I upgraded my thesis on Fortinet, Inc. (NASDAQ:FTNT) in late November 2023, as the market battered it following its disappointing third-quarter earnings release. I argued that FTNT dropped to its long-term support levels, which attracted the interest of dip-buyers, who likely saw a significant opportunity given the capitulation.

That thesis panned out, as FTNT has outperformed the S&P 500 substantially, powering ahead with a total return of nearly 30% since my previous update. Based on its November lows, FTNT gained more than 50% through last week’s highs, stunning the bearish investors with no faith in the wide-moat cybersecurity market leader.

It’s important to consider that Fortinet is a highly profitable SaaS leader, assigned a best-in-class “A+” profitability grade. While the slowdown over its core networking business likely led to the significant selloff, the market also quickly priced in the weaker growth momentum. Furthermore, management provided insights in an early December conference suggesting that Fortinet “anticipates a return to a normal environment for the firewall market.” As a result, while the high-growth phase spurred by the pandemic has likely dissipated, Fortinet remains well-positioned to consolidate its prowess in the fragmented cybersecurity market.

Accordingly, the company has a unified end-to-end SASE stack based on a “universal” approach. As a result, it allows customers to “deploy SASE on-premise or in the cloud based on their preferences.” Coupled with its core networking advantage, the company is confident it can continue gaining market share. Despite that, Fortinet also cautioned that switching costs are embedded, notwithstanding its market leadership. Management underscored that it still needs customers to “be willing to replace existing products for Fortinet to succeed in this regard.”

As a result, while the network effect and scale advantages likely benefit Fortinet and help secure its competitive moat, it also offers robust defense to critical players like Palo Alto Networks (PANW) and cloud-native leaders like CrowdStrike (CRWD). Given their embedded switching costs, it isn’t a surprise that cybersecurity leaders often trade at a marked premium relative to the market.

Fortinet is slated to report its fourth-quarter and FY23 earnings release on February 6. Investors are likely looking past 2024 as a reset year after a few years of rapid growth. As a result, investors are urged to look further ahead and assess whether FTNT can continue to recover its earnings growth momentum.

Accordingly, analysts’ estimates suggest a reacceleration in revenue and adjusted EPS growth for FY25. Fortinet is projected to post revenue growth of 15.1% in 2024, following an expected slowdown to 12.1% for FY24. Its adjusted EPS growth cadence is also expected to reaccelerate to 16.2% after a marked deceleration to 7.2%. As a result, I urge investors to look further ahead when assessing whether FTNT is still priced appropriately when considering their thesis.

FTNT is valued at an FY25 adjusted EPS multiple of 34.2x, well below its 10Y average of 47x. As a result, it seems likely the market has yet to price in its recovery fully, suggesting a further re-rating potential remains possible.

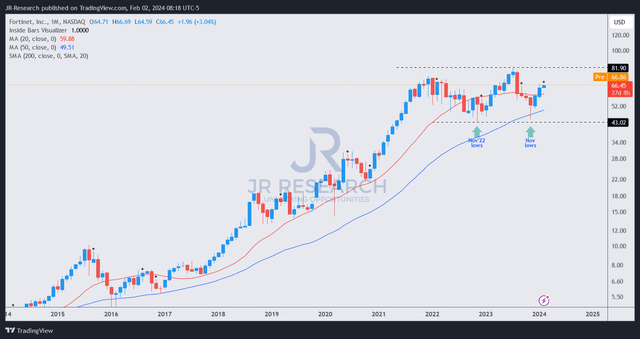

FTNT price chart (monthly, long-term) (TradingView)

Furthermore, FTNT’s long-term uptrend bias remained undefeated despite the steep selloff in 2023. In fact, the low $40 levels are well-supported, as dip-buyers returned aggressively to defend, seeing a highly attractive risk/reward profile as FTNT weak holders capitulated.

I assessed that FTNT’s long-term price action indicates an uptrend continuation bias is in play, although the most attractive buy levels are likely over.

With that in mind, I gleaned it’s apt for me to retain my bullish tilt on FTNT, although it’s no longer reasonable to maintain my Strong Buy rating.

Rating: Downgraded to Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here