Investment thesis

I initiate my coverage of The Estée Lauder Companies Inc. (NYSE:EL) with a Sell rating following my in-depth research of the company and the underlying beauty and cosmetics industry.

Estee Lauder, a renowned leader in the cosmetics industry, boasts a market cap of $50 billion and a rich history of providing high-end cosmetics and skincare products. The company’s impressive portfolio of brands, global presence, and growth in key markets, such as skincare, makeup, fragrance, and haircare, have driven consistent revenue growth, with a CAGR of 6% from 2012 to 2022.

Nonetheless, Estee Lauder’s overreliance on the skincare segment raises concerns about its risk profile. With 51% of sales and a staggering 83% of operating profit coming from skincare, the company’s financial performance is highly sensitive to this segment’s performance. Diversification within the beauty industry is often considered a more balanced approach, protecting against fluctuations in any segment.

Estee Lauder’s recent challenges are notably linked to the decline in the Asian travel retail market and the underperformance of the skincare segment. While the company is expected to benefit from a recovering Asian travel retail industry, it may still face headwinds from factors such as a consumer spending slowdown and increased competition.

The company’s margin profile is another concern, with gross margins declining over the years and hitting decade lows. Operating expenses, particularly in advertising and marketing, have grown significantly. These challenges impact the company’s profitability and pose obstacles to margin expansion in the future.

Looking ahead, Estee Lauder’s near-term and long-term outlooks suggest only moderate growth. While the recovery in travel retail and improving gross margins are expected, ongoing challenges in the industry and a lack of significant margin improvement may hinder the company’s ability to achieve its historical valuation premium.

With shares currently trading at a P/E ratio of over 35x and the risk-reward profile appearing unfavorable, investors are advised to exercise caution. The stock’s current valuation seems to factor in a sales and margin recovery that may not fully materialize, making it less attractive compared to peers like L’Oréal (OTCPK:LRLCY), which offers similar growth prospects with a lower risk profile. A conservative price target of $112 is suggested, reflecting an 18% downside risk. For now, a “sell/avoid” rating is recommended. It may be prudent to revisit Estee Lauder as the situation evolves, as there is clearly a lot of value in this company, which is just not materializing today.

The Beauty and Cosmetics industry offers plenty to investors

The cosmetics industry is a fascinating one and a very enticing investment opportunity. The industry was valued at over $260 billion as of the end of 2022, according to Grand View Research, and is part of the beauty market—defined as skincare, fragrance, makeup, and haircare — which generated approximately $430 billion in revenue in 2022 and should grow at a CAGR of 6%, according to McKinsey.

The industry has desirable qualities, including relative resilience, a solid growth outlook, strong brand recognition, a massive target audience, and impressive innovation. The cosmetics industry serves a broad and diverse customer base, including different age groups, genders, and cultural backgrounds. This diversity can create opportunities for companies to introduce a wide range of products and target specific demographics, growing the TAM.

The cosmetics industry is expected to show solid growth for the remainder of the decade. According to research from Grand View Research, the cosmetics industry is expected to grow at a CAGR of 4.2% through 2030, driven by factors like population growth, urbanization, and increasing disposable incomes. Other important growth drivers also include increasing consumer interest in skincare products and the aging population.

And while this is no very exciting growth as we see from many technology verticals, the industry has shown impressive consistency, even during economic downturns. People tend to continue purchasing beauty and personal care products, as they are often seen as essential to daily grooming and self-esteem, regardless of the economic climate.

Furthermore, research points out that large and well-known brands will continue to dictate and lead the market, giving the industry leaders an edge over the competition in terms of product innovation and pricing as these brands receive strong brand recognition and customer loyalty. This brings me to one of the industry’s leaders – Estee Lauder – which reports sales in 4 categories: the earlier mentioned skincare, fragrance, makeup, and haircare, projected to grow at a CAGR of 6% annually.

Yet, before we get into this market leader, it is worth mentioning that the cosmetics industry is also highly competitive, with many players vying for market share. Additionally, regulatory and safety concerns, changing consumer preferences, and the potential impact of economic and health crises can pose challenges for those same industry participants. Success is no straightforward process, nor has it been that for Estee Lauder in recent years.

