flatexDEGIRO (OTCPK:FNNTF) continues to report a resilient operating performance despite the challenging market environment and its shares are undervalued.

As I’ve covered in previous articles, flatexDEGIRO is a growth play within the European financial services industry, but its business has suffered some setbacks over the past few quarters, including some regulatory issues.

This largely explains why its share price has moved sideways in recent months, even though its valuation remains quite cheap. In this article I analyzed the company’s most recent financial data and update its investment case, to see if it remains a compelling long-term play in the European financial sector or not.

Recent Earnings

flatexDEGIRO has some competitive advantages over its peers, namely due to its business model being the largest pan-European online brokerage company, with a presence in sixteen European countries. Over the past few months the company has decided to exit some markets, namely Norway and Hungary, as it was not able to reach the desired scale in those countries.

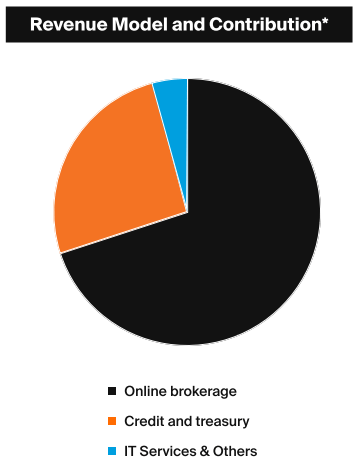

Most of its revenue comes from trading fees, while due to higher interest rates over the past year its revenue coming from credit and treasury has increased in a significant way, plus it also generates some revenue from IT services.

Revenues (flatexDEGIRO)

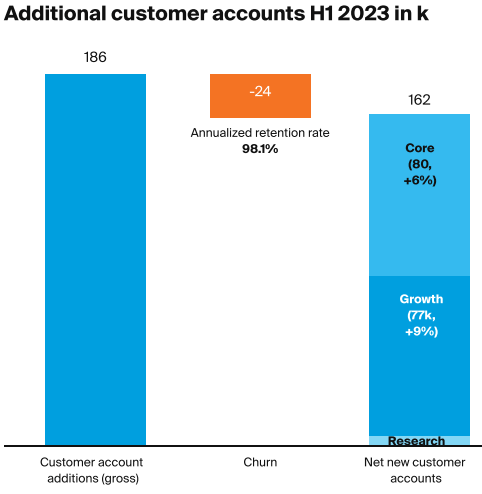

At the end of last June, flatexDEGIRO had close to €48 billion of assets under custody, an increase of 26% YoY, which is quite impressive given that it was a tough period for capital markets. Moreover, even during a market downturn the company was able to gain net new customers, which is quite positive and shows the strength of its business model, a trend that was maintained during the first six months of 2023.

Indeed, flatexDEGIRO was able to increase its customer count by 162k (net) during H1 2023, while its customer retention rate was above 98% during this period, boding well for its revenue and earnings growth ahead.

Net new customers (flatexDEGIRO)

Beyond gaining new customers, the company has also been able to report positive net inflows, of which more than 90% are invested, being an important contributor for higher assets under custody. In H1 2023, net inflows amounted to €2.9 billion, of which only €300 million were left in cash.

Despite these positive trends regarding asset, customer growth, and net inflows, customer activity has remained somewhat subdued in recent quarters, a trend that is widespread across the industry. After the bar market during 2022, customers remain largely on the sidelines, which is negative for flatexDEGIRO’s revenues that rely heavily on transactions.

Nevertheless, there has been some recovery in activity from a relatively small base, enabling the company to report higher revenues during the past couple of quarters. Moreover, interest income has increased considerably due to higher interest rates in Europe, being an important tailwind for revenue growth.

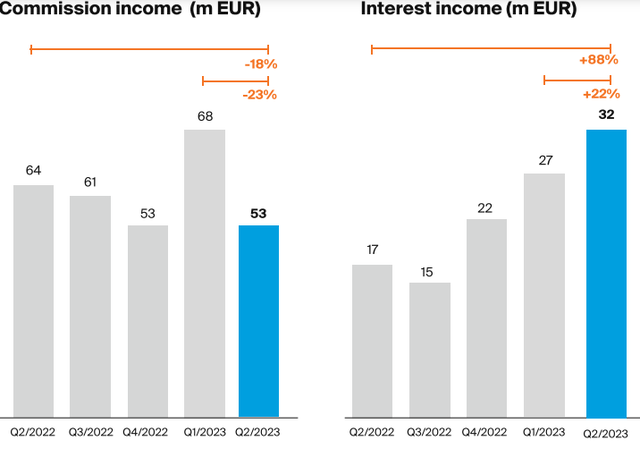

While commission income increased in Q1 2023, it reported again weakness in Q2, but this was to some extent compensated by higher interest income that has been on a growing trend in recent quarters.

