At a Glance

Building on my prior bullish stance, Aldeyra Therapeutics (NASDAQ:ALDX) finds itself at an inflection point. The company’s Q2 2023 earnings report reveals a significant 52% cut in R&D spending, hinting at a shift from drug development to market readiness. Financially, with a $151.7M cash reserve and an estimated 40-month runway, Aldeyra has cushioned its operational risks. The impending PDUFA decision for reproxalap, their lead candidate targeting a $6.2B dry eye disease market, could serve as a seismic catalyst. Despite a capitalization shrink to $382.63M and lagging stock performance, Aldeyra remains a “Buy,” especially for investors eyeing long-term value and unfazed by sector-specific volatility.

Q2 Earnings Report

To begin my analysis, looking at Aldeyra’s most recent earnings report for Q2 2023, a striking feature is the significant drop in Research and Development (R&D) expenses from $14.6M to $7.0M year-over-year. This 52% reduction mainly stems from decreased external clinical development and drug manufacturing costs, partially offset by hikes in personnel and preclinical expenses. It suggests Aldeyra may have advanced key assets past costly development stages. On the other hand, General and Administrative (G&A) expenses saw a modest rise to $3.4M, attributed mainly to increased legal and personnel expenditures. The net other income improved by $1.5M, primarily due to higher interest income. Overall, the substantial decline in R&D expenses signals a pivotal shift in resource allocation, possibly towards market readiness or pre-commercial activities.

Cash Runway & Liquidity

Turning to Aldeyra’s balance sheet as of June 30, 2023, the company has $151.7M in cash and cash equivalents; marketable securities are not present. The net cash used in operating activities over the past six months is $22.8M, giving us an estimated monthly cash burn of approximately $3.8M. With this, Aldeyra has a cash runway of approximately 40 months, assuming similar spending rates. Note that these estimates are based on historical data and may not accurately predict future performance.

On liquidity and financing: Aldeyra holds a moderate level of long-term debt, approximately $10.1M net of the current portion, posing some leverage risk but not immediately threatening the company’s stability. Given the cash runway and existing debt structure, securing additional financing in the near term seems plausible but not urgently necessary. This could come in various forms, such as equity issuance or debt, but the company has the leverage to negotiate favorable terms. These are my personal observations, and other analysts might interpret the data differently.

Capital Structure, Growth, & Momentum

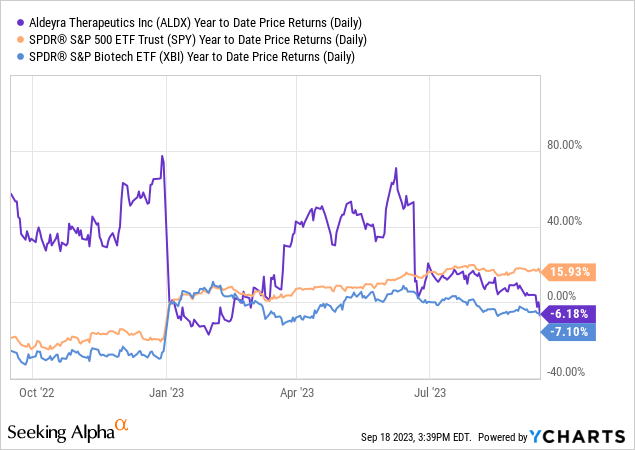

According to Seeking Alpha data, Aldeyra exhibits a comfortable capital structure with a market cap of $382.63M, minimal debt, and a robust cash position. The dramatic YoY revenue projection from $571.10K in 2023 to $41.46M in 2024 suggests a company at an inflection point, transitioning from R&D to a commercial phase. Analysts project further revenue acceleration to $140.82M by 2025. Despite these bullish signals, stock momentum has been lackluster, underperforming the S&P 500 with a one-year decline of 0.91%.

Aldeyra’s Reproxalap Approaches Pivotal FDA Milestone

In 2023, Aldeyra is approaching several decisive catalysts that will shape its clinical and regulatory trajectory. Most notably, the NDA PDUFA date for reproxalap, intended for dry eye disease, is slated for November 23, indicating a pivotal moment for the company’s lead asset. Additionally, a Type C meeting with the FDA will take place in H2 2023 to discuss the clinical development roadmap for proliferative vitreoretinopathy. Alongside this, Aldeyra anticipates releasing top-line data from multiple Phase 2 trials: atopic dermatitis, idiopathic nephrotic syndrome, and Sjögren-Larsson Syndrome, all expected in H2 2023. Lastly, the company is planning to kick off a Phase 2 study for moderate alcohol-associated hepatitis in the same period.