Estee Lauder – A beauty and Cosmetics giant

With a market cap of $50 billion and $15.91 billion in annual sales as of its most recent fiscal year, Estee Lauder is one of the world’s largest cosmetics and beauty companies, even after losing close to 50% of its value YTD. The company is a well-known American multinational cosmetic and skincare company. The company is headquartered in New York City and has grown to become one of the world’s leading manufacturers and marketers of high-end cosmetics and beauty products. Over the years, Estée Lauder has established itself as a leader in the luxury beauty industry and is associated with quality and prestige.

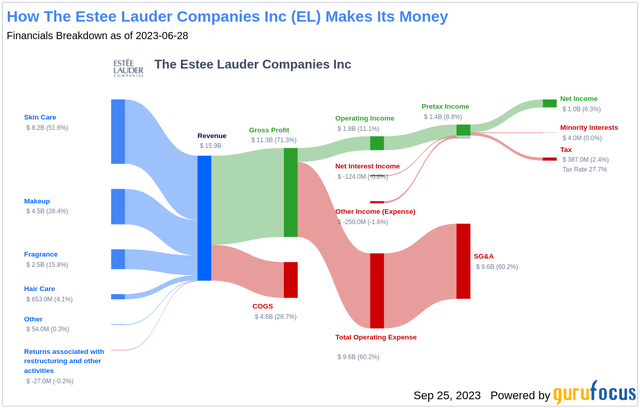

Estée Lauder’s product line includes various well-known brands, such as Estée Lauder, Clinique, MAC, Bobbi Brown, La Mer, Aveda, Jo Malone, and many others. These brands offer a wide range of cosmetics and skincare products, catering to a diverse customer base.

Estee Lauder brands (Estee Lauder)

The company has a strong presence in department stores, specialty retailers, and its own standalone stores, in addition to its e-commerce operations. Estée Lauder is recognized for its innovation in skincare and cosmetics, and it has a global presence, serving consumers in over 150 countries.

As stated before, the company operates and reports in four categories: skincare, makeup, fragrance, and hair care. Crucially, the company holds strong positions in at least three of its leading markets, dominating the industry together with peer and competitor L’Oréal.

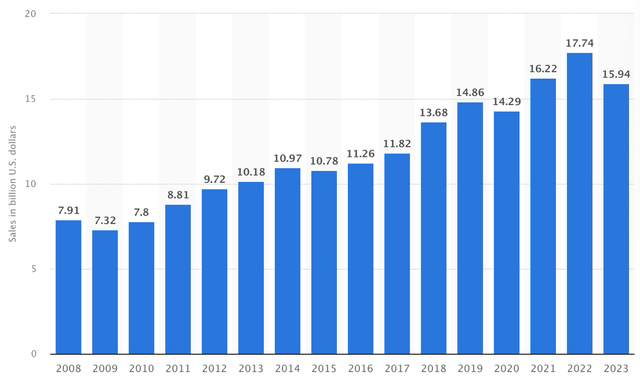

Furthermore, the company has been expanding its market share in every single one of its end markets, highlighting its impressive performance in recent years. This, combined with solid underlying industry growth and acquisitions, allowed the company to grow revenue at a CAGR of 6% from 2012-2022, which is a respectable performance.

Estee Lauder revenue (Statista)

Nowadays, the company holds a 20% market share in the makeup industry and end market. In haircare and fragrance, its market share currently sits around the 1.5% and 9% mark, respectively.

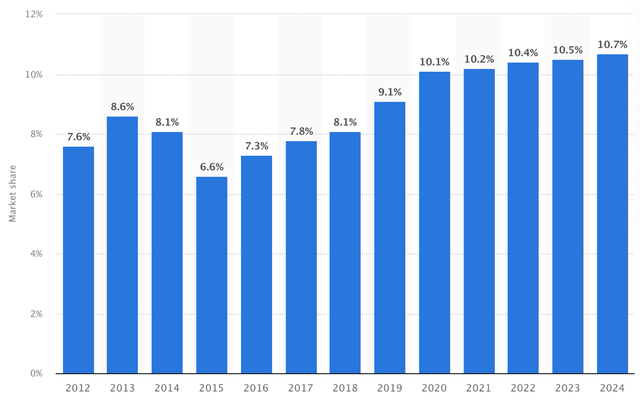

In its largest market and segment – Skincare – Estee Lauder holds a market share of slightly over 10% after successfully expanding it from just 6.6% in 2015. The global skincare market, a primary growth driver of the overall cosmetics industry, is expected to grow at a CAGR of 6.2% through 2030, driven by the aging population and growing attention to healthy and moisturized skin among younger generations.