Income (flatexDEGIRO)

As shown in the previous graph, commission income declined by 18% YoY in Q2 2023, a weak performance that can be justified both by weak customer activity and also by the company’s decision to increase fees in recent months. It’s likely that some customers may have switched to other brokers, such as Interactive Brokers (IBKR), given that flatexDEGIRO’s pricing is now much more in-line with its closest peers than it was before, especially in U.S. markets where its pricing was quite cheap.

flatexDEGIRO increased fees in some countries for U.S. and local trades, where it usually is also cheaper than compared to other markets, which is likely to have a negative impact on customer activity and consequently in commission income.

Fees (flatexDEGIRO)

Despite this increase in fees, flatexDEGIRO’s average commission per transaction has declined during Q2 2023 to less than €4 per transaction (from €4.17 in Q1), showing that customers adapt their trading activity based on fees and can switch brokers quite easily based on pricing.

Regarding expenses, flatexDEGIRO is also making some efforts to adapt its business to the current operating landscape, reducing marketing expenses to protect its business margins. Marketing expenses amounted to €25.5 million in H1 2023, a decline of 17% YoY, and are expected to decline even further in the coming quarters as the company already said that it wants to stop its sports sponsorship of two European football clubs.

This will have impact mainly in 2024, thus its annual marketing expenses will decline from about €49 million in 2022, to less than €30 million in 2024 (vs. expected €36 million in 2023). Despite these measures, its EBITDA was €29 million in Q2 2023, a decline of 22% YoY, as lower commissions have a higher impact than cost cutting in the past few quarters.

For the full year, flatexDEGIRO’s guidance remained stable compared to its initial February guidance, even though it now expects lower commission income (€240 million in 2023 vs. €265 million expected previously), which will be offset by higher interest income (€125 million vs. €100 million). In H2 2023, the company expects to have much lower marketing expenses plus it also has some one-off effects in H1, which is expected to lead to an adjusted EBITDA of €89 million in H2 2023 (vs. €64 million in H1 2023).

This shows that flatexDEGIRO is currently more focused on managing its profitability rather than seeking growth, even though it’s still trying to grow its business beyond its current offering. A good example is flatexDEGIRO’s recent partnership with Whitebox, to offer a wealth management solution in Germany.

This new offering was launched in July and will allow German customers to have in the same platform the access to an online broker and wealth management, through four different investment profiles. Management fees will range from 35-95 basis points, to be shared between flatexDEGIRO and its partner. This will allow flatexDEGIRO to have a new business line with a more recurring revenue profile, being based on overall assets under management instead of volume, which is positive for its business model and valuation in the future.

Regarding its regulatory issues, flatexDEGIRO has addressed most of Bafin issues about the company’s credit risk mitigation, which is now pending approval from the regulator. The company is confident that has improved its internal procedures and further action shouldn’t be needed, but until the regulator reviews the whole process, there is still some potential regulatory risk that shouldn’t be overlooked by investors.

Despite that, there has been some positive news on the regulatory front, given that flatexDEGIRO’s capital requirement was lowered by 75 basis points. This means that flatexDEGIRO now needs to hold less capital because the regulator considers its business to be more robust, being potentially positive for shareholders if in the future the company decides to return capital through share buybacks or dividends.

Going forward, flatexDEGIRO’s growth strategy is not expected to change much, being focused on organic growth and managing profitability at the same time. Its new offering in the wealth management segment was a surprise for me and I think it makes sense because it allows to gain more customers, especially among those who don’t want to manage their own investments and are willing to outsource that to professional investors, plus it diversified the company’s revenues and includes a more recurring profile, which is positive over the long term.

If this new offering is successful in Germany it’s quite likely that flatexDEGIRO will offer it in more countries, and potentially this could represent a sizable part of its business, being another growth source over the next few years.

Conclusion

flatexDEGIRO has reported acceptable results for the first half of 2023, even though the operating environment continues to be tough due to relatively muted customer activity. Despite that, the company is showing good progress on important metrics, such as customer and asset growth, which should lead to higher revenues down the road. Its new wealth management offering is also another step in the right direction and can be an important growth source in the future, being complementary to its existing business.

Regarding its valuation, flatexDEGIRO continues to trade quite cheaply, given that it’s currently trading at 11.8x forward earnings, while its peer average is close to 16x, thus it remains an interesting long-term growth play within the European financial sector.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here