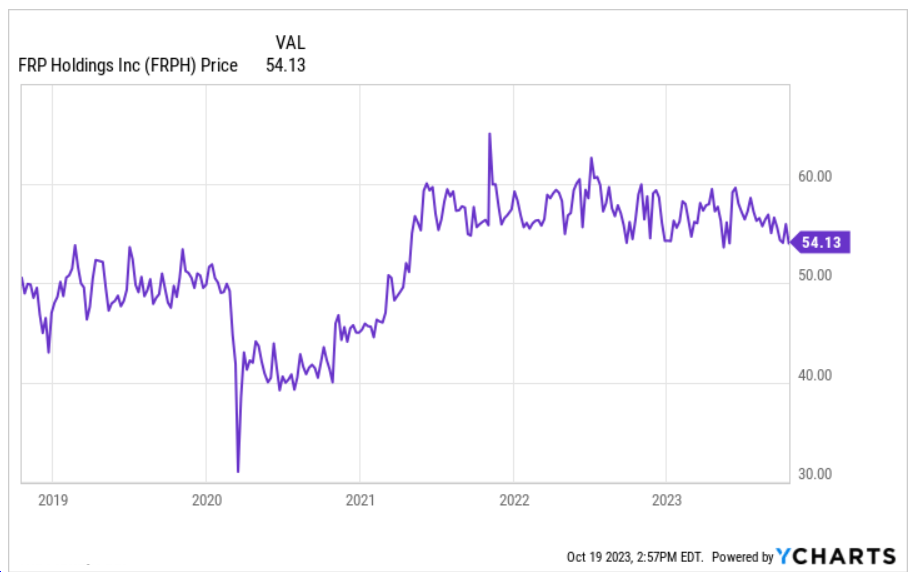

Considering previous EV/FCF multiples of close to 21x-26x reported in the past, I assumed exit multiples of about 21x-26, which I believe is a conservative assumption.

Source: YCharts

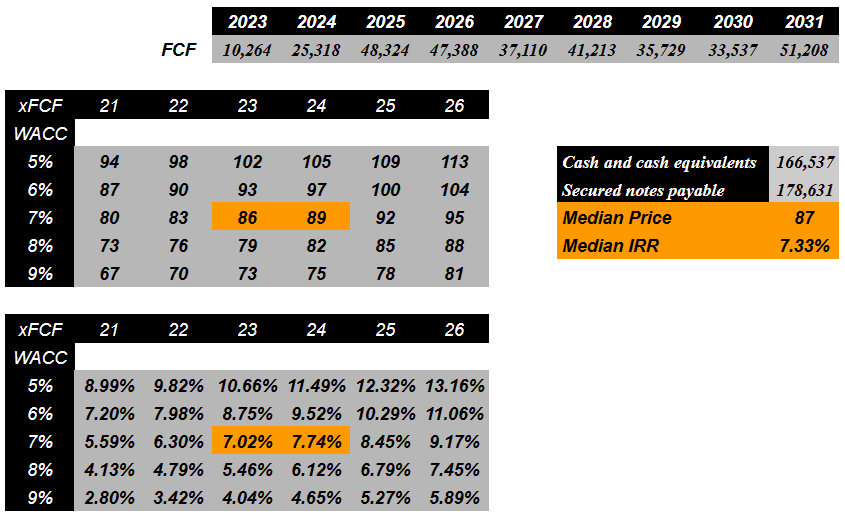

With FCFs close to $10-$51 million obtained between 2023 to 2031 and WACC between 5% and 9%, I obtained a forecast price of close to $67-$113 with a median forecast price of $86.57 per share. Besides, I obtained a maximum IRR close to 13% and a median internal rate of return of 7.33%.

Source: My Financial Valuation

The Valuation Offered By FRP Also Reveals That The Current Stock Valuation Is Quite Cheap

I believe that the valuation figures offered by management to investors are worth highlighting. In a sum of the parts analysis reported recently, the company obtained a valuation of close to $68-$78 per share and an equity valuation of $648-$744 million. My numbers are a bit more elevated than what the company reported, however taking into account the current stock price, FRP remains undervalued.

Source: YCharts

Source: 2023 Investor Day Presentation

Competitors

Like any real estate market with a high concentration of participants, competition is significant, and is given by companies with similar project developments as well as real estate owners and operators. Within this consideration, FRP has a small portion within the markets in which it participates, as it is not one of the main companies, but it has a considerably larger size than some other actors such as independent developers.

Risks

The first risk that we must point out is the low number of tenants on which the land owned by this company for mining developments is concentrated. An example of this is Vulcan Materials Company (VMC). In addition, Vulcan is one of the companies that currently, together with four others, completes the client portfolio for that segment.

In the Mining Royalty Lands Segment, we have a total of five tenants currently leasing our mining locations, and Vulcan Materials Company accounted for 23% of the Company’s consolidated revenues in 2022. An event affecting Vulcan’s ability to perform under its lease agreements could materially impact the Company’s results. Source: 10-K.

Source: 10-Q

Likewise, we must talk about the geographic concentration in the development of real estate projects in the Baltimore and Washington DC region as well as the economic conditions of this region as factors of direct dependence for FRP activity. Although a decrease in economic activity in this region would not be the only cause of risk since great growth in the same direction that allows the entry of new participants and generates greater competition is also a risk factor to be taken into account in this analysis.

On the other hand, this company has a great dependence on the activity of the construction industry, which tends to be cyclical. Therefore, in many cases, future forecasts are made with great factors of uncertainty. In addition, the inability to renew lease contracts or managing to generate new contracts for properties that currently do not have developments underway are likewise risk factors that should be considered.

Conclusion

FRP Holdings, Inc. delivered impressive quarterly figures, and noted a long list of future projects involving many new units and lending ventures highlighting a double-digit internal rate of return. Additionally, the company is expecting to benefit substantially from recent investments in public and private infrastructure as well as growing investments in data centers and e-commerce infrastructure. I do see risks from the geographic concentration in the development of real estate projects or failed forecasts about the price of development of projects. However, I believe that the stock appears quite undervalued.