Estee Lauder skincare market share (Statista)

Also, the Skincare market generally allows for very high margins due to low input and production costs, as is also reflected in Estee Lauder’s financials, with its skincare segment being its most profitable one. I am, therefore, quite optimistic about the company’s exposure to this industry.

Estee Lauder is overly dependent on its Skincare segment, increasing the risk profile and impacting the outlook

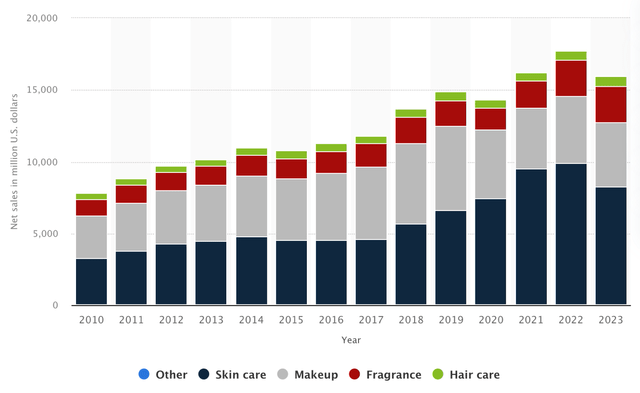

Yet, I am not so positive about its over-exposure to the skincare market. The latest financial results show that the company derives 51% of its sales from the skincare segment, down from 56% in the previous year. This is already quite a lot, but what is even more concerning is that 83% of the operating profit is generated by the skincare segment, making the company’s bottom line result highly sensitive to the performance of a single industry.

Estee Lauder revenue by segment (Statista)

I believe a well-diversified beauty industry giant should have no single segment accounting for over 50/55% of the top or bottom line. Even when an industry or end market has a significant growth outlook, I am uncomfortable with a company having too much exposure and little diversification as it creates more risk.

For example, its larger peer and primary competitor, L’Oreal, has no operating segment accounting for over 40% of its sales. Even in the cosmetic branch itself, no single end-market accounts for over 41%, with skincare being the largest at 40.1%. This highlights a far better-diversified business compared to that of Estee Lauder and, therefore, a far better risk profile.

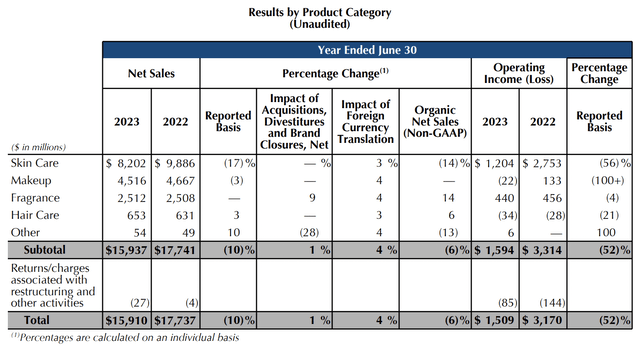

And I am not even exaggerating here. Just how much of an impact Estee Lauder’s weak sales diversification can have is highlighted by its most recent financials. For its fiscal FY23, Estee Lauder reported a 10% revenue decline, fueled by a 17% decline in sales from the skincare segment, accounting for 93% of the YoY decline in dollars. In terms of profit dollars, the skincare segment accounted for 90% of the decline, causing a 52% decrease in operating income.

What I am trying to highlight here is that the strategy to go all-in on the high-end skincare market over the last decade, which has helped the company grow, has now caused it to be overly exposed to a single industry. Once this one underperforms as it has done in the last year, this has a massive impact on the company’s reported financials as other segments are simply too small to offset this.

Will the industry recover? Yes, it likely will, as the underperformance is partly due to weakness in travel retail, but I am still unsure if it can drive significant growth again for Estee Lauder. The current slowdown in consumer spending is impacting the near-term performance of its leading high-end brands, similar to the slowdown we are seeing for other luxury giants like LVMH. Furthermore, the growing number of cheaper alternatives on the market is also not making life for Estee Lauder any easier in the longer term. The company has been facing increasing competition in recent years, slowing down its rate of market share gains, and while its brand recognition will protect it somewhat from the competition, I do not see any more market share gains in the medium term (nor significant market share losses, though), in part due to the higher cost of living expected to persist, resulting in consumers looking for more cost-effective alternatives.