Reproxalap, with its unique reactive aldehyde species [RASP] inhibitory mechanism, targets both dry eye disease (DED) and allergic conjunctivitis. This dual applicability has the potential to capture a significant portion of the DED market, projected to hit $11.26 billion by 2030, and the allergic conjunctivitis market, estimated at >$2 billion annually. Current therapies, such as cyclosporine and corticosteroids, often bring along safety concerns or limited efficacy, leaving an unmet need for an estimated >16 million diagnosed DED patients in the U.S. alone.

The frequent co-occurrence of DED and allergic conjunctivitis – estimated at 31-36% comorbidity – exacerbates symptom severity, complicating patient management. Reproxalap’s RASP inhibition is designed to neutralize aldehydes, implicated in ocular inflammation and irritation, thus offering a treatment potentially more aligned with the underlying pathophysiology of these conditions. Its dual-targeting capability could streamline patient treatment regimens, and its novel mechanism may reduce reliance on multiple medications, decreasing the risk of side effects.

If reproxalap gains FDA approval, its first-to-market advantage as a RASP inhibitor would not only set a new standard of care but also position Aldeyra strongly in competitive market landscapes. The upcoming PDUFA date in November 2023 serves as a pivotal milestone for reproxalap, and by extension, Aldeyra’s strategic market positioning.

My Analysis & Recommendation

In conclusion, Aldeyra Therapeutics finds itself on the precipice of a transformative phase. The upcoming PDUFA decision on reproxalap could materially alter its market position and investor sentiment. The company’s financial health, characterized by a $151.7M cash balance and a manageable cash burn rate, underscores its preparedness for a robust market entry should reproxalap receive FDA approval. Importantly, Aldeyra’s reduction in R&D expenses and reallocation of resources imply a shift towards commercialization, suggesting that the management is taking preparatory steps for a smooth market transition.

However, there are clear hurdles. For one, the dry eye disease (DED) market is highly competitive, teeming with established treatments like cyclosporine and corticosteroids. The challenge lies in convincing physicians to change prescribing habits, a task that’s often more arduous than winning FDA approval. Additionally, investors should watch the speed of physician uptake, as any initial lag could temper revenue forecasts.

Strategically, the company’s financial stability provides it with leverage to negotiate favorable terms for additional financing, although this is not an immediate need. This strengthens the balance sheet further, insulating against the cash-intense process of marketing a new drug post-PDUFA.

Taking the above factors into account, I maintain a “Buy” recommendation on Aldeyra. The company’s strong financial position ahead of the PDUFA decision, coupled with a groundbreaking drug candidate in reproxalap, makes it a compelling investment for those willing to navigate the inherent sector risks. Should reproxalap receive FDA approval, Aldeyra not only captures first-mover advantage but is also poised for significant revenue acceleration, given the vast unmet need in DED and adjacent markets. The current market capitalization of $382.63M suggests that significant upside potential exists if the company successfully navigates the commercialization process.

The next few weeks and months promise to be highly instructive. Investors would do well to watch for the PDUFA decision and scrutinize early indicators of physician adoption post-approval, as these will be the true barometers of Aldeyra’s capacity to convert clinical promise into market performance.

Risks to Thesis

Although my analysis supports a ‘Buy’ recommendation for Aldeyra Therapeutics, there are noteworthy risks that could challenge this stance:

-

Regulatory Uncertainty: The FDA’s PDUFA decisions are unpredictable. A negative outcome would substantially impact stock value.

-

Physician Adoption: Even with FDA approval, reproxalap faces the hurdle of altering entrenched prescribing behaviors. Slow adoption would hamper revenue growth.

-

Competition: Incumbent drugs like cyclosporine enjoy strong physician loyalty, potentially slowing reproxalap’s market penetration.

-

Overemphasis on R&D Cut: The 52% YoY reduction in R&D spending might be seen as readiness for commercialization. Alternatively, this could signal underinvestment in future pipeline development, a long-term concern.

-

Cash Burn: While the 40-month cash runway seems sufficient, unexpected clinical or commercial setbacks could accelerate the burn rate, compelling dilutive financing.

-

Lackluster Stock Momentum: The stock’s underperformance against the S&P 500 signals market skepticism, which could hinder short-term gains.

Read the full article here