The one positive I see for Estee Lauder to help it maintain its share in the skincare industry is its leadership position in anti-aging skin products, which are increasing in popularity globally. Estee Lauder is a frontrunner in this product category as clinical and preclinical results demonstrate scientific innovation and leadership across emerging skin health and anti-aging areas. The company’s continued innovation on this front will support its market share.

However, overall, I expect the company’s over-dependence on the skincare industry, especially for its profits, to hold it back in the near to medium term while also adding to its risk profile.

The dependence on travel retail and the Chinese consumer has taken its toll in recent years.

Jumping right in there: the company’s financial performance over the last year has not been great, as highlighted by the close to 50% drop in the share price YTD. In August, JPMorgan analysts called the bottom in Estee Lauder shares (shares moved further down in the two following months, declining another 15%). According to JPMorgan analysts and several others, this is all about the recovery of the Asian travel industry.

Looking at the last few years, we can see the company was impacted by the COVID-19 crisis in 2020 as sales dropped slightly due to closed retail locations and travel limitations. However, the company (and the underlying industry) held up well, allowing Estee Lauder to report new highs in 2021.

However, while Estee Lauder did relatively well during the COVID-19 crisis, we can’t say the same about its performance over the last year, with sales down 10%, although up 4% organically.

FY23 financial data (Estee Lauder)

While the company was able to drive mid-single-digit growth in retail sales in its fiscal FY23, overall sales were still down 6% YoY as gains across most geographies were offset by Asian travel retail, which caused a 34% YoY organic decrease in global travel retail sales as Asian (mostly Chinese) travel activity is still down from the covid-19 lockdowns and is only slowly recovering. With travel retail being an important growth driver and large segment for Estee Lauder (now down to 20% of revenue), the impact of this segment lagging is significant.

Also contributing to this slowdown was “daigou,” which refers to reduced discounts to curtail wholesale purchases. In May and June, retail sales trends deteriorated and turned steeply negative following the enforcement actions by the Chinese government to control daigou activity, as these simply led to fewer sales. However, this should recover in time, and I am not expecting this to have any lasting effects, which should, in time, help the recovery of the Asian travel retail performance.

The Asian travel industry now seems to be slowly recovering, which, according to JPMorgan analysts, should significantly improve results over the next two quarters. This should be helped by strong continued momentum in the EMEA, Latin America, and a recovering Asia Pacific market (excluding travel retail), where organic sales growth improved from 7% in the third quarter to 36% in the fourth quarter, led by mainland China. Fundamentally, the business isn’t doing so badly in terms of sales, and once the Asian travel retail market recovers, this should boost growth.

However, despite such a recovery, it is safe to assume growth to stay somewhat subdued due to Estee Lauder also facing strict inventory control measures from retailers as consumer spending has slowed and remains weak. Even luxury giant LVMH (OTCPK:LVMUY), which was able to report strong growth for the last couple of years, is now seeing growth slow down as the demand environment for high-end products is deteriorating. This is not giving me more confidence in the recovery for Estee Lauder, which sells high-end discretionary items. Therefore, despite the Asia recovery, I am not expecting blowout results in its fiscal FY24.

Based on everything discussed so far, short-term growth of high-single digits and long-term growth of closer to mid-single digits seems likely and a reasonable scenario to go with.

Yet, while sales growth across most regions might be looking good, the lagging performance can be attributed to more than just the lagging Asian travel retail market and the underperformance of the skincare segment (which are somewhat related). Pretty much all analysts see a recovery here as the driver of the bull case, but while it will help results in the short term, it won’t be enough to impress investors and convince them to pay 38x earnings for single-digit growth ahead. Even based on very optimistic FY25 EPS estimates by Wall Street analysts, shares still trade at 25x earnings, valuing it above larger and stronger performing peer L’Oreal and consumer staple giants like PepsiCo (PEP) and Mondelez (MDLZ), which offer similar growth at far better risk profiles.

Margin developments are worrying

As highlighted above, Estee Lauder’s near-term performance is weak, and its longer-term outlook is far from impressive. That brings me to the margin profile, which leaves much to be desired.

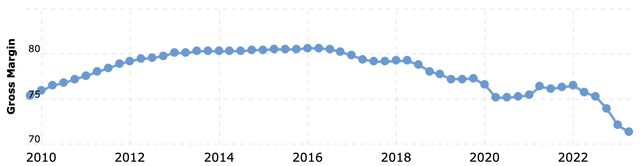

The gross profit margin was down 440 basis points YoY in FY23, highlighting the company’s margin deterioration, mainly due to the slower-than-expected recovery in Asia travel retail. This might indicate that the current weakness is temporary and simply the result of some near-term headwinds, and while that seems to be the case up to a point, the problem appears to be rooted somewhat deeper.

Looking at the historical margin development, we can see margins hit a decade low, but even more importantly, the gross has been consistently deteriorating since 2016, falling from above 80% to 76.5% in its record FY22. This decline then accelerated over the last year, reaching a current low of close to 71%.

Estee Lauder gross margin development (Macrotrends)

This shows that the margin decline has already been going on for much longer than just the last year. This problem only became substantial in the last year as growth also slowed, accentuating the issue. In contrast, Estee Lauder grew out of the problem in previous years by outgrowing cost growth. However, not anymore, and the margin development is highly worrying as the problem extends past near-term headwinds.

It is safe to say that management will be desperate to return to its previous sales levels and sustainable growth to boost the reported gross margin. However, as growth is expected to stay moderate, management has a serious challenge on its hands.

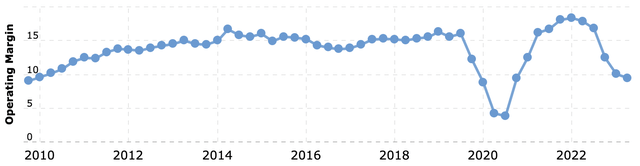

The operating margin development in its fiscal FY23 also was not significant as expenses as a percentage of revenue were up 390 basis points, mainly due to SG&A expenses remaining very high, including in areas such as advertising, promotion, innovation, and selling, which collectively increased by 280 basis points as a percentage of sales.

Gurufocus

This caused the operating profit to drop by 52% YoY and the operating margin to fall 830 basis points to 11.4%. This was also not helped by the second-largest segment – makeup – delivering a negative operating income, despite M.A.C, the world’s biggest makeup brand, being the best-performing brand across the entire portfolio in fiscal FY23 and accounting for the majority of the makeup sales.

This worries me as, apparently, the fastest-growing brand can barely deliver an operating profit, which is a negative indication for margin developments and seems to result from excessive marketing expenses. In order to improve operating income for this segment, management will need to get these costs under control, but recent commentary only indicates that it plans to increase these costs, creating a tough margin outlook.

Estee Lauder operating margin development (Macrotrends)

This deteriorating margin profile led to EPS also being down 52% YoY to $3.46. Furthermore, while the Q4 top-line performance showed a meaningful improvement from previous quarters, the gross margin was still down 330 basis points YoY, and the operating margin 380 basis points YoY, showing little progress.

Nevertheless, according to management, restoration of the operating margin is a top priority, although through a multi-year plan. A skincare and makeup segment recovery over the next 12 months will support margin improvements, but not very significantly. Another positive development regarding margins for Estee Lauder will be the slowing inflation rate, which might positively impact the YoY growth in expenses.

Furthermore, management plans on using its pricing power and brand strength to boost the gross margin, but I am not sure how this will work in a challenging economic environment where consumer spending power is down. Management added the following regarding the improvement of the gross margin:

… inclusive of driving additional accretive and compelling innovation, and improvements in operational efficiencies including enhanced supply demand planning and inventory optimization to reduce excess inventory and discount.

Still, despite management’s faith and commitment to improve margins, I am afraid Estee Lauder will struggle to boost margins and bring these back to historical levels with competition heating up, impacting its premium pricing power and requiring significant marketing expenses.

Another reason I am not seeing sufficient margin growth in the years ahead is the shift to less premium products. For a couple of years, Estee Lauder has also started focusing on the less premium brands to reach a larger audience with its products. However, this does impact margins.

Yet, the company seems to have little choice. As discussed earlier, the skincare segment will lose its share if it keeps focusing on the high-end product range as consumers are getting more price-aware and are looking for cheaper alternatives.

However, I am not expecting the luxury markets to disappoint as a whole. I am confident about the luxury industry due to the growing wealth globally. Yet, companies need to distinguish themselves through quality or price in a highly competitive industry such as cosmetics. The cosmetics industry is far more sensitive to price awareness than luxury verticals like cars and fashion.

To round things up, there is the balance sheet and shareholder returns. The company currently has $4 billion in total cash on the balance sheet against a total debt of $10 billion. With EBITDA off approximately $2.5 billion expected for its next fiscal year, it is at a net debt/EBITDA position of 2.4x, which could be better but is manageable, assuming cash flows improve over the next couple of years.

Shares currently yield 1.9%, offering a decent yield, although at a payout ratio of 74%. Of course, this is based on depressed cash flows, so I expect the dividend to be safe and well covered, with plenty of room for growth in line with sales growth.

Outlook & EL stock valuation

For its fiscal FY24, management has guided growth to return with organic sales rising 6% to 8%, which should also drive a slight operating margin improvement of 60 to 110 basis points YoY to 12% to 12.5%, still sitting very far below its historical averages. This should lead to EPS in the range of $3.50 to $3.75

This includes Q1 guidance of a 12% to 10% organic sales decline and EPS of negative $0.31 to negative $0.21. This includes the impact of a cybersecurity breach earlier this calendar year, amounting to $0.07. Finally, management expects to be able to drive more consistent compounded annual sales growth within the 6% to 8% long-term growth algorithm, although I expect this to be closer to a 5-7% range.

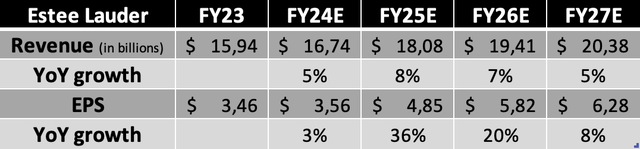

Following my research of the company and management’s near-term guidance, I now expect the following financial results through the company’s fiscal FY27. This includes the expectation of the company seeing a solid recovery in travel retail sales over the next two years and it growing in line with the industry in the years after. Furthermore, I do expect some improvement in the gross margin in the next two years to around a 74% to 75% level, still below its highs of 80%, and this to drive a more meaningful improvement in operating income with an operating margin recovering to 17-19%. However, I do not see much more room for further improvements in the years after without a solid margin improvement plan from management, including much-improved operating efficiency.

Financial estimates (Author)

Historically, Estee Lauder shares have received a significant premium from investors in terms of its valuation, as do many of its luxury peers, and rightfully so. The luxury industry is very appealing due to its anti-cyclical and inflation-resistant nature and its strong dependence on brand power. This and solid growth make it an industry deserving a premium valuation. This has led to Estee Lauder receiving a 5-year average valuation of 40x earnings.

However, the last five years have looked much better than it does today in terms of growth, financial health, and operational performance. Despite significant headwinds and all issues discussed throughout the article, shares are still valued at a premium of 38x the FY24 EPS projection, already pricing in a sales and margin recovery as management has guided for and even more. However, I believe there is a significant risk of financial results disappointing and meaningful margin expansion staying out due to increasing costs and moderate sales growth. While the current analyst consensus is guiding for EPS growth of above 50% for fiscal FY25, this seems too optimistic.

Furthermore, with this already priced into the shares, this creates a very unfavorable risk-reward profile. While the company has very strong brands, the mediocre execution by management, moderate sales growth, and uncertain margin outlook do not warrant a premium any longer. For example, L’Oréal seems much better positioned with a similar sales growth forecast and lower risk profile while trading at a similar valuation, all things considered.

Based on the current outlook and operational risks, I believe Estee Lauder shares are no longer attractive at a P/E of over 25-30x. Using my FY25 EPS forecast to include some margin expansion and a 28x earnings multiple (L’Oréal trades on a 25x multiple, but the EPS forecast for Estee Lauder is looking better), I calculate a price target of $136. Going with an annual return of 10%, I believe shares are fairly valued at $112 today, reflecting another 18% downside risk.

Whereas my medium-term financial estimates are conservative and definitely leave room for upside, I believe this is required to account for the operational risks involved and the company’s increased overall risk profile to make this an interesting investment today.

However, at the current share price of $137 and my conservative outlook, investors should expect annual returns of 0% over the next two years. (1.5% including dividends). Even based on the current, more bullish expectations from Wall Street analysts and a 28x earnings multiple, total annual returns are limited to 7.5% while taking on significant risk.

Based on this, I believe there are many more attractive opportunities in the market today. I recommend that investors who want exposure to the cosmetics industry look closely at L’Oréal. With further downside highly likely, I am rating shares a sell/avoid and will revisit once the situation changes. For now, I believe it is best to avoid EL shares (I would not short them due to the technical profile and significant decline YTD).

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here